S&P 500 faces resistance ahead of crucial data and FOMC meeting

US equities trade mixed on Friday as traders await the latest round of jobs data.

The bullish drive has been revived in US equity indices after a few weeks of downside pressure. The S&P 500 and the Nasdaq both broke to new highs on Wednesday driven mostly by technology stocks. The ADP May employment report also helped revive some buying appetite as it came in below expectations. There isn’t a very good correlation between the ADP data and the non-farm payroll data released later today, but markets took benefit in the weaker reading as a sign of a possible cooling in the US labour market, which could allow the Federal Reserve to cut some time in the coming months.

Money markets are assigning a 97% chance of no change from the central bank when it meets next week. But the ECB’s 25 basis point cut delivered on Thursday may have started to put traders in a better mood when considering the possibility that the Fed will actually be able to cut this year. For now, a 25-basis point rate cut is fully priced in by November, but Powell and his team have continued to be quite hawkish up until now, dampening hopes. Next week’s meeting will be a big test for markets as they’ll want an update on how the central bank expects things to unfold. Before the meeting, we’ll see the CPI data for May, another important market event.

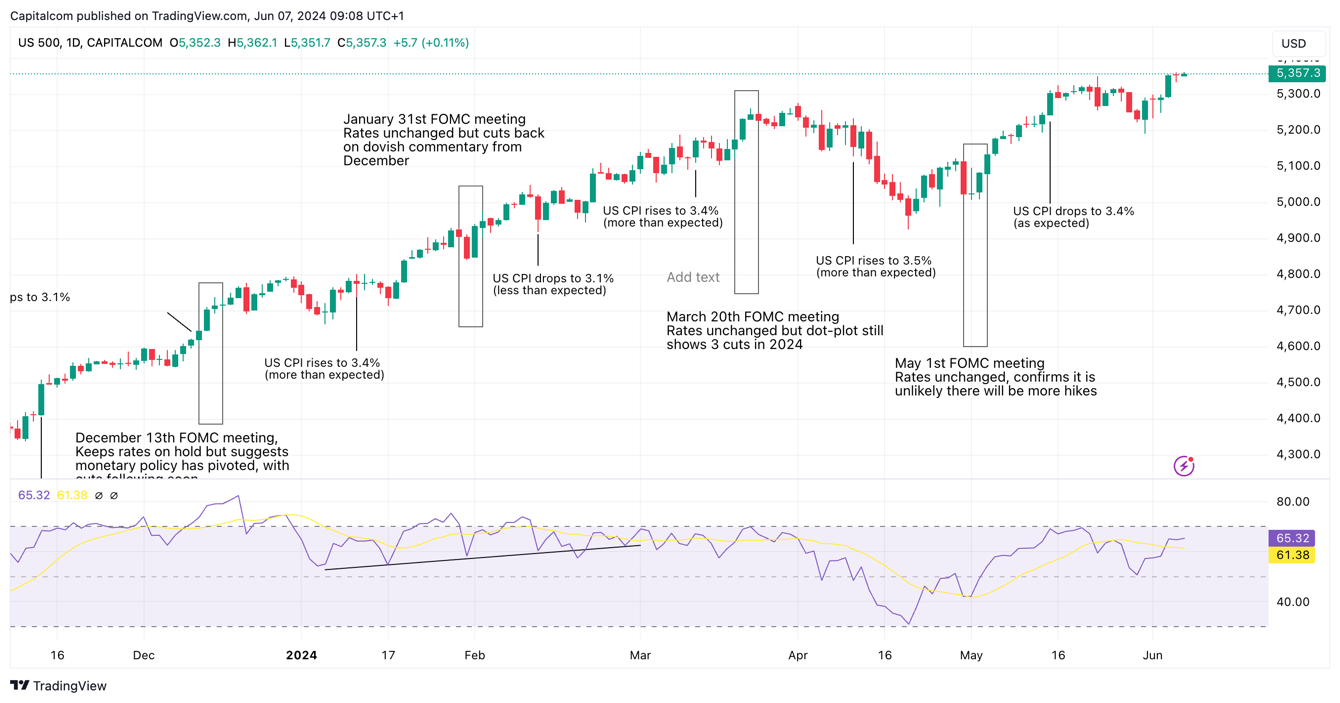

S&P 500 daily chart

(Past performance is not a reliable indicator of future results.)

(Past performance is not a reliable indicator of future results.)

On the chart, the S&P 500 continues to show potential for upside movement, but the rise ascent is becoming more laborious. Thursday saw little movement for the index as traders took a pause ahead of the latest labour data released on Friday. There is likely to be a lot of focus on the wage component of the data, as wage inflation has been sticky in recent months, and a key reason stopping the Federal Reserve from cutting. If the data comes in softer than expected, then it is likely that we see further bullish follow-through in the S&P 500 and other major US indices. That said, the chart continues to show signs of being a bit over-extended so the extent of the move might be slightly limited. Traders will also be weary of the CPI data being released next week so they may want to hold off on being too bullish just yet. The majority of the move is likely to come after the FOMC meeting next Wednesday, especially if the bank starts to show a readiness to cut rates fairly soon.