Recap of the Bank of England and Federal Reserve meetings

Both the bank of England and Federal Reserve have delivered their latest policy updates this week and here is how markets have reacted

BoE Holds, Slows QT: markets read “less hawkish than feared”

The Bank of England left Bank Rate unchanged at 4.0% with a 7–2 vote, citing persistent—though easing—domestic inflation pressures alongside subdued growth. The MPC said underlying disinflation has continued, pay growth is slowing, and CPI was 3.8% in August, likely to tick up slightly in September before moving closer to target. Guidance stayed cautious: policy is not on a preset path, and the MPC will take a “gradual and careful” approach to any further withdrawal of restraint, remaining data dependent.

On the balance sheet, the MPC conducted its annual review of quantitative tightening and decided to slow the pace: the stock of gilts held for policy purposes will be reduced by £70bn over the next 12 months (vs £100bn previously).

The reaction in markets was muted, sterling softened slightly against the dollar (mostly due to renewed greenback strength), gilts firmed at the margin (yields a touch lower across the curve, with the long end benefiting from the tilt away from long-dated sales), and UK equities eked out modest gains. The move fits a “less hawkish than feared, but not dovish” take on a hold plus slower QT: trimming the annual gilt run-off to £70bn skewed sales toward shorter maturities, which eased some pressure on duration without materially changing the policy stance.

The odds of further cuts remain mostly unchanged. Less than 10bps of easing are priced in by year-end, with the next 25bps cut fully priced in for March-April next year.

GBP/USD daily chart

Past performance is not a reliable indicator of future results.

