FOMC Decision Preview

As the US Federal Reserve prepares for its most significant decision since ending the rate hike cycle in mid-2023, the balance of risks has shifted. With inflation stabilizing at 2.6% and rising unemployment at 4.2%, the FOMC faces increasing pressure to address employment concerns. Markets anticipate a rate cut, with debate on the extent of the reduction.

This week’s decision by the FOMC is the most consequential since the US Federal Reserve ended its rate hiking cycle in the middle of 2023. According to market pricing, a cut is fully priced-in, with the markets split on the size of the cut.

Balance of risks for the US economy shifts

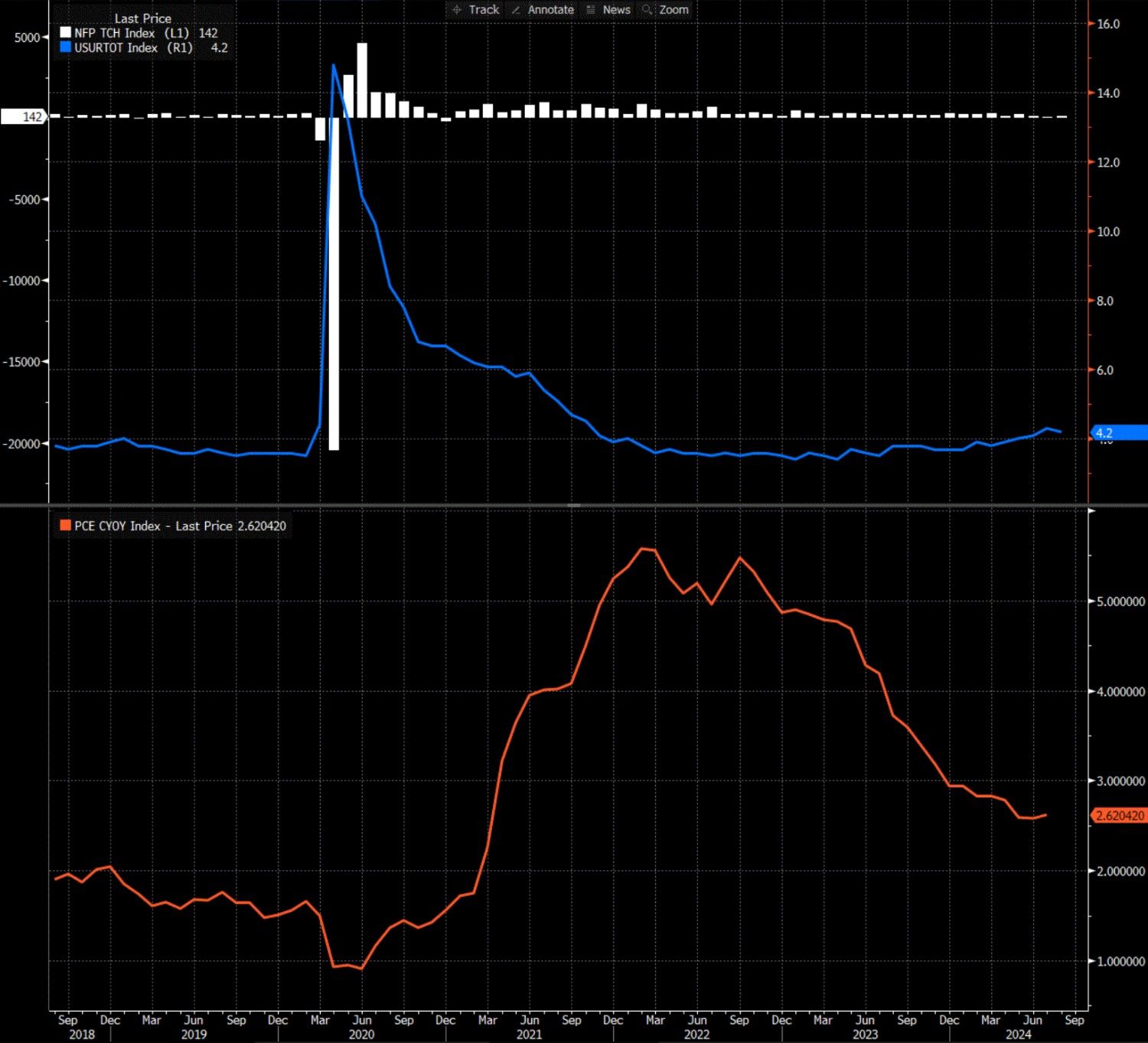

The balance of risks to the US economy have shifted in recent months, with price stability giving way to employment as the Fed’s more pressing issue. Although the latest inflation data revealed that annual core PCE remains around 2.6% and above the Fed’s target, the central bank has expressed “greater confidence” that inflation is on the path back to 2%. In addition, signs of softness in the labour market signals weaker demand and diminishing price pressures in the US economy. The two Non-Farm Payrolls reports since the last FOMC decision surprised to the downside and revealed a pick-up in the unemployment rate to 4.2%. On top of that, the data came with downgrades to previous month’s figures, with a massive annual downgrade of 818,000 jobs by the Bureau of Labor Statistics in August hinting at a much weaker jobs market than previously thought.

(Source: Bloomberg)

Given this backdrop, Federal Reserve Chairperson Jerome Powell used his Jackson Hole speech last month to prime the markets for rate cuts and frame the Fed’s new thinking about future policy. “The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks”, Powell said.

