US CPI Preview: Inflation data to test Fed’s tariff assumptions and policy expectations

US CPI data could impact the Fed's views on tariffs, inflation and monetary policy

Markets are turning their attention to the June US Consumer Price Index (CPI) report, the 15th of June, with expectations that the data could significantly influence the Federal Reserve’s next policy steps. Amid threats of new tariffs, the inflation print is a critical signal for the direction of US monetary policy heading into the second half of the year.

Modest reacceleration in inflation expected

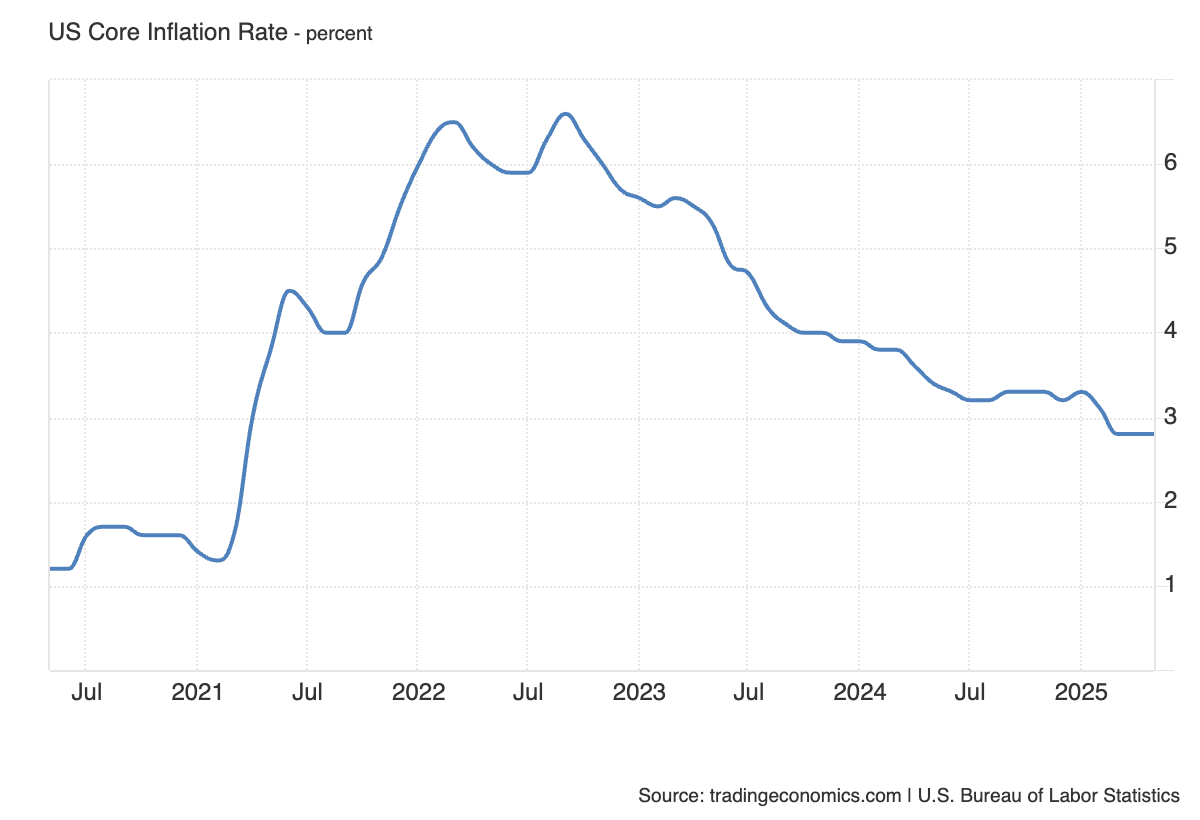

Economists forecast a slight uptick in both headline and core CPI. Headline inflation is expected to rise from 2.4% to around 2.6% year-on-year, while core inflation—excluding food and energy—is projected to increase from 2.8% to 2.9% . On a monthly basis, core CPI is anticipated to accelerate from 0.1% to 0.3%.

These expectations reflect mounting concerns that tariffs, which have so far had limited visible impact on consumer prices, could begin to push inflation higher. The assumption is that businesses may now be moving beyond the phase of absorbing costs and running down inventories, and are beginning to pass those costs on to consumers. While this hasn’t yet shown up in a sustained way in the data, the CPI print for June could mark the start of that transition.

(Source: Trading Economics)

Tariffs have been disinflationary—so far

Despite the risk narrative, the actual inflationary impact of tariffs has remained limited. In fact, recent evidence has suggested a slightly disinflationary effect, with weaker demand helping to offset potential supply-side cost pressures. In sectors like services, price growth has either softened or outright declined in recent months.

One explanation is that many firms have delayed price hikes, anticipating that tariff threats might be walked back or watered down. Additionally, businesses have been running through existing inventories, avoiding the need to pay higher prices for imported goods affected by new duties. However, that buffer may now be running thin. If tariffs remain in place—or are escalated further—companies may have no choice but to begin adjusting prices upward.

A pivotal moment for Fed policy

The upcoming CPI print arrives at a delicate time for the Federal Reserve. The central bank has held off on further rate cuts, in part because of expectations that tariffs will cause a one-off lift in inflation. While this view has yet to be validated by the data, it remains a key part of the Fed’s current policy framework.

If the June CPI data comes in cooler than expected once again, it would cast further doubt on that assumption. A soft reading could increase the likelihood of renewed policy easing, especially if paired with any signs of weakening demand or labour market softening. Conversely, a stronger-than-expected print would reinforce the Fed’s current pause and reduce the odds of rate cuts in the near term. Currently, the next cut is fully baked in for the November meeting.

(Source: CME Group)

The labour market adds further complexity. Recent non-farm payrolls data showed a surprise drop in the unemployment rate to 4.1% and moderate jobs growth, although wage growth and broader participation metrics have not shown the kind of strength that would normally drive persistent inflation. This leaves the Fed in a position where it may not feel compelled to cut rates given resilient labour market conditions.

Markets debate the timing of the next Fed cut

The CPI release also has important implications for broader market pricing. A significant portion of the optimism seen in risk assets over recent months has been underpinned by expectations that inflation will remain contained, allowing the Fed room to cut rates if needed. At the same time, there is growing uncertainty around US trade policy, with an array of new tariffs announced in the past fortnight, including an up to 30% rate on European goods and even steeper rates for copper.

If inflation data surprises to the upside, it could lead markets to reassess the likelihood of near-term rate cuts, lifting the US Dollar and weighing on equities and rate-sensitive sectors. On the other hand, another downside miss could reinforce the disinflationary narrative and trigger a rally in risk assets, as the prospect of Fed easing returns to the fore.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)