Market Mondays: Trade Uncertainty Returns as Geopolitical Risks Ease

The markets move pass geopolitical risk as attention returns to US trade policy and upcoming US jobs data

After weeks of markets trading under the weight of geopolitical uncertainty, attention is shifting back to trade policy — particularly as the 90-day tariff truce approaches its July 9 expiry. While risk appetite has recovered following a fragile ceasefire between Iran and Israel, the looming deadline for new U.S. tariffs is beginning to dominate the macro narrative once again.

Equities are climbing that familiar wall of worry, supported by hopes of a favourable outcome to ongoing trade negotiations, resilient U.S. data, and a Federal Reserve still signalling rate cuts despite sticky inflation.

Wall Street breaks to new highs — but risks are asymmetrical

U.S. equities rallied to fresh record highs last week, erasing all of the post–Liberation Day losses and reaffirming the market’s underlying bullish trend. Optimism is being fuelled by assumptions that the Trump administration will finalise a series of trade deals, with average tariff rates settling somewhere near the low teens — far below the initial Liberation Day levels.

A framework agreement on rare earths and technology transfer between the U.S. and China last week lifted sentiment, with markets largely interpreting it as a step toward a broader resolution. But while the base case remains constructive, the risk is clearly asymmetric. Any sign of talks collapsing — particularly if paired with an abrupt hike in tariffs — would likely trigger a pullback.

Moreover, the rally has once again been narrowly concentrated in large-cap tech. While the S&P 500 and Nasdaq have surged to new highs, the Dow Jones remains below its peak, suggesting cyclicals are lagging amid lingering concerns about the growth impact of tariffs.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

European equities lag on trade concerns

Despite improved global sentiment, European equity markets have struggled to match U.S. momentum. The DAX, FTSE 100 and Stoxx 600 remain below their highs, reflecting relative underperformance as trade tensions with the EU emerge as a potential headwind.

Trump has repeatedly described the EU as a “difficult negotiating partner,” and markets are beginning to price in a higher risk of disruption for European exporters. Although concessions are still possible and a breakdown appears unlikely at this stage, traders are mindful that the next phase of trade talks could prove more politically sensitive.

Technical indicators are mixed. The RSI on major European indices remains below neutral, signalling hesitation despite improved risk appetite elsewhere.

U.S. data in focus: Jobs and inflation dynamics

On the data front, all eyes will be on Thursday’s U.S. non-farm payrolls report — moved forward due to the Fourth of July holiday. While the labour market has remained resilient, recent data has shown signs of softening. Job growth is expected to remain in the low 100,000s, with the unemployment rate possibly ticking up to 4.3%.

That backdrop is critical as markets assess how the Fed will respond. Despite core PCE inflation rising to 2.7% in May — above expectations — the Fed continues to project two rate cuts this year, with headline inflation forecast to move above 3%. The takeaway: the central bank is likely to look through moderate price pressures if labour market conditions deteriorate.