Futures point to line ball call with focus on policy outlook

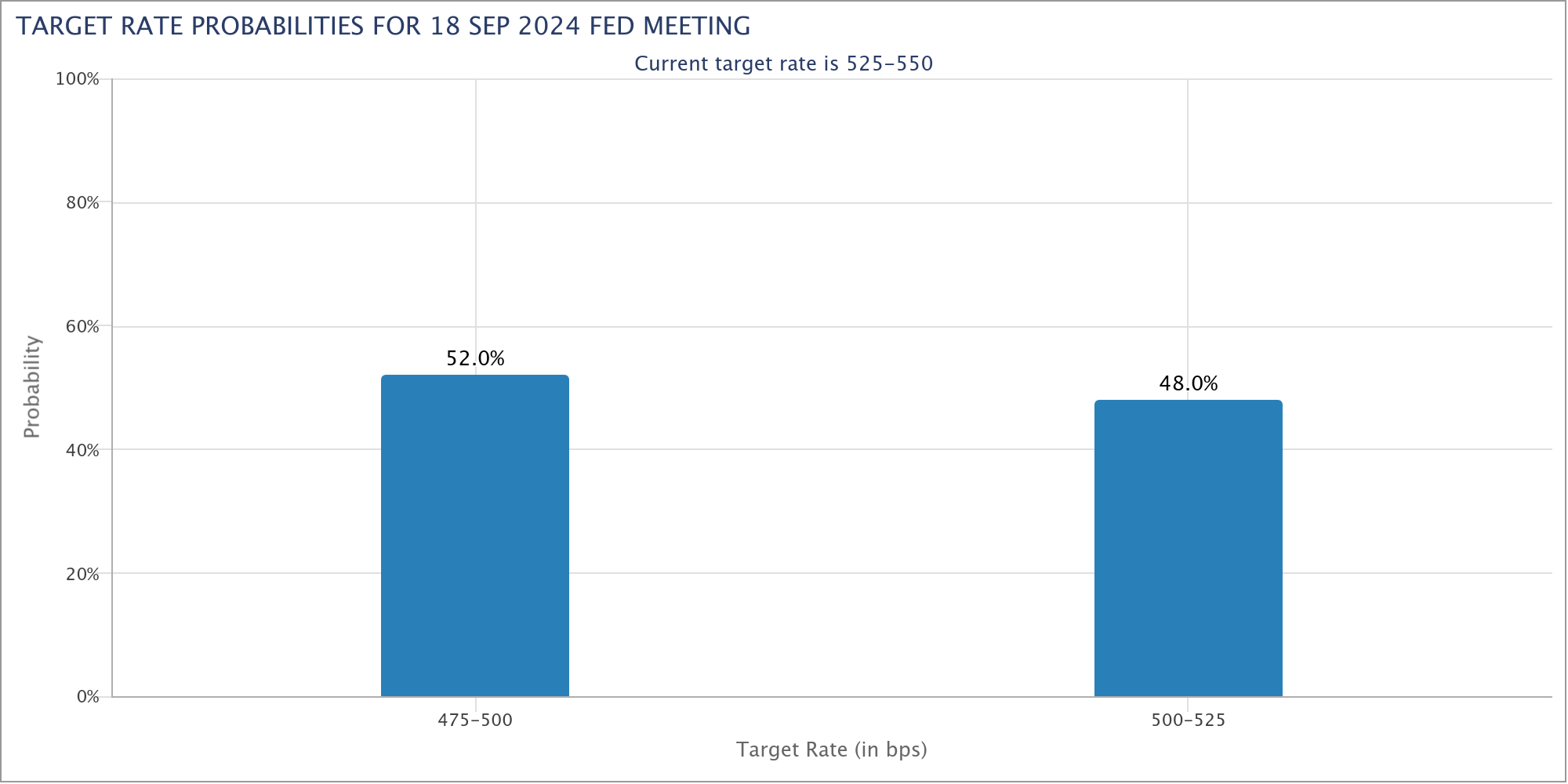

As of the end of last week, markets are split on the outcome of this FOMC decision. A 50 point cut is considered more probable but only by the finest margin. On top of that, the Fed’s guidance will also be crucial; even when the odds of a 50 basis point cut have receded in recent weeks, the markets have stuck to the view that the central bank will reduce rates by 100 basis points this year. That means that if the Fed doesn’t cut by 50 basis points at this meeting, the expectations for such a “jumbo” may consolidate for either November or December meeting, depending on whether the Fed pushes back on the notion of such aggressive easing.

(Source: CME Group)

