UK mortgage rates forecast 2025

Explore the latest UK mortgage interest rate forecasts, with third-party insights on BoE mortgage rates, and , and how to trade rate-linked CFDs.

Mortgage interest rates represent the percentage a lender charges. In the UK, these rates closely track the Bank of England (BoE) official bank rate – directly influencing property affordability – and the current mortgage interest rates UK borrowers pay.

For contracts for difference (CFD) traders, shifts in mortgage rates often mirror wider changes in economic conditions and central bank direction – influencing forex CFDs such as GBP/USD, or share CFDs tied to housing and banking.

In this guide, we’ll explore the latest UK mortgage rate forecasts from third-party analysts, including how to trade shares and forex CFDs linked to rate movements.

Mortgage interest rates in the UK: Third-party forecasts

The Financial Conduct Authority introduced stricter affordability tests under the Consumer Duty in 2025, which requires lenders to act in the best interests of consumers and verify affordability. Moody’s viewed the FCA’s proposed simplification of affordability assessments as: 'Modestly credit positive' for the mortgage market.

Mortgage interest rates in the UK have been on a downward trajectory in the first half of 2025, following successive Bank of England (BoE) base rate cuts and declining inflation. The BoE reduced its cash rate by 25bps to 4.25% in May 2025, following successive cuts in April, and February – with further cuts priced in by markets. Lenders have responded by lowering fixed-rate mortgage deals – although the pace of reductions remains modest.

Rightmove predicted that two- and five-year fixed rates would average 4.73% and 4.66% respectively in 2025, with forecasters expecting gradual declines over the rest of the year. The UK property listings provider further forecasted that average fixed mortgage rates would settle around 4.0% in 2025, aligning with expectations for a BoE base rate near 3.5% by year-end.

On 14 May 2025, executive director of research at Zoopla, Richard Donnell noted that: ‘Expectations of lower interest rates are already priced into fixed rate mortgages today. Lower interest rates would likely result in further modest declines in mortgage rates.’

CBRE expected average two-year fixed rates to reach 3.4% by Q4 2025, while Fitch projected mortgage rates to decline marginally in 2026 after stabilising around 4.25% by year-end.

Meanwhile, Trading Economics projected that three-year fixed term mortgage interest rates would average 6.96 in Q2 2025, and fall to 6.71 in Q3, 6.46 in Q4, and 6.21 in Q1 2026.

Projected UK mortgage rates for the next 5 years

Looking further ahead, Fitch Ratings saw fixed rates trending towards 4.0% in 2026, while Zoopla flagged the likelihood of rates remaining in the 4%+ range depending on swap rate movements. As Morningstar highlighted, over 800,000 sub-3% fixed rate deals are set to expire annually until 2027, creating a sustained wave of refinancing activity.

The Office for Budget Responsibility’s (OBR) latest projections, however, highlighted that the average rate across the total stock of UK mortgages is still rising – from 3.7% in 2024 to a forecasted peak of 4.7% by 2028. This lag reflects the high share of borrowers on fixed-term deals, many of whom are yet to refinance.

Ultimately, while short-term rate cuts are widely anticipated, most forecasts suggest UK mortgage rates will stabilise in the 3.5-4.5% band over the next five years – barring sharp shifts in inflation or monetary policy.

Past performance isn’t a reliable indicator of future results.

What’s the UK’s mortgage interest rate history?

UK mortgage interest rates have historically seen wide fluctuations that reflect the BoE’s monetary policy decisions, inflation, and broader macroeconomic shifts.

In the early 2000s, fixed mortgage rates typically ranged between 4% and 6.5%, before falling sharply following the 2008 financial crisis. By 2009, two-year fixed rates began to fall below 4.0%, with five-year fixes at 3.7%, reflecting record-low base rates introduced to support the economy.

Between 2010 and 2021, mortgage rates remained historically low. Statista data indicated that five-year fixed deals fell to just 2.3% in 2021, helped by loose monetary policy and increased lender competition. That trend reversed from 2022, as the BoE raised rates to tackle inflation, and average two-year fixed rates peaked at 5.91% in mid-2023.

Rates have eased slightly in 2025. The UK Finance (formerly BBA) standard variable mortgage rate fell to 7.21% in April, down from 7.23% in March, according to Trading Economics. Meanwhile, Moneyfacts reported that average two- and five-year fixed deals dropped to 5.18% and 5.10% respectively in May.

