What’s this page for?

This page will show a complete costs and charges breakdown across our products, covering spreads, overnight adjustments, and guaranteed stop-loss orders (when activated).

You’ll find examples demonstrating how we calculate our fees, which you can apply to your own trades to estimate the cumulative effect of our costs and charges on your returns.

It’s important to remember that your total costs will increase proportionate to your trading volumes.

The example trades and the values shown in this document are for illustrative purposes only. They should not be treated as forecasts, recommendations or endorsements of a particular trading strategy.

- For more information on our costs and charges, click here.

- You can also find out how we price our markets per asset class by clicking here.

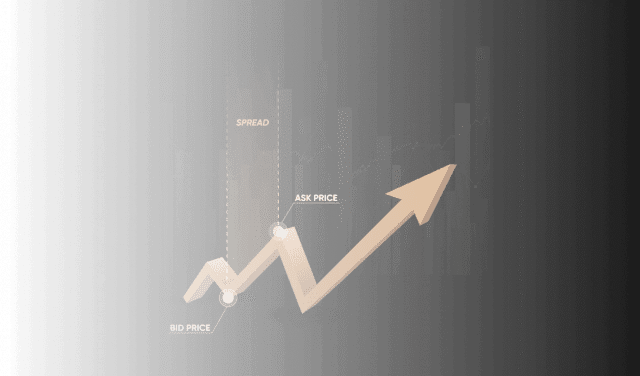

Spread cost examples for CFD trades and spread bets

In this section, we’ll focus on spread cost examples across our five main asset classes, using CFDs. The spread is the difference between the bid and ask price of the market at the time you place your trade. It’s charged to cover the cost of facilitating the trade, and it’s the main way we and other derivatives brokers make money.

While spread bets* are structured differently to CFDs, their costs are identical. However, it’s important to remember that spread betting is exempt from capital gains tax,* so this should be factored into your cost calculations. For our unleveraged 1X product, the only fee you’ll pay is the spread.

Trading outside regular exchange hours may be available on selected stocks. Please note that spreads can widen, and liquidity may be lower during these times, which can impact execution quality and cost.

You can find typical spread prices by clicking on your chosen asset on our markets page, in the ‘All markets’ section.

*Tax treatment depends on individual circumstances and can change or may differ in a jurisdiction other than the UK. Spread betting is not available to clients outside the UK.

Forex

- You hold a position of 100,000 units of EUR/USD, with a bid/offer quote at 1.05000/1.05006.

- The spread on this market is therefore 0.6 pips (0.00006).

- Opening the position: you pay half the spread when you enter (0.3 pips, or 0.00003).

- Closing the position: you pay the other half when you exit (0.3 pips, or 0.00003).

- The spread is calculated in the quote currency.

- Total cost of the spread: 100,000 units × 0.00006 = $6 (or equivalent in your account currency).

Commodities

- You hold a position of 10 contracts on Gold (10 troy ounces), with a bid/offer quote at 2500.00/2500.30.

- The spread on this market is therefore 0.30 points (2500.30-2500.00).

- Opening the position: you pay half the spread when you enter (0.15 points).

- Closing the position: you pay the other half when you exit (0.15 points).

- Total cost of the spread: 10 contracts × 0.30 points = $3 (or currency equivalent).

Indices

- You hold a position of 1 contract on the UK 100, with a bid/offer quote at 9000/9001.

- The spread on this market is therefore 1 point (9001-9000).

- Opening the position: you pay half the spread when you enter (0.5 points).

- Closing the position: you pay the other half when you exit (0.5 points).

- Total cost of the spread: 1 contract × 1 point = £1 (or currency equivalent).

Shares

- You hold a position of 10 shares on Apple, with a bid/offer quote at 240.00/240.13.

- The spread on this market is therefore 0.13 points (240.13-240.00).

- Opening the position: you pay half the spread when you enter (0.065 points).

- Closing the position: you pay the other half when you exit (0.065 points).

- Total cost of the spread: 10 shares × 0.13 points = $1.30 (or currency equivalent).

Overnight funding (swaps) cost examples

Every time you hold a leveraged trade open overnight, your position will be subject to a funding adjustment, or swap. This reflects the cost of borrowing to maintain the leveraged exposure. Whether you pay or receive this adjustment depends on several factors, including the instrument, trade direction, and underlying interest rates.

Forex

- You hold an overnight position of 10,000 units of USD/JPY. Your nominal exposure is therefore $10,000.

- For the purposes of this calculation, let’s say the overnight swap (or TomNext) rate for USD/JPY is currently -0.0182. At the prevailing spot price of 132.80 that equates to -0.0137% daily.

- Our daily fee is 0.00411%.

