Trump is testing the markets' confidence – will they continue to “Sell America”?

In US President Donald Trump, the American people voted for someone to disrupt the status quo, and that’s what they have received. When it comes to the markets, President Trump is testing confidence. The question is: will it be permanent?

The US founding fathers crafted the American system of government to separate powers, of course politically, but also economically. While the label democracy is errantly thrown around to describe America, it’s more accurate to say it as a constitutional republic. The rule of law is supreme, with democratic, oligarchic and monarchic elements built in for the purpose of checks and balances. The system is designed to limit aspiring autocrats, as well as the proverbial rule of the mob, especially when the latter enables the rise of the former.

It’s this architecture that has helped make the US the most powerful economy in world history and the beloved bedrock of modern capitalism. For investors, this faith in America and its institutions underwrites the trust required to maintain a healthy and functional financial system, and the property rights necessary for investors to invest with confidence.

President Trump’s brand of national populist economics and exercise of unitary executive power has raised questions about this system and what it may mean for the US markets. The pressure on America’s constitutional republic is happening on several fronts and has sparked a mini crisis of confidence in the US government increasingly manifesting in financial markets as the so-called “Sell America” trade.

Domestically, President Trump’s use of the judiciary to target opponents had been politically provocative but of relatively little economic and investment concern. That changed for market participants recently with the threats against the US Federal Reserve, specifically, its Chairperson Jerome Powell. While the rhetoric from Trump about US Fed policy has been inflammatory, and, by the Fed’s own reckoning, designed to coerce, the threat of criminal charges against Powell in particular is an act normally reserved for emerging market autocracies with notoriously unstable monetary policy, markets and economies.

These attacks on the Fed bring direct risks and potential costs. US President Trump has openly called for interest rates at 1%, a level that, if lowered to, as unlikely as it is to happen, would almost certainly inflame price pressures at a time of already elevated inflation. Such a dynamic would undermine the credibility and policymaking ability of the Fed. Fortunately, the nomination by the Trump administration of Kevin Warsh as the next Fed Chairperson has allayed some of these fears. However, some luminaries still hold doubts about Warsh’s motives and allegiances, posing risks to optimal policy outcomes.

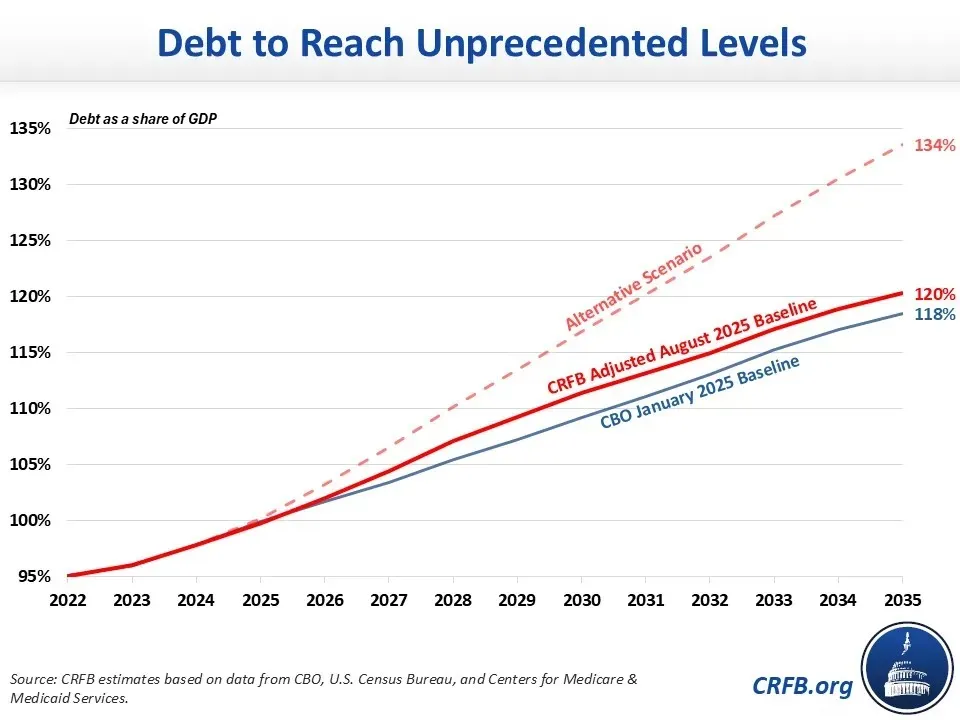

The Trump administration is also testing US markets on the fiscal side. While both sides of US politics are equally culpable, President Trump’s fiscal strategy is maintaining fiscal deficits at crisis-like levels around 5% to 6%, threatening to blow-out the government debt load and raising doubts about the value of US Treasuries. Even when given the opportunity to address the problem by using tariffs – an effective consumption tax – to cover public spending, the money is immediately earmarked for cash splashes to households at the expense of healthy public finances.

(Source: Committee for a Responsible Federal Budget)

(Source: Committee for a Responsible Federal Budget)

President Trump’s actions recently could be an inflection point. The fresh tariff threats waved at European economies to box them into handing over Greenland almost ended the EU-US trade deal and threatened NATO. The Trump administration walked back threats against European partners. However, there remains lingering damage to US prestige and credibility, especially amongst allies and trading partners, raising questions about future flows into US sovereign assets.

Whether the motive is for resources, a strategic land mass, living space, or whatever else, the erratic trade and foreign policy shakes trust in America. President Trump’s trade deals are worth little when they can be walked back in a social media post. All future agreements are put into perpetual doubt, casting uncertainty over global trade. That uncertainty gets reflected as heightened market volatility in the short-term and potentially less trade and weaker growth in the longer run.

Market signals are increasingly demonstrating the impact US President Trump’s policies are having on the markets. The so-called “sell America” trade has returned with force. Leading into President Trump’s recent Davos speech, the US Dollar hit a four year low, extending a roughly 10% decline in 2025. Gold prices surged to record highs – before spectacularly collapsing – in large part as investors shun Treasuries and seek out an alternative store of value. Central bank reserve managers, especially those of US adversaries, are reducing exposure to US sovereign assets, too, mostly in favour of gold.

Despite this, these moves are marginal in the bigger picture and largely add to what were existing trends. Wall Street is at record highs; US bonds tell a story of structural risks but yields at the long end have remained in a range for the past year. While highly politicised, the throwing out of cases against James Comey and more than likely Lisa Cook shows the courts are maintaining meaningful independence. The upcoming ruling on the legality of “emergency” tariffs will also be telling, both from the perspective of the balance of powers in the US, but also whether trade policy can be effectively dictated via social media posts.

The story here could be that for all the risks President Trump poses to US assets, investors still have faith in the strength of the American system to contain it. That is, like the Jacksonian period, the Civil War, and the Nixon era, the centre can indeed hold, and the “sell America” theme will be relatively short-lived.

Alternatively, the “sell America” trade could just be getting started, with the erosion of confidence in the US being offset in the short-term by loose fiscal policy, interest rate jawboning, mercantilism and state directed capitalism of President Trump, even if it brings risks in the long run.