US Non-Farm Payrolls data forecast to reveal solid labour market

Explore the December 2024 Non-Farm Payrolls report, revealing job growth, wage trends, and labor market resilience. Analyze its implications for Federal Reserve policies, inflation control, and financial markets.

Non-Farm Payrolls data is expected to show resilient labour market

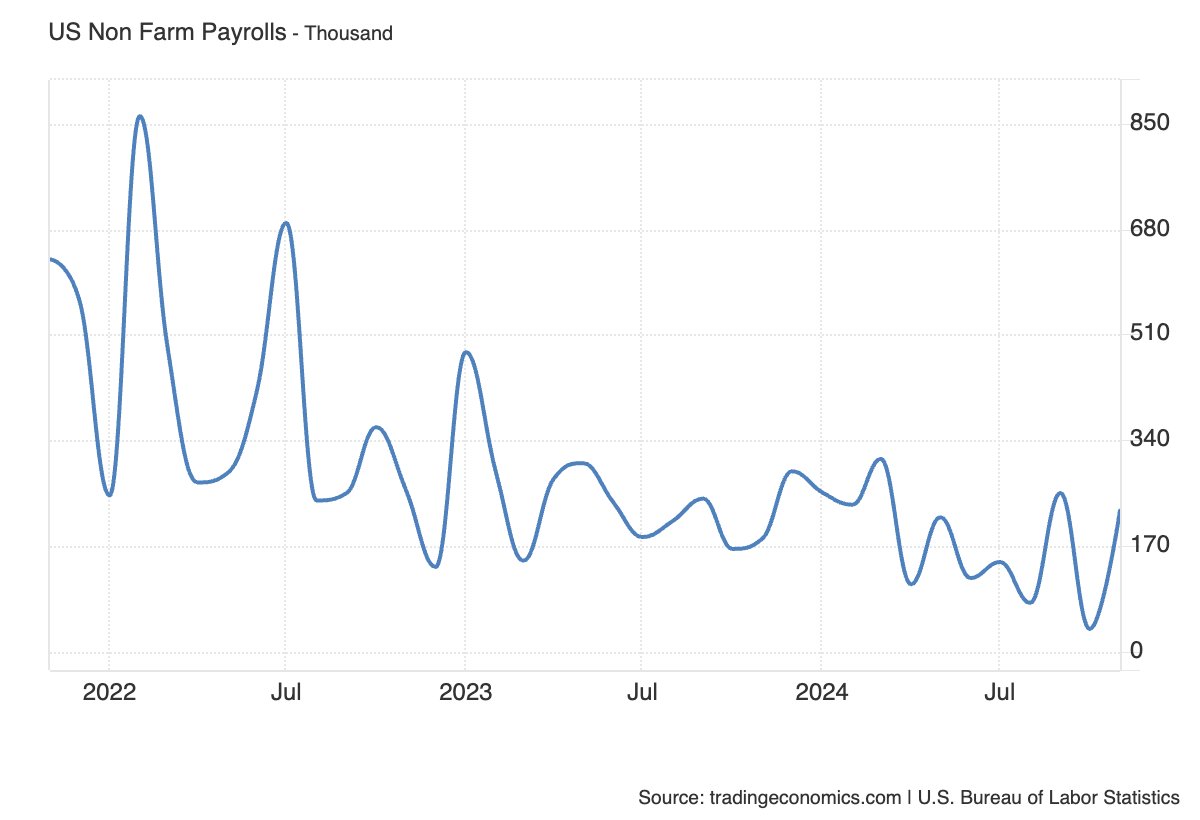

The upcoming Non-Farm Payrolls (NFP) report for December 2024 is a key release, shedding light on the state of the US labor market as the economy transitions into 2025. Economists expect an increase of 154,000 jobs, a slowdown from November’s gain of 227,000 jobs, reflecting an economy adjusting to the Federal Reserve’s recent monetary policy changes.

(Source: Trading Economics)

The unemployment rate is forecast to hold steady at 4.2%, suggesting a labor market that remains tight but is much looser than a year ago. Analysts will closely monitor this figure for any indication of weakening demand, which could signal broader economic softness.

On wages, average hourly earnings are anticipated to soften slightly, pointing to easing inflationary pressures. Slower wage growth could reflect the impact of previous rate hikes and offer reassurance to policymakers focused on controlling inflation.

Payrolls data could impact timing and number of Fed cuts in 2025

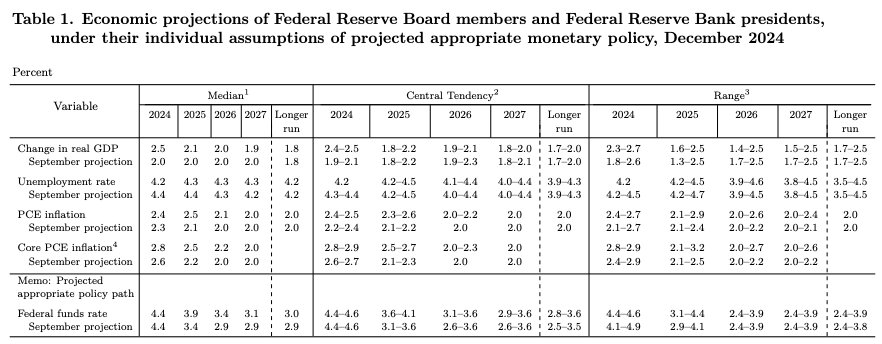

The Federal Reserve is expected to pause its rate-cutting cycle due to a resilient labor market, persistent inflation, and stronger-than-anticipated economic growth. At its December 2024 meeting, the Fed revised key projections: raising the dot plot for future rate paths, increasing the PCE inflation forecast, and lowering the unemployment rate projection. These adjustments highlight ongoing concerns about inflation and labor market tightness despite recent rate reductions.

(Source: US Federal Reserve)

The December FOMC meeting also featured a dissenting vote from one member favoring a pause in rate cuts, underscoring growing divisions within the committee about the appropriate trajectory for policy. A stronger-than-expected December jobs report could solidify the Fed’s decision to maintain its current stance, while weaker data might renew calls for further easing. However, with inflation still above target, the Fed remains cautious about acting too quickly.

The FOMC minutes for the December meeting is scheduled to be released on the 8th of January and may offer clarity, or muddy further, the central bank’s outlook for economic growth and policy, and its reaction function.

The markets look for another set of goldilocks figures

A stronger-than-expected NFP report, with robust payroll gains and stable or rising wages, would likely reinforce expectations for a prolonged Fed pause. Short-term Treasury yields could rise as markets price in tighter policy, while the US Dollar would strengthen on higher yield differentials. Equity markets might face headwinds from concerns over borrowing costs, although the implications for strong consumer activity and earnings could support the market. Gold prices, conversely, could decline as higher yields and a stronger dollar reduce its appeal.

A weaker-than-expected NFP report, with softer job growth and slowing wages, would likely bring forward the timeline of the Fed’s first cut in 2025 and increase the odds of two cuts for the year. Treasury yields might fall as a result, boosting equity markets, especially in growth-sensitive sectors like technology, although that may be offset by risks of softer economic growth. The US Dollar could weaken as the US economy’s outperformance diminished marginally, making gold more attractive and benefiting from lower real yields.

The US Dollar Index hits a 2-year high

The US Dollar hit a two year high, maintaining its “Trump-trade” uptrend. The US Dollar Index completed a textbook breakout from its symmetrical pennant formation, pushing the index into overbought territory on the daily charts, indicating strong upward momentum. New technical resistance is possibly around the 109.50 higher-high, while support may be found at previous resistance at roughly 108.50.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)