Tightening Liquidity Is Becoming a Problem for Risk Assets

Liquidity in the market has been tightening in recent months as the Federal Reserve’s reserve balances have fallen sharply.

This decline follows the increase in the Treasury General Account—the US government's checking account—after the debt ceiling agreement in mid-July.

Consequently, reserve balances at the Fed have dropped below $3 trillion, putting pressure on the overnight funding market. This is reflected in the increased use of the Standing Repo Facility and the widening of spreads on secured overnight financing rates (SOFR).

Tighter Liquidity Conditions

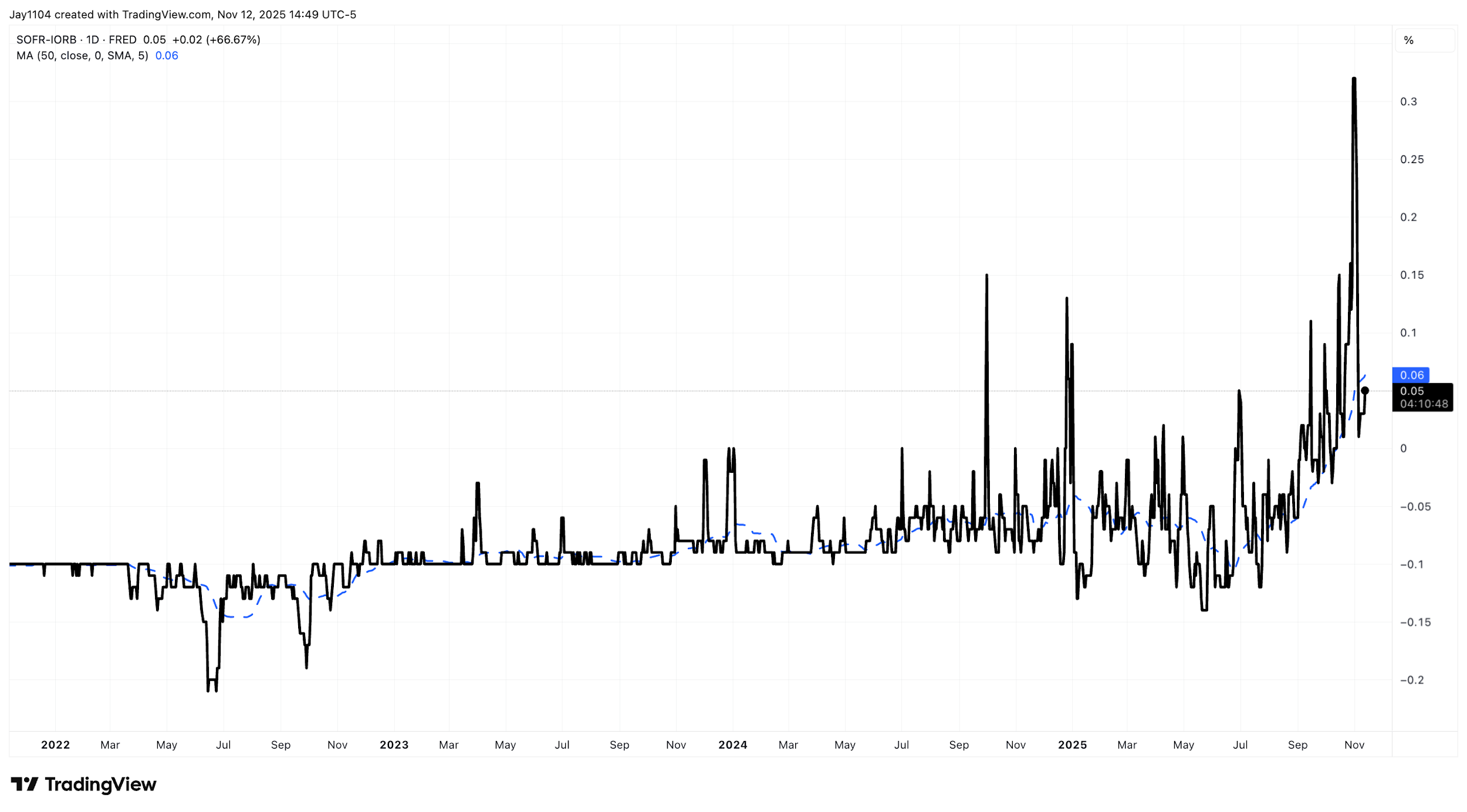

Secured overnight financing rates are best assessed as a spread over the interest on reserve balances, the effective federal funds rate, or the Standing Repo Facility rate. In all these cases, spreads have widened significantly. More importantly, the volatility of these spreads has risen markedly — another clear indicator of stress emerging in the overnight funding market.

