Market Mondays: December starts with anticipation as Fed expectations reign

Markets enter December with anticipation as the Federal Reserve meeting will be a key risk event, with changing expectations driving market volatility

Last week’s holiday-shortened U.S. trading schedule did little to calm financial markets, as shifting expectations around Federal Reserve policy continued to dominate sentiment. With minimal fresh macroeconomic data, investors remained laser-focused on commentary from Fed officials and movements in rate expectations, factors that drove sharp swings across bonds, equities, currencies, and commodities.

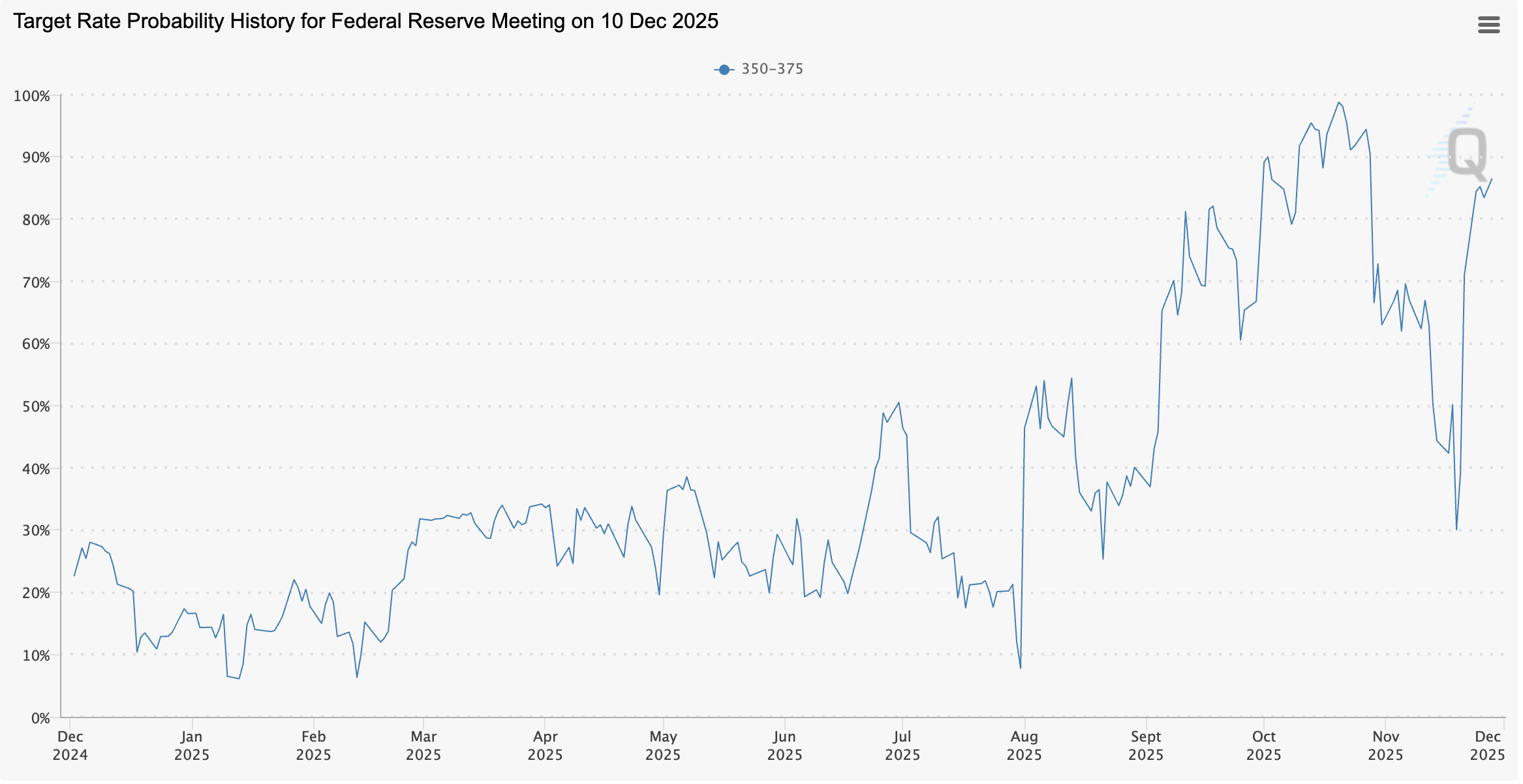

Repricing the Fed: December Cut Odds Surge to 87%

The CME FedWatch tool showed markets pricing in an 87% probability of a 25 bps rate cut at next week’s FOMC meeting. That sharp rise from just weeks prior—when expectations briefly dipped as low as 20%—has been a central driver of momentum in equities and bond yields.

