Why aren't rising geopolitical risks driving gold prices higher?

Gold prices have slid despite rising geopolitical risks stemming from conflict in the Middle East.

Gold prices have fallen since the onset of the war between Iran, Israel and the US. That is despite the rise in geopolitical risks, which are typically associated with a higher gold price. The drop in gold is generally attributed to a stronger US Dollar, due to so-called “safe haven” demand. While true, this isn't the complete story. Gold is falling because of a stronger US Dollar. But the reasons are more complex and varied, combining fundamental, mechanical and technical drivers. On top of that, those drivers are mostly short-term in nature, with the longer term impacts of the war still potentially supportive of gold.

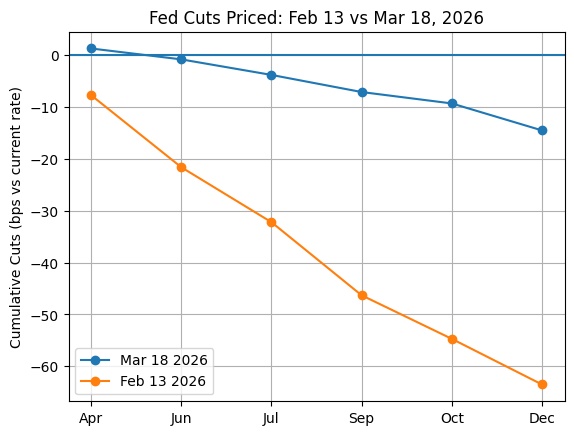

Expectations of higher interest rates

The first driver of a stronger US Dollar is shifting interest rate expectations. The surge in oil prices has led to expectations of higher inflation around the world, including the United States. For example, the last time oil was around $US100 per barrel, headline CPI in the US was nearly 6%. The risk of stronger inflationary pressures has led the market to aggressively price-out future interest rate cuts from the US Federal Reserve. Currently, the markets imply no cuts for 2026 compared to more than two before the onset of the war. That has contributed to a lift in Treasury yields and the US Dollar, subsequently weakening gold.

(Source: Bloomberg, Capital.com)