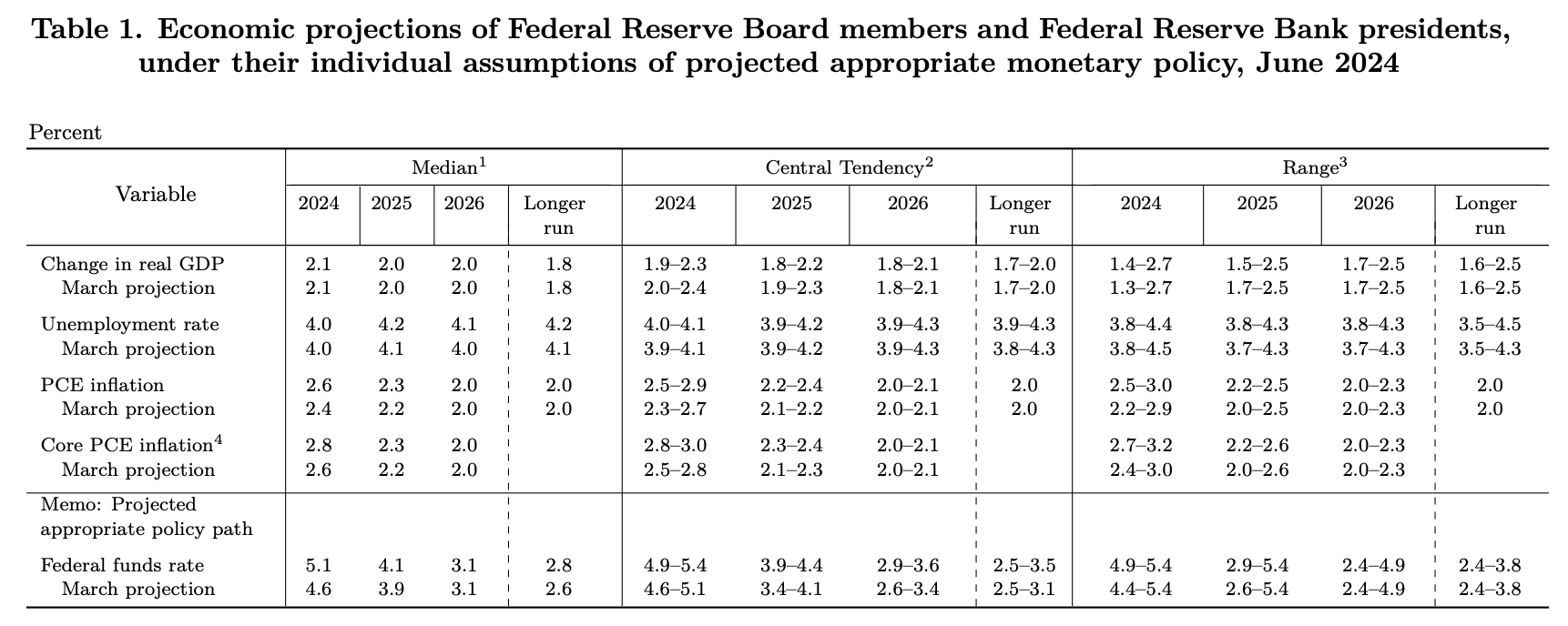

The Fed also publishes its latest Statement of Economic Projections (SEP) at this meeting, with the markets to search for clues about the potential path forward for policy in that document, too. The June SEP revealed forecasts for higher interest rates and subsequently fewer projected rate cuts following what was a period of stickier than expected inflation at the start of the year. With the balance of risks to the economy leading to a shift in focus from price stability to maximum sustainable employment, the SEP is likely to see a moderation in inflation forecasts, an increase in projected rate cuts and possibly a downward revision to growth and upward revision to the unemployment rate.

(Source: US Federal Reserve)

Heightened volatility likely amid policy uncertainty

Heightened volatility is highly likely off the back of this FOMC decision, given its a live meeting. Firstly, the markets will have to adjust to discount the additional 12 basis points of cuts, or price-out roughly 13 basis points of cuts depending on whether the central bank lowers by 25 or 50 basis points. Secondly, the markets will have to shift the shape of the futures curve according to the Fed’s commentary and Statement of Economic Projections. The four most probably scenarios look like the following:

| Dovish | Neutral | |

|---|---|---|

| 25 bps | The Fed only cuts by 25 basis points, prompting an unwind of the approximately 13 additional points of cuts priced-into the curve. However, dovish commentary and lowered dot plots leads the markets to defer expectations of a 50 basis point move to either November or December. The smaller cut could be interpreted as a show of confidence in the US economy and therefore seen as a positive thing. There is the risk the markets perceive such a decision as the Fed not being responsive enough to downside risks to the labour market and therefore respond bearishly. The dynamic would likely weigh on the Dollar and give equities and gold a boost. | The Fed only cuts by 25 basis points, prompting an unwind of the approximately 13 additional points of cuts priced-into the curve. The central bank only lowers its dot plots moderately, defying expectations of a deep cutting cycle. The markets pare back expectations of a 50 point cut coming in either November and December, possibly raising fears about policy remaining relatively restrictive. While such a move may project confidence in the economy it could also stoke fear that the Fed isn’t attentive enough to downside risks to the labour market and is keeping policy at overly restrictive levels. The move would be positive for the US Dollar, negative for gold and other commodities, and probably negative for equities. |

