FOMC preview: updated projections to give more insight into the path of rate cuts

Hotter CPI data weighs on rate cut hopes from the Federal Reserve

The Federal Reserve is expected to leave rates unchanged at their meeting next week. Data from Reuters shows a 99% chance of no change at the meeting on Wednesday following hotter inflation readings. There was already little hope for a 25bps cut at the March meeting, but traders hoped the latest data would support policy easing by June. That may not be the case any longer, even if futures continue to price in a 52% chance of a rate cut in June.

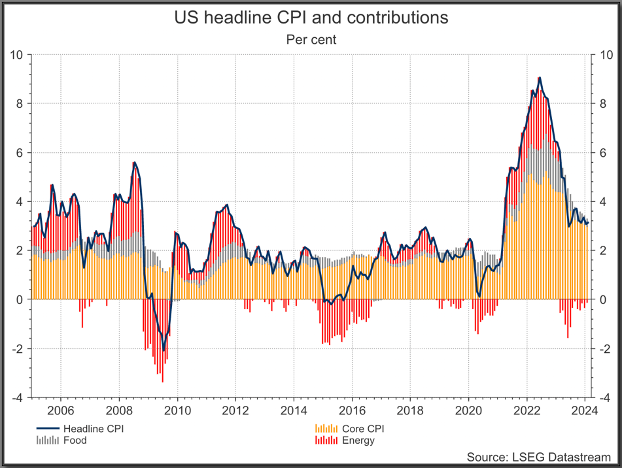

Consumer prices came in higher than expected in February for the third month in a row. The price of goods and services is 3.2% higher than it was in February last year, a rise from the 3.1% seen in January. Core prices – which exclude volatile elements like energy and food – rose 0.4% month-over-month, for the second month in a row. Markets had been hoping the rate would drop to 0.3%. The yearly rate did manage to drop from 3.9% to 3.8%, but markets had been a tad more optimistic, with expectations for a drop to 3.7%.

Past performance is not a reliable indicator of future results.

Higher-than-expected producer prices added more fuel to the fire on Thursday. February saw prices rise for the second month in a row, suggesting an end to the drop in prices experienced in the last quarter of 2023. The price of goods at the start of the production line rose 0.6% in February from 0.3% the month prior. This higher reading could lead to higher consumer prices down the line, which should put the Fed on high alert for a resurgence in inflationary pressures.

All in all, the readings suggest that the disinflation process is proving to be stubborn in its final stage. This isn’t necessarily worrying, given that non-linearity within the return to the 2% target is not uncommon. Still, it does pour cold water on hopes that the Federal Reserve may start cutting rates soon.

The inflation data is conflicting with the latest jobs data released last week. The key takeaway was that the tightness in the labour market is unwinding, with monthly wage growth coming in at the lowest level in two years, while the unemployment rate rose unexpectedly. By no means does it show a particular weakness in the US economy – wage growth is still above its long-term average – but it did validate the perception that the Federal Reserve could be starting to consider cutting rates soon.

Futures markets are currently pricing 75 basis points of cuts in 2024, a significant drop from the 150 priced at the start of the year. Stronger data has eased expectations of immediate policy action from the Federal Reserve, but interestingly, the stock market hasn’t suffered the consequences. Tuesday’s hotter CPI print is a good example of this, as both the S&P 500 and the US Tech 100 ended the session higher, just inches away from the recent highs. There also no longer seems to be a ‘bad-data-is-good-rally’, as evidenced by the lack of follow-through on Friday after the weaker jobs data. Currently, US equity markets seem to be moving higher, slightly unfazed by the latest data.

This could be because traders are confident that they understand the path of monetary policy the Federal Reserve is on and are convinced that rate cuts are coming, even if they are a little later or slower than originally thought. It also helps that projected profits are holding up, given the recent round of corporate earnings. Ultimately, markets don’t seem to mind higher rates if they are discounting higher profits. So, it seems like as long as rates don’t go higher, the momentum in stocks could remain bullish.

S&P 500 daily chart

Past performance is not a reliable indicator of future results.

Attention will likely be drawn to the updated projections and the dot-plot graph. This will be the first time we get updated numbers this year, as the last one was in December. Back then, the general feeling was that data was weakening across the board, including inflation, so it will be interesting to see how expectations within the FOMC have shifted, given the recent strengthening in some data points. Back then, the dot-plot showed a majority leaning towards 75bps of cuts in 2024. Any amendment to this could cause volatility across the broader market.

USD buyers remain unconvinced despite the stronger inflation data. Thursday saw a rebound in appetite after the higher-than-expected PPI release, but there is a lack of follow-through, suggesting traders are not convinced that buying USD is appropriate right now. Fundamentally, the balance remains tipped in favour of a rate cut over another rate hike, which puts downward pressure on the dollar. However, the prolonging of the first-rate cut, given the stronger data, is allowing the dollar to regain some composure.

If the Fed is seen as more hawkish in this meeting by emphasising the stronger data or even adjusting the projections higher and pushing back on rate cuts this year on the dot-plot graph, then the bullish momentum could re-emerge in USD. This could also weigh on equities, even if just temporarily.

US Dollar Index (DXY) daily chart

Past performance is not a reliable indicator of future results.