After years of these spreads being relatively tight, with very little daily movement, volatility began to pick up in July, when the Treasury began issuing more Treasury bills and increasing the size of the Treasury General Account.

(Source: TradingView)

Past performance is not a reliable indicator of future results.

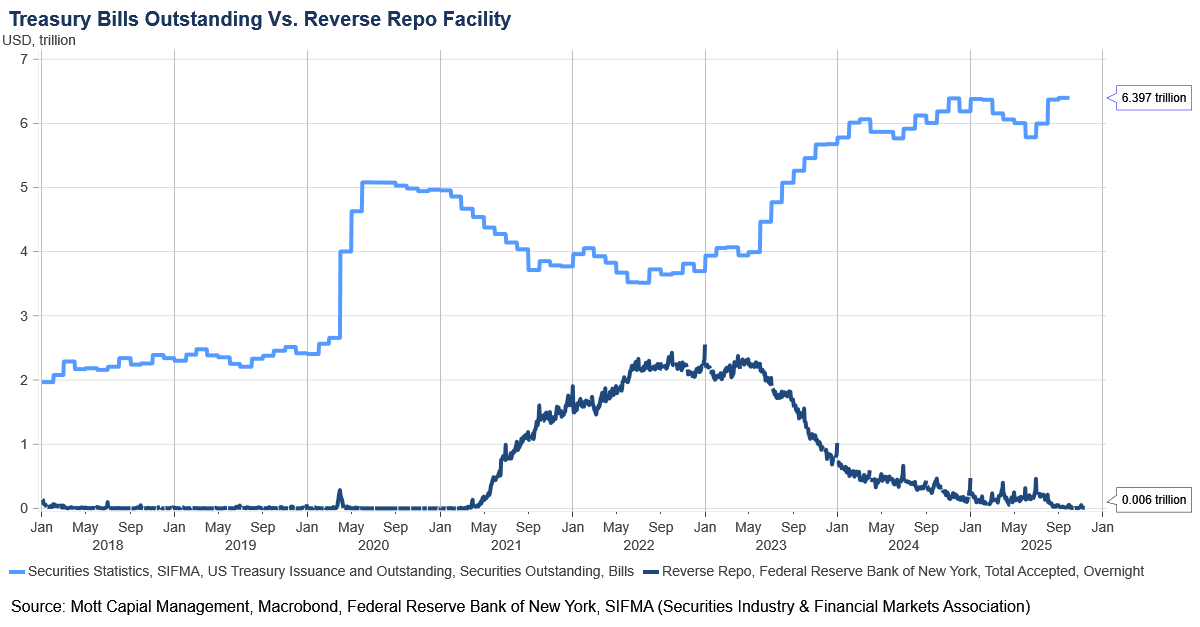

Additionally, the Fed’s Reverse Repo Facility, which institutions use when they have excess cash and are looking to earn interest, has been nearly exhausted, with usage dropping to almost zero. This decline has been caused by a significant rise in Treasury bill issuance, which has absorbed the excess liquidity that the facility once absorbed.

(Source: TradingView)

Past performance is not a reliable indicator of future results.

