Cooling but not cracking: The UK’s delicate economic balance

The UK economy is showing signs of fatigue with minimal growth and a slowing labour market, but inflation still remains above target.

The latest UK labour market and inflation releases have painted a picture of an economy that is cooling but not collapsing. The combination of rising unemployment, slowing wage growth and mixed inflation signals is shifting expectations for monetary policy, and in turn shaping the near-term outlook for UK assets.

A cooling labour market signals economic fragility

The labour market data showed unemployment ticking higher while payroll employment softened, reinforcing the narrative that hiring momentum is fading. Wage growth also eased compared to previous readings, suggesting that domestic inflationary pressure from earnings is gradually moderating.

This is significant because the UK economy has already been growing at a very modest pace. With GDP barely expanding in recent quarters, a softening jobs market increases the risk that consumer spending, a key driver of UK growth, weakens further in the months ahead.

In short, the labour data signals that the economy is losing steam. It does not point to a sharp downturn yet, but it clearly reflects reduced labour demand and a shift away from overheating conditions.

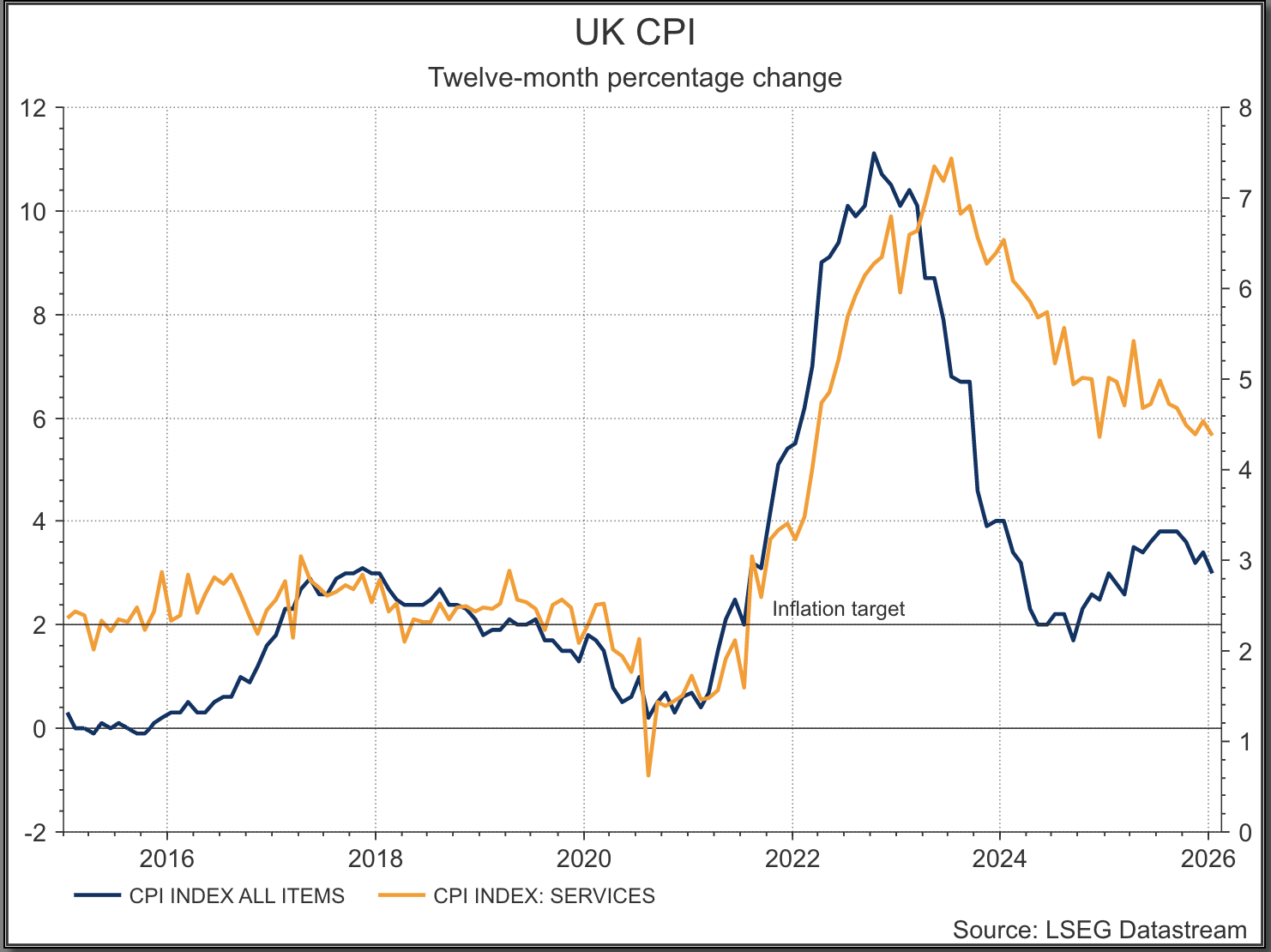

Inflation: encouraging but not yet mission accomplished

The inflation picture is more nuanced. Headline CPI eased, confirming that overall price pressures are moderating. However, core CPI remains above 3% year-on-year, even though the month-on-month core reading came in at -0.6%.

This combination tells us that inflation momentum is weakening in real time, but the annual rate remains elevated due to base effects and previous price increases. The negative monthly core reading is particularly important as it suggests underlying price pressures may be easing more quickly than the annual figure alone would imply. For policymakers, this is cautiously encouraging. It reduces the risk of a renewed inflation surge but does not yet give the Bank of England full confidence that inflation is sustainably returning to its 2% target.

UK Headline CPI and Services CPI

What this means for the Bank of England

The combined message from labour and inflation data is clear: the economy is cooling and price pressures are gradually moderating. Market pricing reflects this shift. Current implied rate expectations suggest investors are anticipating steady easing through 2026, with rate cuts gradually priced in across successive meetings. Implied rates fall from the current 3.75% to just above 3.5% in March and roughly 3.23% by year-end, indicating expectations of two 25bp cuts over the next ten months.