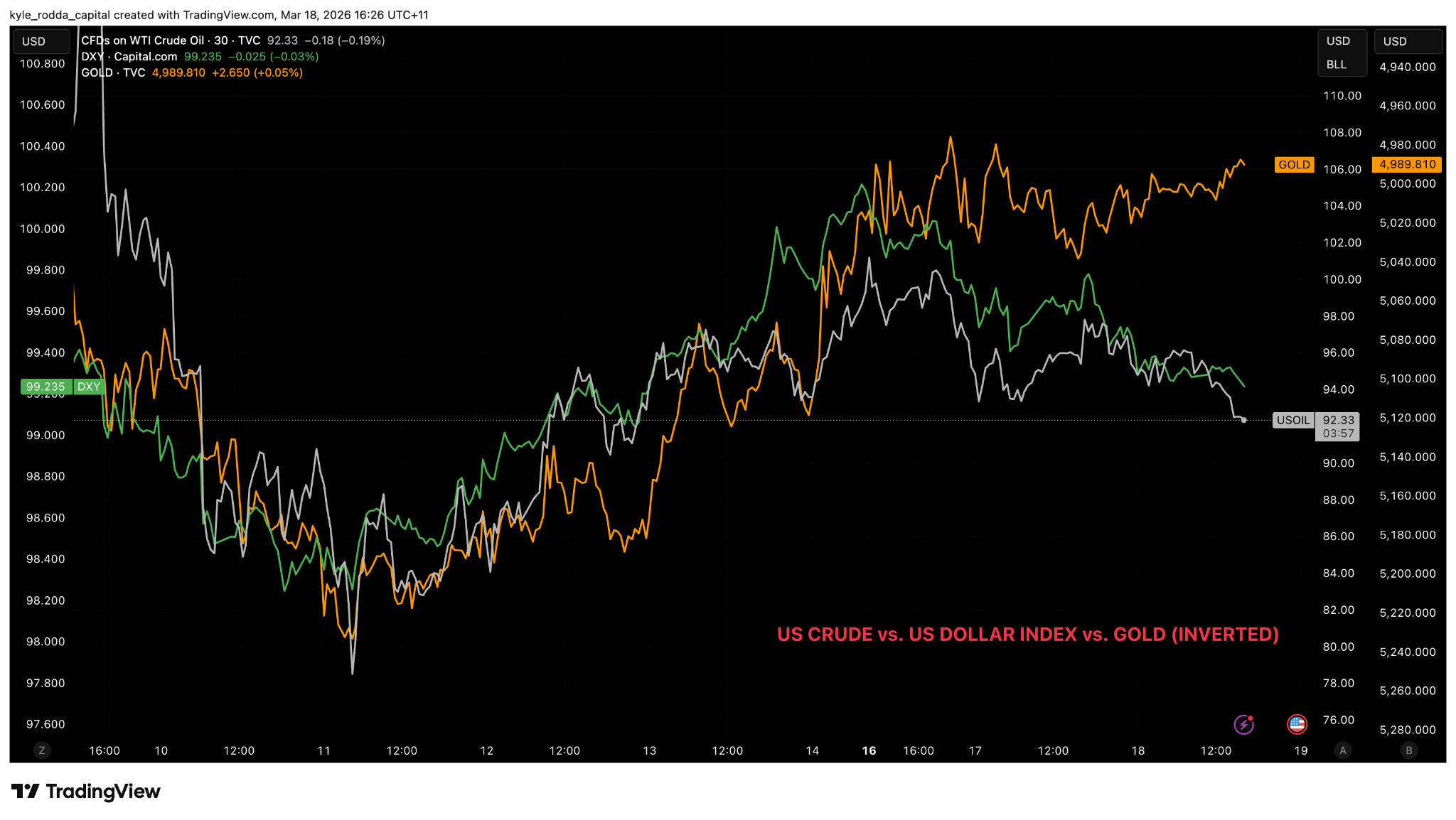

Higher oil prices lifts US Dollar demand

The second driver of a stronger US Dollar boils down to the mechanical relationship between the currency and oil prices. Crude oil products are denominated in US Dollars. That means buyers of crude require US Dollars when making the purchase. When oil prices rise, buyers need more Dollars to pay for the same quantity of oil. This lifts demand for US Dollars, causing it to appreciate. Because gold is also denominated in US Dollars, its price moves inversely to the currency. Hence, as oil prices rise, the Dollar rises too, putting downward pressure on gold.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

Tighter liquidity drives demand for US Dollars

The third driver is liquidity. The US Dollar sits at the centre of the global financial system, acting as the primary funding currency. The war has lifted credit risks and the availability of funding. At the same time, demand for short-term liquidity has increased as market participants seek to manage heightened uncertainty. This combination has pushed up Dollar funding costs. Crucially, a significant share of global debt is denominated in US Dollars. As funding costs rise and when investors need to meet Dollar liabilities, they are forced to sell other assets – including gold – for cash. This creates a bid for the US Dollar, pushing down on gold.

Higher energy prices boost US trade position

The fourth driver is trade balances. The impact of higher oil prices on an economy and its currency is influenced significantly by whether it imports or exports energy. An importer of energy will see its trade position worsen, reducing the demand for its currency. An exporter of energy will see its trade position improve, increasing the demand for its currency. The US is a net energy exporter, meaning higher oil prices support the US Dollar. Economies like Japan and the Eurozone are energy importers, meaning higher oil prices weaken their currencies. This dynamic gives the US Dollar a broad-based boost, weakening gold.