Source: CME FedWatch

The repricing reflects two forces:

- Dovish Fed commentary over recent weeks, despite the lack of major economic releases.

- Longer-term expectations softening further following renewed speculation about who will chair the Federal Reserve next year. Odds have strengthened that Kevin Hassett—considered pro-growth and one of the most dovish potential candidates—could be Trump’s pick, with betting sites assigning roughly a 75% probability to his appointment.

The combination of near-term policy expectations and the prospect of a more dovish Fed leadership has reinforced the belief that U.S. rates could trend lower into 2025 and beyond.

Equity Market Reaction: A Fragile Rebound Meets Early-December Caution

Despite a strong recovery in U.S. indices last week, the tone turned cautious entering December. Futures pointed to a softer open, with traders debating whether recent gains were merely profit-taking after November’s rebound or a sign of deeper unease.

S&P 500 daily chart

Past performance is not a reliable indicator of future results.

Technically, key U.S. equity benchmarks are at a pivotal point:

- A break above recent lower highs would suggest momentum toward retesting record levels.

- Failure here would reinforce concerns that recent rallies are simply lower-high retracements within a broader volatile trend.

Investors are also grappling with a period of data scarcity. The Fed, too, has been “flying blind,” relying on internal measures while waiting for delayed government releases such as the September PCE report—now expected to show core inflation around 2.9%. Anything with a “3” handle could challenge the market’s aggressive rate-cut pricing.

Much of the discussion centres on the difficulty of steering inflation from the current 3% range down to the Fed’s 2% target. The sharp decline from the 2022 peak near 9% was the easy part—what remains is the “hard mile” of disinflation.

Forward-looking indicators, including ISM’s services sector prices paid index, continue to show persistent price pressures. This tension between market expectations and actual inflation dynamics means volatility may remain elevated until more clarity emerges.

FX Markets: Dollar Softens as Rate Expectations Shift

The U.S. dollar has pulled back in recent sessions, pressured by:

- Rising expectations of U.S. rate cuts

- Broad global currency strength driven by local catalysts

- Geopolitical developments such as tentative peace talks between Russia and Ukraine

The dollar index has notably rejected the 100 level and broken below a rising support trendline—raising questions about the durability of the recent USD recovery.

Key FX developments include:

Euro (EUR/USD)

The euro staged a notable rebound last week, supported by dollar weakness and upcoming Eurozone CPI data. Markets expect no change in headline (2.1%) or core (2.4%) inflation. Any surprise could spark volatility, influencing expectations for the European Central Bank’s path—though the ECB is largely expected to hold rates steady until mid-2026.

Japanese Yen (JPY)

The yen strengthened on speculation the Bank of Japan may finally raise interest rates as soon as December. Persistent inflation and expanded fiscal spending are piling pressure on the BOJ after years of ultra-loose policy.

AUD and NZD

Hot inflation in Australia pushed traders to price in the next RBA move as a hike, while the RBNZ signalled the end of its rate-cut cycle. Though less influential globally, these moves added to wider pressure against the USD.

US dollar index (DXY) daily chart

Past performance is not a reliable indicator of future results.

Oil: Extended Downtrend Amid Supply Reassurance and Soft Demand

Oil markets remain under significant downward pressure, marking one of the longest losing streaks since 2023.

Major drivers include:

Supply Factors

- Reduced geopolitical risk premiums, partly due to tentative Russia-Ukraine peace discussions.

- Rising U.S. production, adding to global supply.

- OPEC+ maintaining output quotas through 2026, signalling comfort with prices in the high-50s to low-60s range.

This pricing range achieves a balance between protecting market share and supporting fiscal revenues for major producers.

Demand Factors

Economies across the U.S., Europe, and China are slowing—not recessionary, but insufficient to signal strong energy demand ahead. China’s manufacturing sector is particularly weak, recording its longest contraction stretch on record.

While oil charts show early signs of buying support, any recovery faces stiff resistance from the persistent downtrend.

Anticipation, Not Reaction: Markets Are Front-Running Central Banks

A recurring theme across markets is that investors are not reacting to central banks—they’re anticipating them.

No major decisions have yet been made by the Fed or BOJ.

Markets are instead reacting to changes in expectations about upcoming moves:

- A December rate cut from the Fed

- o A potential rate hike from the BOJ