The Bank of England is unlikely to rush, particularly given core inflation remains above target. However, the balance of risks is tilting toward easing rather than further tightening. If labour market slack continues to build and monthly inflation readings remain soft, a cut in the coming months becomes increasingly likely. The key risk to this outlook would be a reacceleration in services inflation or wage growth, neither of which is currently evident.

GBP/USD: dollar-driven, but fundamentally fragile

GBP/USD has been trading largely as an inverse reflection of dollar dynamics rather than strong domestic fundamentals. The pair recently rallied toward the 1.38–1.39 region before retracing lower. Technically, the pair has slipped back below short-term momentum levels and is hovering near 1.36. The 50-day moving average is acting as near-term support, while resistance now sits around 1.3650 -1.37. The RSI has cooled toward neutral territory, suggesting a loss of upside momentum.

From a macro perspective, the divergence between the UK and US outlook is becoming clearer. The US economy remains stronger, while the UK faces stagnation risks. If markets continue pricing earlier or deeper Bank of England cuts relative to the Federal Reserve, sterling may struggle to sustain rallies. In the near term, GBP/USD could remain range-bound between 1.34 and 1.38, but risks are tilted slightly to the downside if rate expectations shift further in favour of the dollar.

GBP/USD daily chart

Past performance is not a reliable indicator of future results.

FTSE 100: benefiting from sterling weakness and global exposure

The FTSE 100 has continued its steady uptrend, recently pushing toward the 10,600 region. The index remains comfortably above its key moving averages, and momentum indicators are elevated but not yet extreme. Unlike domestically focused indices, the FTSE 100 tends to benefit from sterling weakness due to its heavy weighting in multinational exporters, energy and commodity firms. A softer pound improves overseas earnings when translated back into GBP.

Additionally, if the Bank of England moves toward easing, lower borrowing costs and improved financial conditions could further support equities, particularly in yield-sensitive sectors. However, upside momentum may slow if global risk sentiment deteriorates or if UK growth concerns intensify.

FTSE 100 daily chart

Past performance is not a reliable indicator of future results.