What’s the average mortgage rate in the UK?

Based on the latest data, as of 22 May 2025:

- The average UK mortgage rate stood at 7.21% for revert-to-rate products, according to Trading Economics, which references BoE data.

- Fixed-rate deals were lower, with two-year fixes at 5.18% and five-year fixes at 5.10%, based on May figures from Moneyfacts.

While rates have edged down in early 2025, they remain above pre-pandemic levels – with further direction depending on the pace of BoE cuts and lender pricing. Fixed-rate deals, in particular, may respond quicker to swap rate changes than the revert-to-rate average.

Understanding BoE bank rate decisions

The Bank of England (BoE) sets the UK’s official interest rate – known as the bank rate or BoE base rate – to control inflation and support the economy. This rate directly affects mortgage pricing, as lenders use it to set borrowing costs.

At its latest meeting on 7 May 2025, the BoE’s Monetary Policy Committee (MPC) voted 5–4 to cut the bank rate by 0.25 percentage points to 4.25%. Two members pushed for a bigger cut to 4.0%, while two preferred to hold steady at 4.5%. The narrow split reflects ongoing uncertainty about the economic outlook.

Why the cut? Inflation has been falling – down to 2.6% in March – as earlier energy price shocks have faded and tight policy has cooled demand. But the BoE expects inflation to rise temporarily to 3.5% in Q3, before easing again. The UK economy has also slowed, with weaker growth and a softer jobs market since mid-2024.

What’s next for mortgage rates?

Markets expect at least one more rate cut in 2025, potentially taking the bank rate to 3.75% by year-end. But any moves will depend on how inflation, wages, and global trade risks develop.

For traders, BoE decisions influence GBP pairs like GBP/USD and UK-listed banking stocks. Mortgage rates tend to follow bank rate direction – but often adjust more slowly and depend on other factors like swap rates and lender competition.

Interest rates: How do they affect mortgages?

Historically, the BoE bank rate has influenced mortgage rates in the UK.

Global interest rate settings also play a role. If major central banks like the US Federal Reserve or European Central Bank shift policy, it can influence BoE decisions – which impact mortgage rates.

Here’s how two cash rate scenarios might impact variable mortgage rates:

| Scenario | Reaction | Result |

|---|---|---|

| BoE hikes the cash rate | Lenders may increase variable mortgage rates. | Higher repayments may reduce borrowing capacity, potentially weighing on housing prices. |

| BoE cuts the cash rate | Lenders may reduce variable mortgage rates.* | Lower repayments may stimulate demand, potentially supporting housing prices. |

*However, lenders may delay or partially pass on cuts, especially if their funding costs remain elevated.

For fixed mortgage rates, the link to BoE moves is less direct. Fixed rates reflect expectations about future interest rate changes and domestic bond market conditions, making them sensitive to shifts in BoE guidance and investor sentiment.

Discover third-party Bank of England (BoE) interest rate predictions.

