Market Analysis: oil rallies further as supply tightness dominates

Oil prices continue to surge as US sanctions on Russia and Iran are expected to tighten supply

Oil prices have surged recently, driven by expectations of new US sanctions on Russian oil exports. This shift in focus—from demand concerns to supply constraints—has bolstered oil prices significantly. As a result, US crude futures (WTI) have climbed over 9% since the start of the year, surpassing $76 for the first time in three months. Meanwhile, Brent futures have crossed the $80-per-barrel mark.

US crude (WTI) daily chart

Past performance is not a reliable indicator of future results.

Key Drivers of the Rally

1. Impending Sanctions on Russian Oil

The Biden administration is set to implement stricter sanctions on Russian oil exports ahead of Donald Trump's inauguration on January 20. These sanctions will target tankers carrying Russian oil priced above the $60-per-barrel cap imposed by the US and Europe. The anticipated restrictions are expected to disrupt Russian exports to major consumers like China and India, forcing them to seek alternative sources in Africa, the Middle East, and the Americas. This shift could increase shipping costs and further drive-up oil prices.

2. Additional Supply Concerns

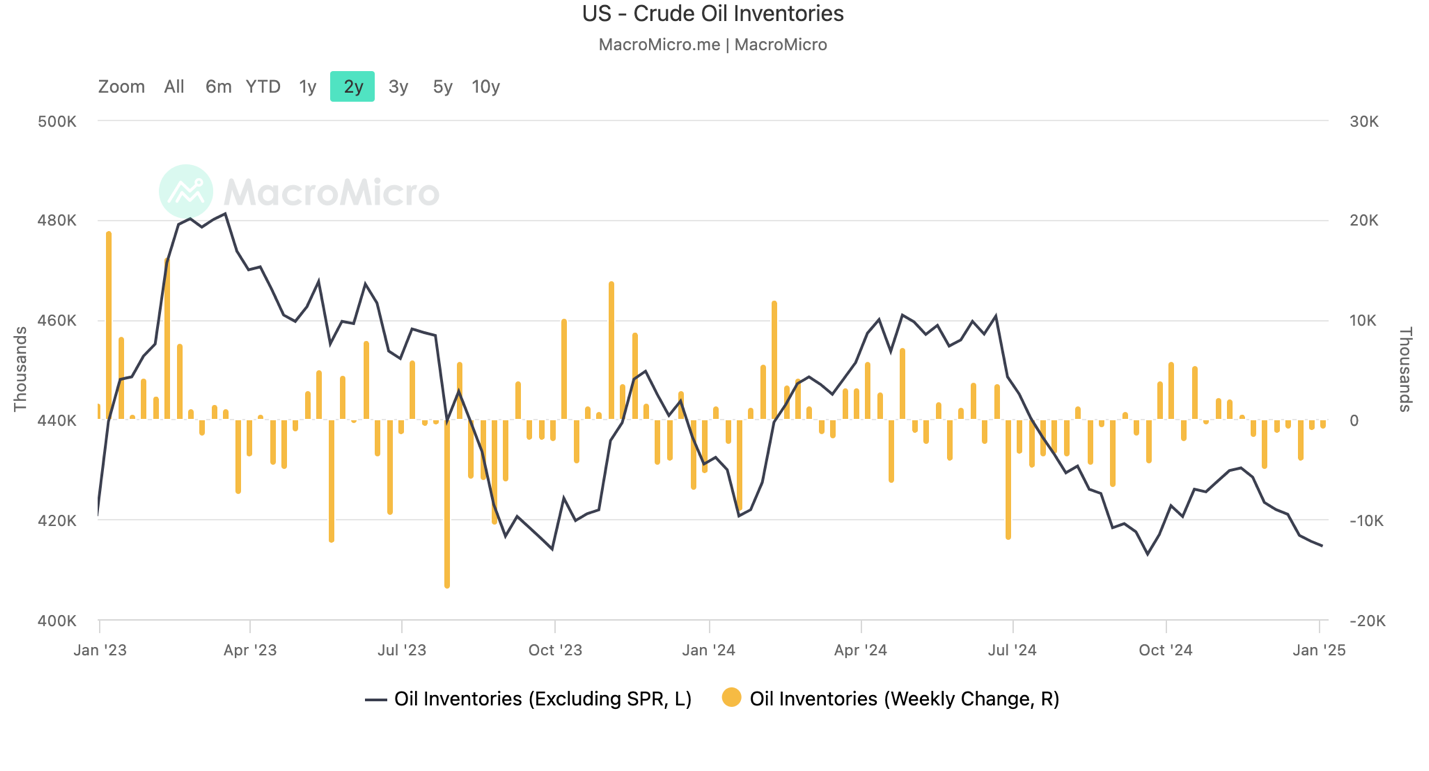

Further supply disruptions are anticipated as Donald Trump plans to reinforce restrictions on Iranian oil exports upon taking office. Additionally, rumours suggest a potential decrease in Saudi Arabian output this month. Compounding these factors, US crude inventories have declined for seven consecutive weeks, with a 950,000-barrel drop last week alone. This ongoing reduction in supply continues to tighten the market.

Economic Environment

The supply tightness coincides with modest improvements in global economic conditions. Positive data from China and the Eurozone, coupled with the sustained resilience of the US economy, suggest that oil prices may have moved beyond their recent consolidation phase. For instance, WTI has risen above its $66 threshold, and Brent has surpassed the $70 mark—both key levels identified by OPEC+ as the minimum acceptable benchmarks.

Technical Outlook

From a technical perspective, the bullish momentum appears overextended. The Relative Strength Index (RSI) has entered overbought territory, a level not seen since April last year when WTI traded at $85 per barrel. This could signal a potential short-term correction; especially as daily candlestick patterns reveal selling pressure at higher price levels. However, any correction is likely to be brief unless there are significant changes to the fundamental drivers of supply tightness.