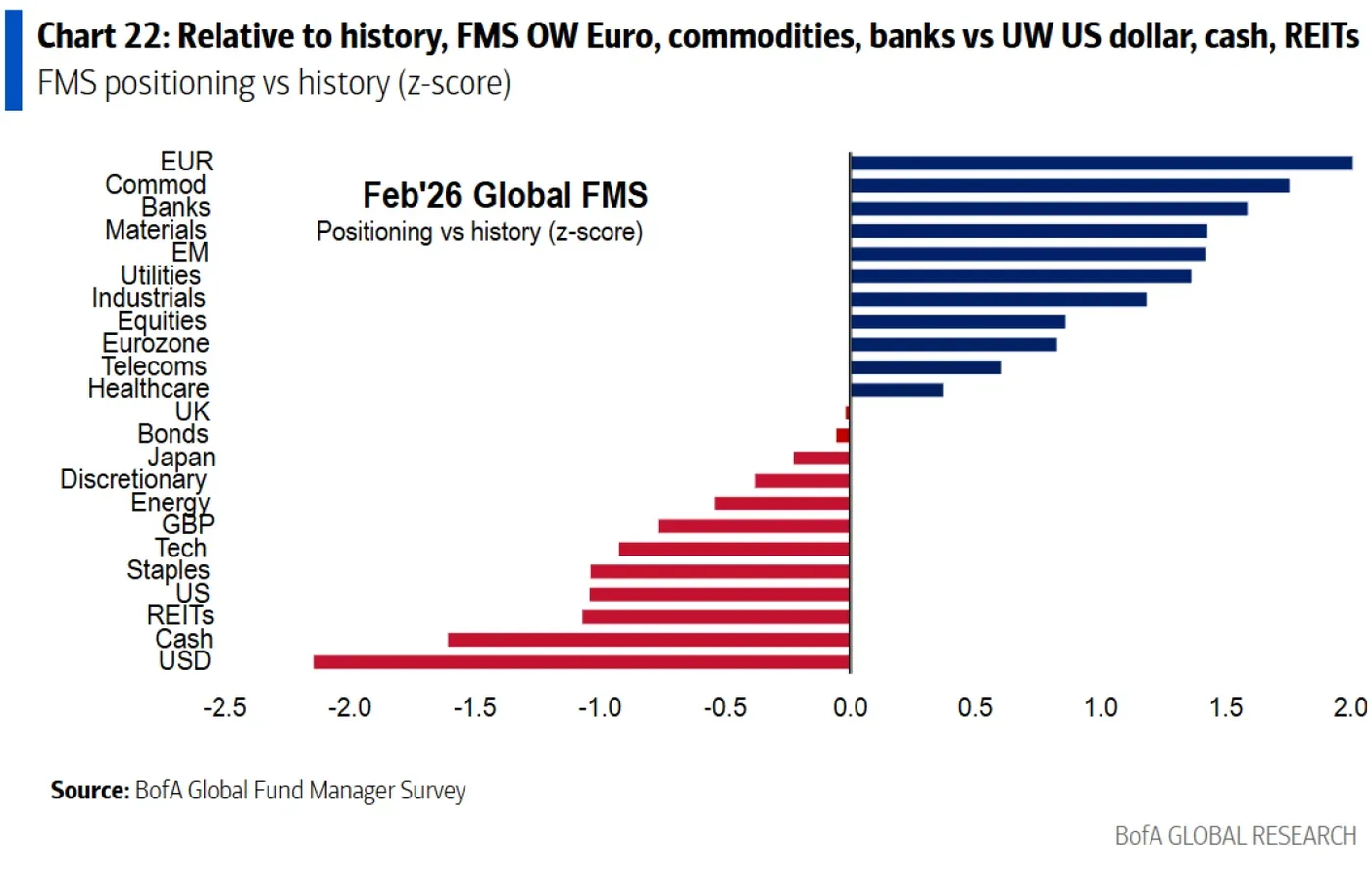

Long gold and short Dollar trades unwind

The fifth driver is positioning. The markets were heavily short US Dollars before the onset of the war. In fact, the February Bank of America Global Fund Manager Survey suggested short-positioning in the US Dollar was at historic extremes. The unwinding of these short-positions has added fuel to move in the US Dollar as the currency responded to fundamental shifts in energy prices, trade flows, financial conditions and interest rates. At the same time, investors were historically long commodities, including gold, with the repositioning in both contributing to weaker gold prices.

(Source: Bank of America)

Geopolitical risk may benefit gold in long run

The fundamental, mechanical and technical factors driving the US Dollar higher and the gold price lower are short term in nature. As a result, the weakness in gold could be temporary. In the longer run, the fundamental case supporting gold hasn’t changed. Arguably, the more unstable geopolitical backdrop and the greater erosion of trust in the US government caused by the war will further support gold. The trend for the commodity also remains to the upside. That means uptrend for gold could be poised to continue once the short-term drivers of US Dollar strength diminish.