Magnificent Seven Earnings Primer: MSFT, META, GOOG

Microsoft, Meta Platforms, and Alphabet account for roughly 13% of the S&P 500’s market capitalisation

The next round of Magnificent Seven companies report after the Wall Street close on Wednesday, October 29th, 2025.

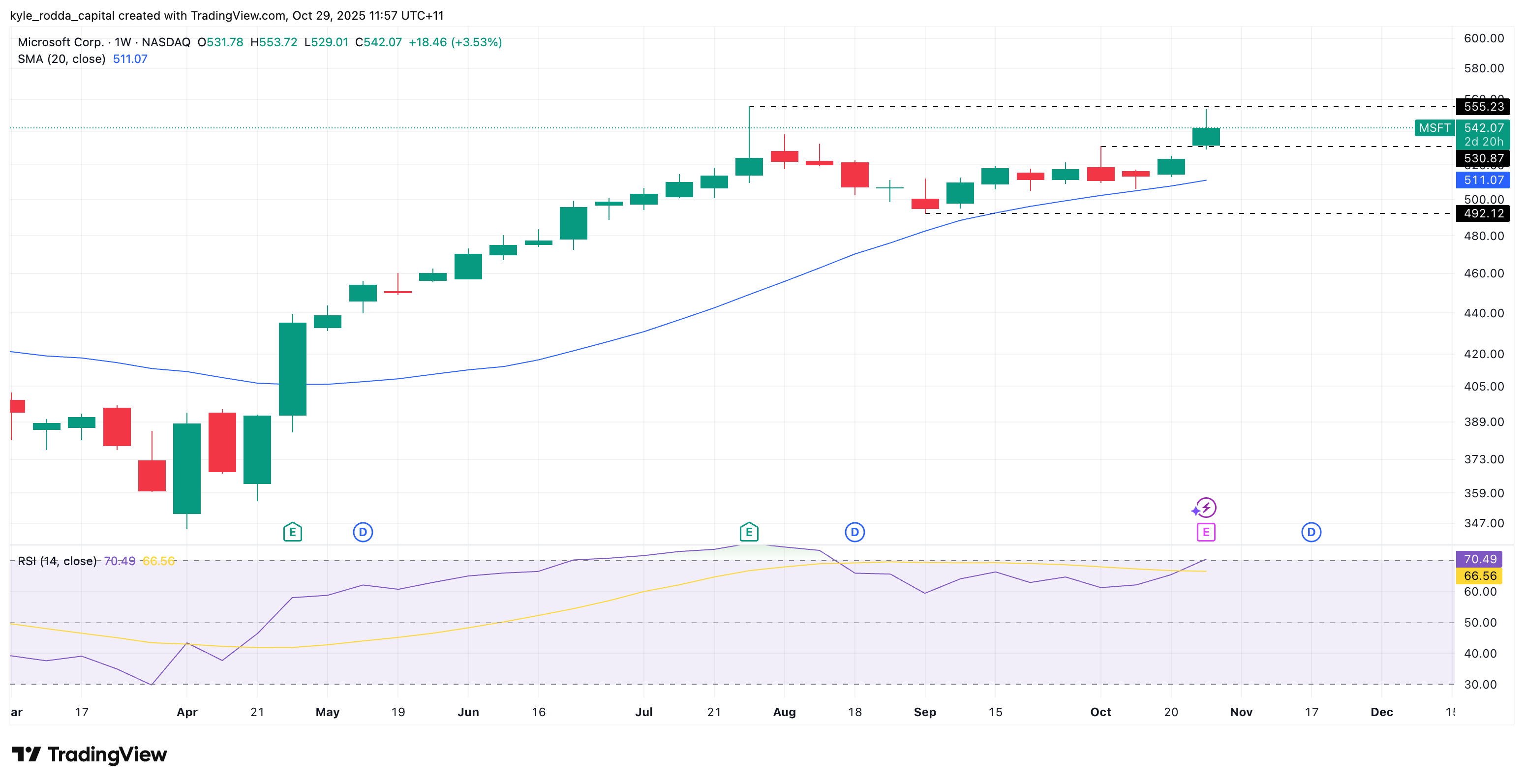

Microsoft: AI demand sustains growth as capex remains elevated

Microsoft’s fiscal Q1 2026 results are expected to underscore its continued leadership in enterprise cloud and AI infrastructure. Consensus estimates call for adjusted EPS of $3.68 on revenue of $75.55 billion, reflecting modest quarter-on-quarter growth. Revenue expansion remains anchored in Azure and Office 365, both benefiting from strong adoption of AI-enhanced services. However, growth is being tempered by a slowdown in traditional software licensing and foreign-exchange headwinds. Microsoft’s margins are steady, supported by subscription pricing power, though record capital expenditure—over $44 billion last quarter—signals sustained investment in data-centre expansion. Looking ahead, the key growth driver remains enterprise AI demand and integration across the Microsoft ecosystem, from Copilot tools to cloud infrastructure, positioning the firm to capture productivity-driven spending in 2026.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

Meta Platforms: Ad growth resilient but cost pressures mount

Meta’s Q3 2025 results are forecast to show strong, albeit moderating, growth following several robust quarters. Analysts expect adjusted EPS of $8.43 and revenue of $49.57 billion, up 22% year-on-year. Ad revenue remains the primary driver, underpinned by improved targeting efficiency and ongoing user engagement gains on Instagram and Reels. While growth in ad impressions continues to offset lower pricing in some markets, operating expenses linked to AI model training and data-centre upgrades are expected to pressure margins. The company’s Reality Labs division remains a long-term play, contributing to near-term cost volatility. Future growth will hinge on AI-powered recommendation systems, video monetisation, and expanding commerce integration across its platforms. Analysts view Meta as well positioned to leverage AI in ad delivery, though cost discipline and regulatory scrutiny will remain key themes into 2026.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

Alphabet: Search steady as AI competition intensifies

Alphabet’s Q3 2025 earnings are expected to highlight stable growth across its core businesses, with adjusted EPS forecast at $2.68 and revenue of $85.1 billion. That represents annual revenue growth of roughly 14%, driven by sustained momentum in YouTube and cloud services, offsetting gradual saturation in traditional search advertising. The company’s investments in AI infrastructure and Gemini-integrated search tools are central to future growth, though near-term returns remain modest as monetisation models evolve. Past quarters have been supported by disciplined cost control and resilience in digital ad demand, while the outlook hinges on whether Alphabet can balance AI innovation with profitability. Investors will watch closely for commentary on cloud growth, AI deployment in Google Workspace, and ad-market share retention as generative AI reshapes the competitive landscape.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)