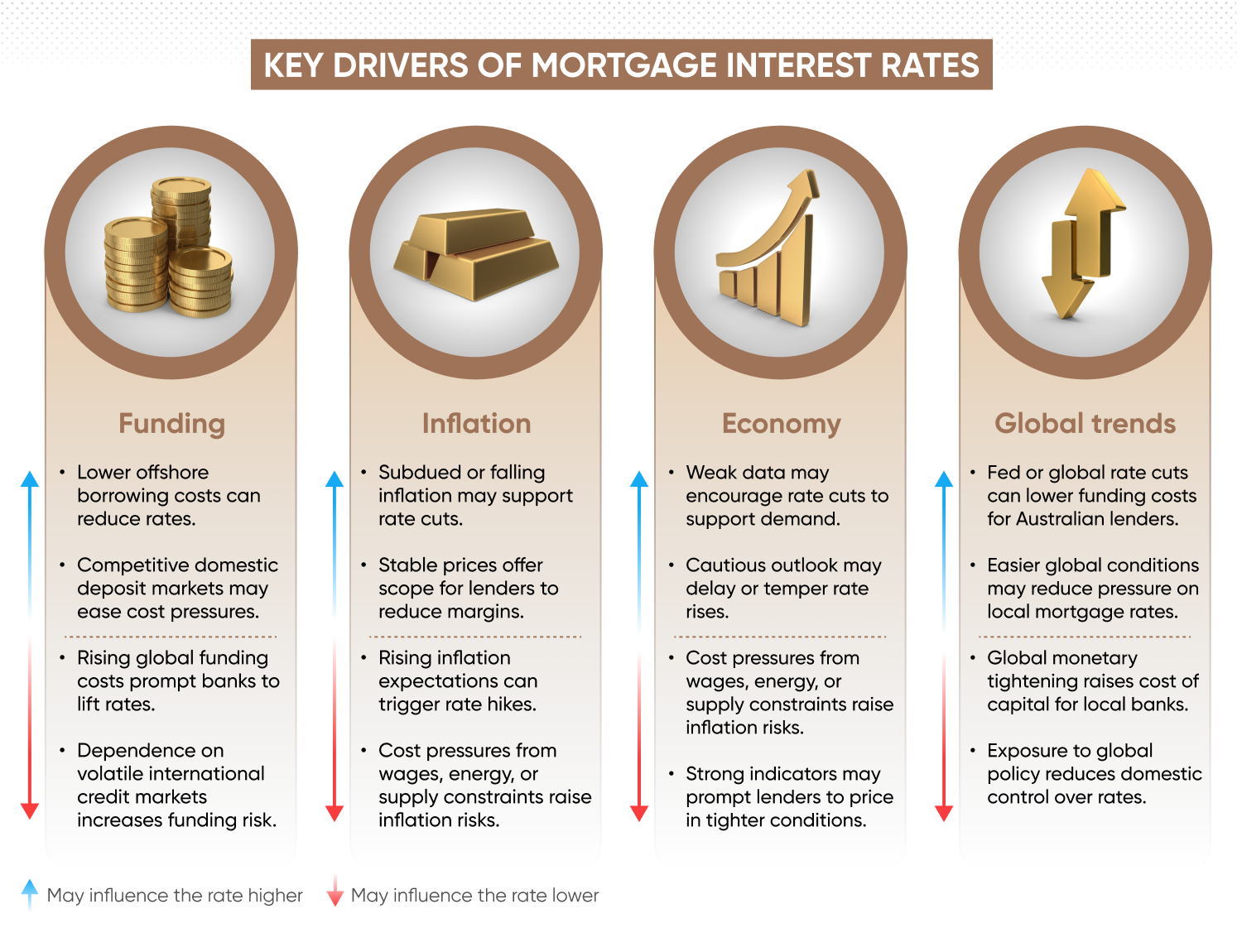

What other factors influence mortgage rates?

Although the BoE base rate is a key driver of UK mortgage pricing, several other factors influence how lenders set home loan rates – including inflation, wholesale funding costs and global monetary trends.

Swap rates

UK fixed mortgage rates are priced using medium-term swap rates (typically 2- to 10-year tenors) – which reflect market expectations for future interest rates. If swap rates rise, lenders may increase fixed-rate deals even if the BoE hasn’t moved. Conversely, falling swap rates can lead to cheaper fixed mortgages, particularly in a stable policy environment.

Inflation pressures

While the BoE targets inflation directly, lenders also watch pricing trends. With UK inflation at 2.6% (ONS, May 2025), concerns remain over wage growth and energy costs. If inflation expectations increase, lenders may price in more risk – keeping mortgage rates elevated even during periods of base rate cuts.

Funding costs

Lenders finance mortgages through a mix of deposits and capital markets. If wholesale funding becomes more expensive – due to global rate hikes or investor risk aversion – this can push up mortgage rates as lenders adjust for higher capital costs. Lower funding costs, by contrast, can allow for more competitive deals, regardless of BoE moves.

Economic indicators

UK data points like GDP growth, employment and consumer confidence also play a role. Stronger economic performance may raise expectations for tighter monetary policy, putting upward pressure on mortgage rates. Weak data may support cuts – but lenders could still price conservatively if risk appetite falls.

Global monetary policy

Decisions by other major central banks – especially the US Federal Reserve and European Central Bank – can influence UK swap rates and bond yields. For instance, when the Fed tightens policy, global yields and risk premiums have historically risen. This may lead UK lenders to lift mortgage rates, even if domestic conditions remain stable.

Past performance isn’t a reliable indicator of future results.

Past performance isn’t a reliable indicator of future results.

How to trade mortgage interest rates

While mortgage interest rates themselves aren’t directly tradeable, they can significantly influence a range of assets – particularly shares and forex contracts for difference (CFDs).