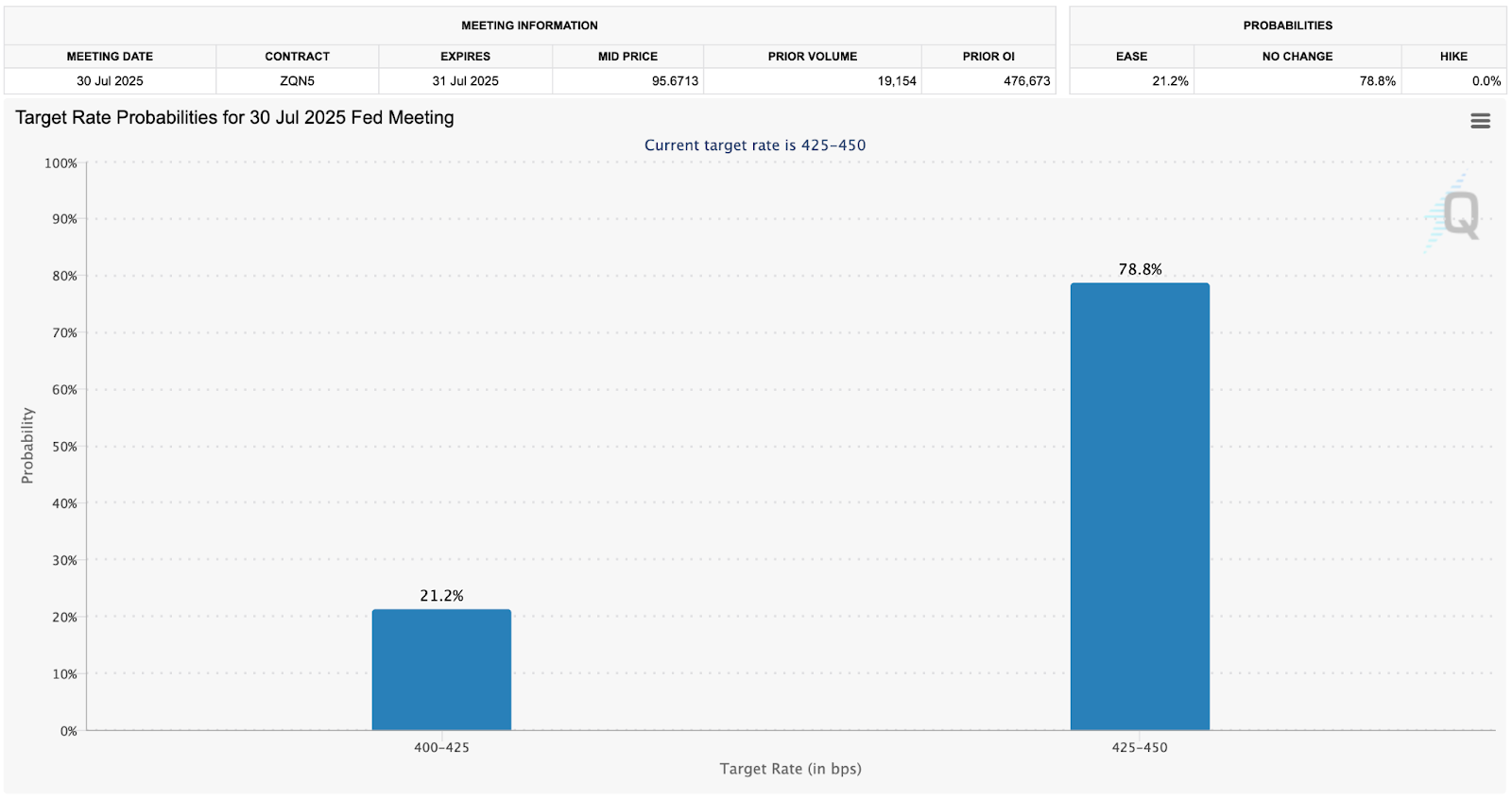

Markets are now pricing in a roughly 20% chance of a July rate cut, with expectations firming for action by September. That’s a shift from earlier in the year, when inflation was running hotter and the Fed was seen staying on hold. Stronger payrolls could revive the "higher-for-longer" narrative, while a downside surprise would likely increase the probability of cuts in the second half of the year.

(Source: CME Group)

Eurozone inflation in focus, but ECB likely to hold steady

In Europe, the focus turns to preliminary CPI figures due Tuesday. Markets expect headline inflation to tick up slightly from 1.9% to 2%, with core remaining steady at 2.3%. However, the monthly figures may prove more telling — after May's flat month-on-month readings suggested a sharp deceleration in price growth.

German inflation data, released Monday, is expected to strengthen marginally, but the broader takeaway is likely to be one of subdued price pressures. The ECB has already delivered two cuts this year and is in no rush to act again. Market pricing currently implies an 88% chance of no change at the July 24 meeting, and even a downside inflation surprise is unlikely to shift that view meaningfully.

The euro has rebounded against the dollar, benefitting from a weaker USD and structural flows tied to de-dollarisation. However, gains have been more muted against other currencies, such as GBP, indicating the rebound has more to do with U.S. dynamics than European fundamentals.

Gold loses momentum despite supportive macro backdrop

Gold has come under pressure in recent sessions, falling below its 50-day moving average and losing momentum despite a weaker dollar and higher inflation. The failure to break through the $3,400–$3,500 resistance zone has triggered a technical pullback, with the RSI now confirming bearish momentum.

While long-term tailwinds remain — from macro uncertainty, fiscal dominance, and reserve diversification — price action suggests markets are reassessing short-term valuations. A break toward the $3,200 zone is possible if buyers don’t re-emerge, though the $3,000 level still looks like critical long-term support.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

Oil stabilises as risk premium fades

Crude oil has also drifted lower after an initial spike on Middle East tensions. The market quickly retraced after concluding that recent U.S. airstrikes on Iranian nuclear sites were unlikely to trigger a broader escalation. A potential increase in OPEC production and the absence of major supply threats have also reduced upside pressure.

Oil is now trading back below $65 per barrel, with technical support seen in the low $60s. For a renewed rally, markets would need to see clear signs of regional escalation, U.S. military escalation, or serious threats to Strait of Hormuz shipping. Barring that, prices are likely to remain range-bound in the $64–$75 corridor.