ECB Preview: Higher CPI expected to keep Lagarde on a hawkish path

ECB Preview: Higher CPI expected to keep Lagarde on a hawkish path

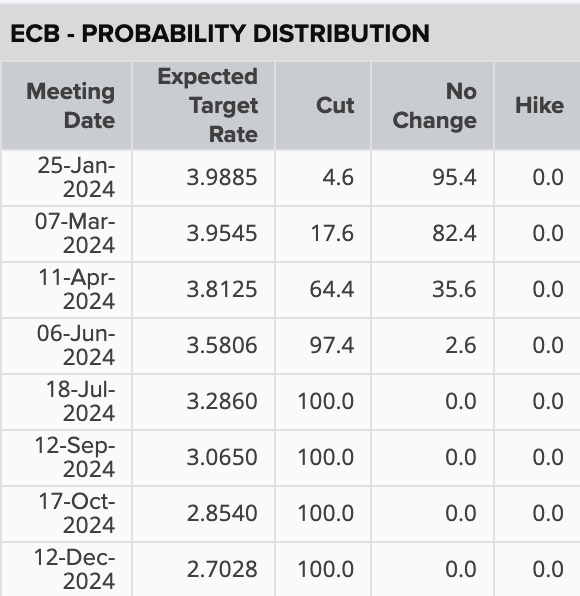

The European Central Bank (ECB) will be hosting its first meeting of the year on Thursday, 25 January. As per data from Reuters, markets are convinced that the central bank will not change its interest rates, with a 95% chance priced in 24 hours before the decision is revealed.

Thinking about how things have evolved since the last meeting, this seems like a pretty good bet. Back in December, the Governing Council had somewhat of a green light to start sounding more dovish and reference the plan for cutting rates after the Federal Reserve had done just that the day prior. It is important to remember that inflation remains higher in the US and the economy managed to grow almost 5% in the third quarter, a stark contrast to the euro area which saw a contraction of 0.1% in the same quarter. So, the feeling was if the Fed could turn dovish with high inflation and stronger growth, then surely the ECB has enough reason to do so too.

But Lagarde surprised many by not only failing to sound more dovish but also pushing back on any plans of cutting rates any time soon. So, flashforward to January and the latest data has shown that inflation rose in December to 2.9%, getting further away from the 2% long-term target. Just this fact alone should be enough to convince anyone that Lagarde will continue to be hawkish at this meeting, at least until she gets more clarity on where CPI is going.

But just in case higher inflation is not enough, recent commentary from members of the Governing Council would be the final nail in the coffin of dovish hopefuls. The key takeaway from the appearances at the World Economic Forum in Davos last week was that rate cuts are likely the next move from the ECB. But there is no clear plan as to when they will start, as it is too early to declare victory on inflation. Dutch Central Bank chief Klaas Knot went as far as to say that rate cuts in the first half of the year are unlikely, suggesting the first possible rate cut could come in July. Markets are currently pricing in a 64% chance of a 25bps cut in April.

Source: refinitiv

Knot also added that geopolitical tensions could pose a risk to inflation and that the labour market remains tight. On market expectations, he mentioned that the more markets ease financing conditions, the less need there is for the ECB to cut rates, possibly pushing back the decision even further. Finnish policymaker Tuomas Valimaki also reinforced views that the ECB will hold on cutting rates for the foreseeable future as he mentioned the central bank should not jump the gun on rate cuts, and it is better to wait a bit longer than exit prematurely.

What’s going to be most tricky for the ECB is to offer forward guidance at a time when it is still unclear at which stage of the cycle the economy is in. Despite the stubbornness in the disinflation process, growth data has started to show concerns about the future path of the economy, with both industrial production and consumer spending taking a tumble in recent months. Analysts are also forecasting GDP to have contracted 0.1% again in the fourth quarter, which would put the euro area in a technical recession.

At this point, the balance between keeping policy restrictive enough to limit a resurgence in price pressures and making sure growth is not too constricted is very delicate. Lagarde has made it clear that there is still more information needed surrounding supply chains, energy prices, and wage growth to decide on when to cut rates, which suggests little is likely to happen at the meeting this week.

The key focus will be on the press conference to get a gauge of how confident they are at telling us what they believe the direction of travel for rates will be this year. This is likely where the majority of the market momentum will come from. How central banks compare to one another is still a key driver in FX markets. So if the ECB is still perceived to be more hawkish than the Federal Reserve, then EUR/USD could see a resurgence in the recent bullish rally. Whilst least likely, if Lagarde and her team are seen to offer more dovish commentary, or if they start to acknowledge the likelihood of rate cuts in the near future, then the euro would likely tumble, with EUR/USD playing into the US dollar’s recent strength, potentially dropping below 1.08 once the 200-day SMA (1.0844) is cleared.

EUR/USD daily chart

Past performance is not a reliable indicator of future results.