Here’s how to gain exposure to rate movements via CFDs:

Shares

UK mortgage rate changes may affect earnings outlooks for banks, homebuilders and mortgage real estate investment trusts (REITs) – these sectors are directly exposed to shifts in borrowing costs and housing activity.

Rising mortgage rates can reduce affordability, lower housing demand, and slow mortgage lending. That may weigh on homebuilders and residential-focused REITs, but can support bank margins if loan volumes hold steady.

Falling mortgage rates can stimulate home loan demand, boost refinancing, and support housing sentiment. This may support developers and mortgage specialists – though it may compress margins for lenders if rates fall faster than funding costs.

Here are some shares CFDs that have been sensitive to UK and global mortgage rate trends:

- Lloyds Banking Group – a major UK mortgage lender; share performance has historically reflected BoE rate expectations – trade Lloyds

- Barclays PLC – strong presence in UK residential lending; impacted by changes in mortgage affordability and credit demand – trade Barclays

- NatWest Group – UK-focused bank with mortgage lending exposure; BoE rate shifts influence revenue mix – trade NatWest

- Annaly Capital Management – US-based mREIT; performance influenced by the spread between borrowing and lending rates – trade Annaly

- Taylor Wimpey PLC – UK homebuilder; sensitive to shifts in affordability and housing demand – trade Taylor Wimpey

- Persimmon PLC – among the UK’s largest residential developers; mortgage trends influence sales outlook – trade Persimmon

- JPMorgan Chase & Co – major US bank with mortgage exposure; responds to Fed policy and housing sentiment – trade JPMorgan

- UWM Holdings – US mortgage specialist; sensitive to refinancing trends and long-term rates – trade UWM

Learn more about shares trading.

Forex

Mortgage interest rates are closely linked to long-term yields, which are influenced by central bank policy and macroeconomic conditions. The same factors also affect currency values

Rising mortgage rates can reflect expectations of tighter monetary policy, pushing up long-term yields and supporting the domestic currency – potentially supporting currencies like the US dollar (USD) or pound – particularly when central banks are seen as more hawkish than their peers.

Falling mortgage rates may signal a shift toward looser monetary policy, which can weigh on yields and put downward pressure on the currency. This could result in weakness for currencies like the British pound or euro, particularly if markets begin to price in further rate cuts.

Here are some forex CFDs that have reacted to interest rate expectations in 2025:

- GBP/USD – sensitive to diverging BoE and Fed policy paths; BoE cuts in early 2025 saw downside pressure – trade GBP/USD

- USD/JPY – historically tracks US Treasury yields; rising US mortgage rates have supported the dollar – trade USD/JPY

- EUR/USD – driven by relative rate expectations between the Fed and ECB; mortgage trends align with long bond moves – trade EUR/USD

- AUD/USD – responds to Reserve Bank of Australia guidance; housing and lending conditions have impacted sentiment – trade AUD/USD

- NZD/USD – like AUD, influenced by domestic rate expectations and refinancing activity – trade NZD/USD

- USD/CAD – Canada’s housing market and mortgage trends contribute to CAD direction; interest rate differentials remain a key driver – trade USD/CAD

Learn more about forex trading.

FAQs

Could UK mortgage interest rates go up or down?

Mortgage interest rates edged lower in 2025 after BoE cuts. If inflation slows further or growth weakens, more cuts are possible – which may lower mortgage rates. Conversely, if inflation rebounds or global risks rise, the BoE may pause or reverse course. Fixed rates also respond to swap-rate moves.

What is the forecast for mortgage interest rates?

Most third-party analysts see UK mortgage rates trending lower in the near term. CBRE projects average two-year fixed rates at 3.4 % by late 2025, Rightmove expects five-year deals near 4 %, and the OBR sees the average stock rate peaking at 4.7 % by 2028. Overall, forecasts place rates in the 3.5 – 4.5 % range over the next five years, subject to inflation and policy shifts.

How do UK mortgage rates affect CFD traders?

Shifts in UK mortgage rates reflect economic conditions and monetary policy – both critical for CFD markets. Falling rates can lift UK homebuilders and mortgage lenders; rising rates might benefit bank margins but depress housing demand. In forex, diverging rate paths between the BoE and other central banks can drive volatility in pairs such as GBP/USD.