- So to hold a long position overnight you would receive 0.00959% – the negative USD/JPY swap rate less our fee – of your exposure, which, converted from JPY, is $0.96 or currency equivalent.

- To hold a short position, you would pay 0.01781% – the positive swap rate plus our fee – of your exposure, which is $1.78 converted, or equivalent.

Commodities

- You have a position of 4,000 therms of Natural Gas, currently priced at $2.54. Your position’s full exposure is therefore $10,160.

- Let’s say the overnight basis adjustment for Spot Natural Gas is currently 0.0031. At the prevailing spot price of 2.54 that equates to 0.12205% daily.

- Our daily fee is 0.01096%.

- For a long position, you’d pay 0.13301% (our fee + the basis adjustment) = $13.51.

- For a short position, you’d receive 0.11109% (our fee – the basis adjustment) = $11.29.

Indices (USD denominated)

- You have a position of 0.6 contracts on the US Tech 100, priced at 20140. Your full exposure would be $12,084.

- Since the US Tech 100 is denominated in USD, the relevant benchmark rate is SOFR. Let’s say this is 5.01448% annually, or 0.01393% daily.

- Our daily fee is 0.01111%.

- For a long position, you’d pay 0.02504% (Our fee + SOFR) = $3.03.

- For a short position, you’d receive 0.00282% (Our fee – SOFR) = $0.34.

Indices (GBP denominated)

- You have a position of 1 contract on the UK 100, priced at 8175. Your full exposure would be £8,175.

- Since the UK 100 trades in GBP, the relevant benchmark rate is SONIA – let’s say this is 4.98260% annually, or 0.01365% daily.

- Our daily fee is 0.01096%.

- For a long position, you’d pay 0.02461% (our fee + SONIA) = £2.01.

- For a short position, you’d receive 0.00269% (our fee – SONIA) = £0.22.

Shares (USD denominated)

- You have a position equivalent to 50 shares in Tesla, currently priced at $252. Your total exposure is $12,600.

- Since Tesla trades in USD, the relevant benchmark rate is SOFR. Let’s say this is 5.01448% annually, or 0.01393% daily.

- Our daily fee is 0.01111%.

- For a long position, you’d pay 0.02504% (our fee + SOFR) = $3.16.

- For a short position, you’d receive 0.00282% (our fee – SOFR) = $0.36.

Shares (GBP denominated)

- You have a position equivalent to 4000 shares in Barclays, currently priced at £2.41. Your total exposure is £9,640.

- Since Barclays trades in GBP, the relevant benchmark rate is SONIA. Let’s say this is 4.98260% annually, or 0.01365% daily.

- Our daily fee is 0.01096%.

- For a long position, you’d pay 0.02461% (our fee + SONIA) = £2.37.

- For a short position, you’d receive 0.00269% (our fee – SONIA) = £0.26.

Bonds/interest rates

CFD example

- You have a position on the US 10-Year T-Note CFD, currently priced at $112.50 per 100 face value. Your position’s full exposure is $200,000.

- Let’s say the overnight basis adjustment is -0.0008. At a price of 112.50, that equates to:

- (-0.0008 / 112.50) × 100 = -0.0711% daily

- Our daily fee is 0.01096%.

- If you're long:

- Total overnight rate = 0.01096% - 0.0711% = -0.06014%

- Funding = $200,000 × -0.06014% = -$120.28

- You’d receive a credit of $120.28 overnight.

- If you're short:

- Total overnight rate = 0.01096% + 0.0711% = 0.08206%

- Funding = $200,000 × 0.08206% = $164.12

- You’d pay a funding cost of $164.12 overnight.

Note: the overnight fee also applies to forward contracts.

Guaranteed stop-loss order cost example

A guaranteed stop-loss order (GSLO) fee is only charged if the GSLO is triggered. The GSLO closes the trade at exactly the price level you specify, with no risk of gapping or slippage. Since we take on this risk for you, we (and other providers) charge a fee for using the GSLO.

You can see the GSLO fee on the deal ticket before placing your trade, once you’ve selected a GSLO. The GSLO premium itself varies depending on the specific market, the position's open price, and the quantity traded.

Formula

You can check the GSLO fee value on the deal ticket when opening a position and adding GSLO.

Guaranteed stop-loss order example

- You open a long position of 1 Gold contract, with a bid/offer quote at $2,000/$2,000.30.

- You place a GSLO at $1,980 to limit potential losses.

- Assume the GSLO premium for this market is 0.03%.

- If the market drops to $1,980, the GSLO ensures your position is closed exactly at that price, with no slippage.

GSLO fee calculation:

- GSLO fee = GSLO premium × position open price × quantity

- 0.03% × $2,000.30 × 1 contract = $0.60

- Total GSLO fee charged (if triggered): $0.60