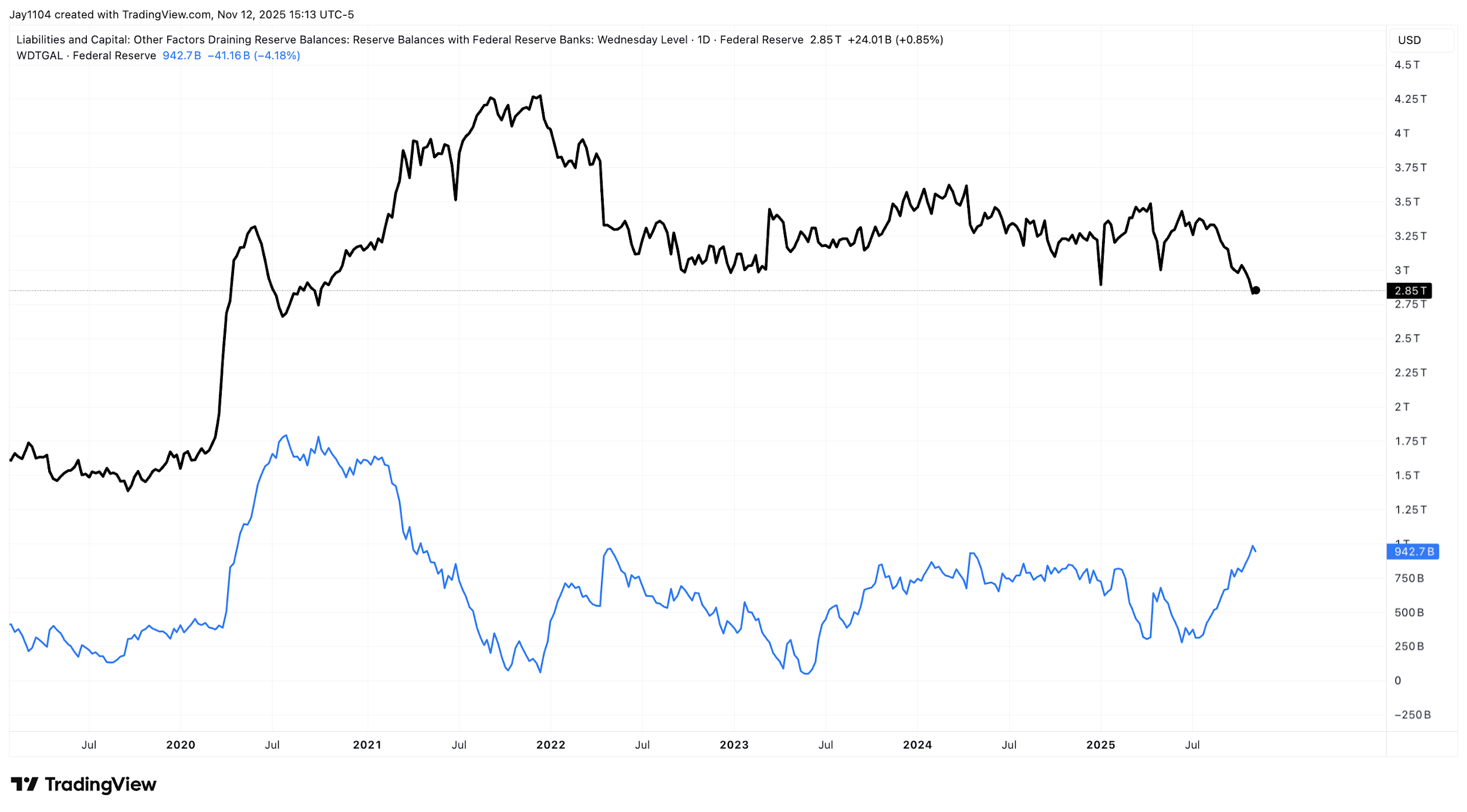

Because the TGA is a liability on the Fed’s balance sheet, as it rises, it reduces the reserve balances held at the Fed by depository institutions. Therefore, as the TGA rose, reserve balances fell, reducing overall liquidity. When reserves are abundant, overnight funding spreads remain tight and are not volatile. As reserves fall and liquidity conditions worsen, these spreads between SOFR and the Fed’s policy benchmarks widen and volatility rises.

(Source: TradingView)

Past performance is not a reliable indicator of future results.

Risk Assets May Struggle

Due to these tighter liquidity conditions, risk assets, as reserve balances are unlikely to grow in the near future, even if the Fed ceases quantitative tightening on 1 December as currently planned. A significant improvement in liquidity conditions would likely require a period of actual balance sheet expansion or the Treasury opting to reduce the size of the TGA; however, a decline in the TGA's value seems unlikely, as the Treasury is targeting a balance of $850 billion.

The main reason liquidity conditions are unlikely to improve until the Federal Reserve resumes expanding its balance sheet is that the US Treasury will keep issuing debt. That debt must be financed through settlement cycles, which can occur 2 to 3 times a week. When settlements are large, they put more pressure on market liquidity, pushing up overnight funding rates and making them more costly. As a result, market liquidity declines, increasing pressure on risk assets.

Currently, this suggests that liquidity in the overnight funding markets has become very tight, putting pressure on risk assets. This tightening has also begun to affect other parts of the equity market, though it is less evident when examining only the S&P 500. The equal-weighted index has shown more significant weakness, as have sectors such as housing and private equity.

Overall, the ongoing stress in overnight funding markets is likely to pressure risk assets for some time, or at least until the Federal Reserve resumes balance sheet expansion.