| 50 bps | The Fed cuts by 50 basis points, with the markets immediately pricing in the approximately 12 additional points of cuts into the curve. The central bank emphasises the downside risks to growth and lowers the dot plots and inflation forecasts while also raising the projections for the unemployment rate. The markets move to price-in the potential for another 50 point cut in either November or December. While the prospect of lower rates could support equities and weaken the Dollar, such a pessimistic outlook could undermine market sentiment and lead to a bearish response. | The Fed cuts by 50 basis points, with the markets immediately pricing in the approximately 12 additional points of cuts into the curve. Two more 25 basis point cuts remain priced-in implying that the markets expect that the Fed will lower by a total of 100 basis points by the end of the year. While the neutral bias projects confidence about the economy, the 50 basis point move may raise concerns about the scale of downside risks to the US economy. The move likely supports equities and gold prices, while the US Dollar likely drops. |

Technical Analysis: US indices and US Dollar Index

Wall Street equities are at a critical juncture heading into the FOMC decision. The benchmark S&P 500 has formed a double top, carving out a critical level of technical resistance at approximately 5660. Meanwhile, the NASDAQ has failed to make a higher-high, although it remains in its primary uptrend. In the short-term, 5,400 looms as a significant level of technical support for the S&P 500, while roughly 18,400 is proving to be an area of buying activity for the NASDAQ.

(Past performance is not a reliable indicator of future results)

The US Dollar Index is in a primary downtrend leading into the FOMC decision. The 100.00 point level looms as much technical support, which if broken could open up a drop towards a significant level around 99.00. On the upside, 101.50 appears to be short-term technical resistance.

(Past performance is not a reliable indicator of future results)