Australian jobs data to test the RBA’s hawkish bias

The Australian labour force data could test interest rate market pricing and the RBA's hawkish bias.

The Australian labour force data for October is released on Thursday, 13th of November and could test the Reserve Bank of Australia’s hawkish bias.

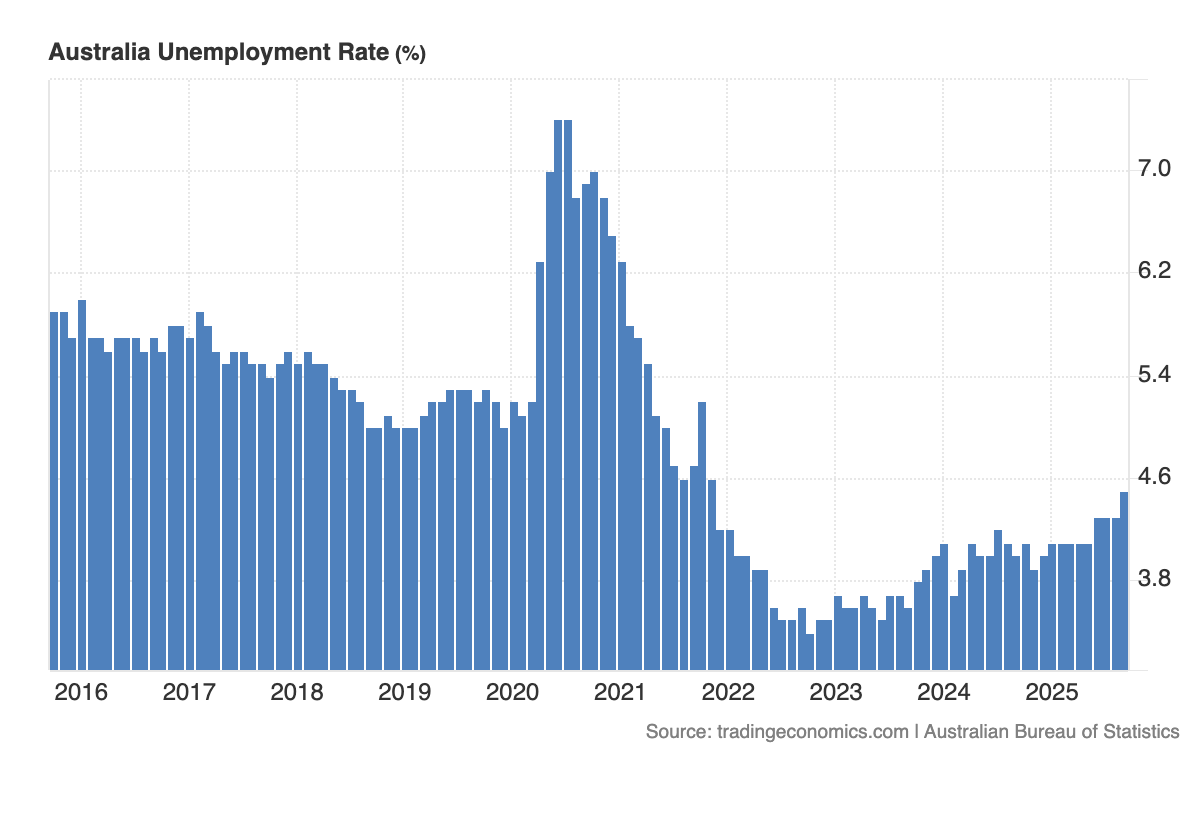

Forecasters predict a drop in the Australian jobless rate

The Australian Bureau of Statistics’ October Labour Force data is tipped to show a very modest improvement in the Australian jobs market. Forecasters predict a drop in the unemployment rate to 4.4%, down from the 4.5% recorded in September that marked a nearly four year high in the measure. The fall in the unemployment rate is predicted to be supported by a 20,100 employment increase for the month, also an improvement on a month earlier. However, with the notional breakeven number for employment a bit above 30,000, it’s likely economists are assuming a lower participation rate in October.

(Source: Trading Economics)

(Source: Trading Economics)

A weak jobs report would put the RBA into a scary dilemma

The employment data comes hot on the heels of an RBA decision which saw the central bank adopt a decidedly hawkish stance. Owing to a shocking surprise in recent quarterly CPI data, which not only revealed an expected leap in headline inflation but also a very unexpected rise in underlying inflation to 3%, the RBA struck a very cautious tone about the prospect of future rate cuts. The central bank projected an inflation rate that would persist above target for much of 2026, leading to the markets pricing out the likelihood of further cuts. Pricing leading into the latest jobs report implies a roughly fifty-fifty chance the RBA cuts rates again from here. The markets had been discounting a full cut at the December meeting only weeks ago.

(Source: RBA)

While the RBA revised its forecasts meaningfully for inflation, the revision for the labour market wasn’t quite as stark. The central bank lifted the projection for where it thinks the Australian unemployment rate will level-out at; however, the 4.4% forecast for the end of 2025 is below the current rate of 4.5%. It suggests the RBA is assuming a degree of resilience in the Australian economy and that the labour market ought to remain tight enough to avoid any uncomfortable trade-offs between jobs and inflation. A higher than expected unemployment rate in this week’s data could push the RBA into the dilemma of prioritising one of its goals and the expense of the other. That could create policy uncertainty for the markets and potentially lead to heightened volatility.

Australian labour market conditions will impact the AUD/USD’s long-term trend

The AUD/USD’s 2025 uptrend, which has been largely a function of a broad-based US Dollar weakness, appears to be slowing down. Meanwhile, the pair’s longer-term downtrend remains structurally in place, with the weekly chart revealing a loss of upside momentum. Labour market strength or weakness could be a major determinant of the short-term and long-term trend for the AUD/USD. A softening labour market could weigh on the pair, with the markets possibly repricing for the higher of odds of rate cuts, either on the belief that it could reflect more spare capacity in the economy and therefore lower inflationary risks, or that the RBA will sacrifice controlling inflation to protect the labour market. Alternatively, a jobs market that remains in a strong enough position for the RBA to remain solely focused on its inflation mandate could prop-up the AUD/USD, although such a dynamic could be offset should the US Dollar continue to appreciate.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)