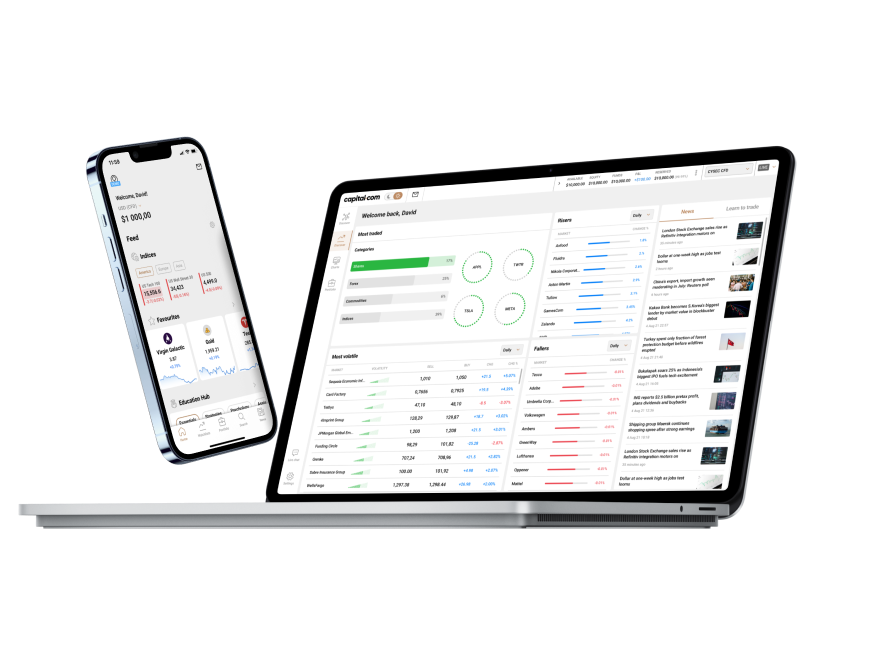

In Italia scegli un broker solido ed affidabile

Gentile trader, siamo consapevoli che la sicurezza è importante per te. Affidati a un broker che gestisce volume di transazioni superiore a 1 trilione di dollari, con la certezza che il denaro sia custodito presso i più rinomati istituti di credito.

Autorizzata e regolamentata dalla Cyprus Securities and Exchange Commission (CySEC)