Powell opens the door—just not wide enough for markets

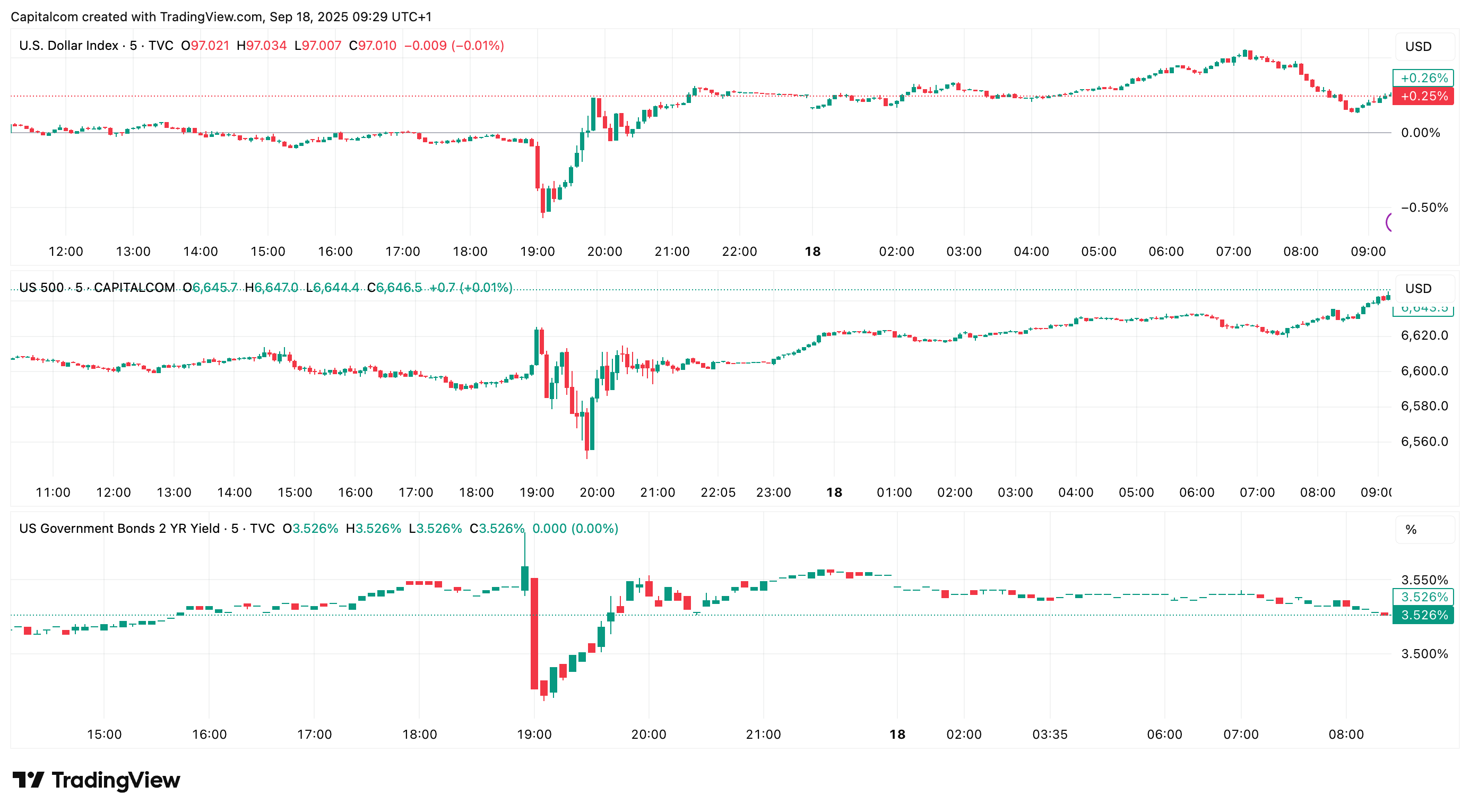

The Federal Reserve delivered the widely expected 25 bp cut, but the market’s reaction told a more complicated story. Stocks and gold initially jumped before fading through Chair Powell’s press conference, while the dollar and Treasury yields clawed back losses.

One of the key takeaways from the night - and possibly what weighed on risk sentiment given how heavily dovish markets were positioned heading into the meeting - was the lack of dissenters in the vote split. Only one member - newly arrived Stephen Miran, who is thought to be a de facto representative of the White House - voted for a 50bps cut. Given the recent labour data, markets had priced in a small chance of a jumbo 50bps cut. The likelihood was small, but the odds were there. The lack of backing offers some important clues for the future.

In July, both Christopher Waller and Michelle Bowman broke with the majority to push for a jumbo cut; last night neither pressed for 50. Both are rumoured to have a shot at Fed leadership once Powell’s term is over next year, and they must have known that their chances would be heavily influenced by their decision to vote on a larger cut. Their lack of follow-through suggests the Committee has coalesced around a measured cadence rather than a front-loaded easing—despite the politics swirling around the Fed right now. It also lowers the probability of outsized moves near-term and helps explain why equities and gold popped then faded while the dollar and yields firmed during the presser: the path got a touch less dovish than positioning implied.

Meanwhile, Powell’s remarks confirmed a recalibration in emphasis from stubborn inflation toward safeguarding employment, but he kept the guidance strictly data dependent. With inflation still elevated, he offered no guarantees, framing policy as a meeting-by-meeting exercise.

One of the key events for the evening was the updated dot plot, which in all honesty failed to provide much further insight. The shift has been towards lower rates, but it has been very modest, to the dismay of market participants. Traders continue to think that the FOMC will have to cut more than the dot plot implies, yet last night’s meeting didn’t validate the most dovish paths.

US dollar index (DXY), S&P 500 and US 02 year yield 5 minute chart

Past performance is not a reliable indicator of future results.

The labour outlook captured the Fed’s balancing act. Policymakers are more alert to the risk that joblessness could rise, yet the median projection for the unemployment rate is now slightly lower than in June. In other words, vigilance has risen, but the baseline still assumes a broadly stable labour market rather than a sharp deterioration.

From here, two signposts will shape the near-term debate. First, watch how quickly front-end OIS leans toward—or away from—two additional quarter-point cuts this year (if the labour data continues to wobble, the market will try to front-run a faster cadence again). Second, core PCE at month-end will test the Fed’s room to proceed: a softer print buys time and supports a gradual path; a re-acceleration would validate the dots’ caution and keep a lid on risk appetite.