US Core CPI tipped to remain unchanged in September

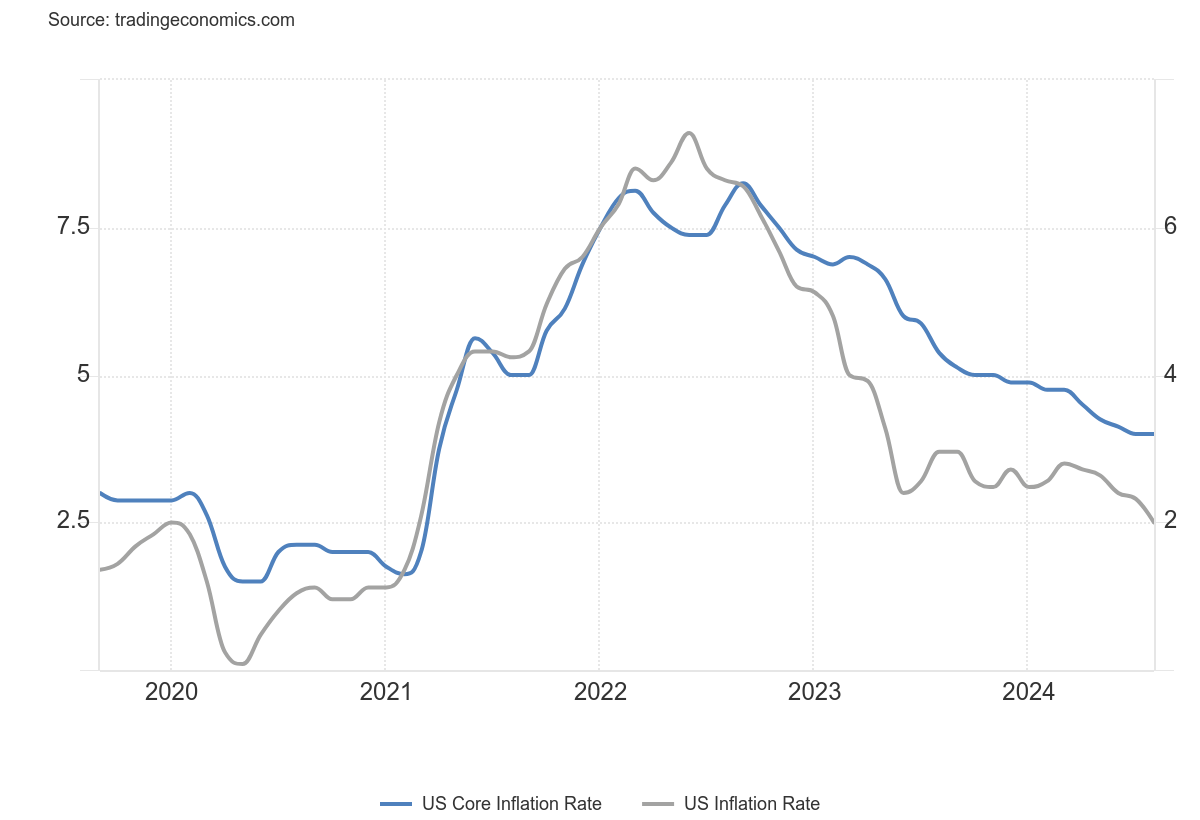

US inflation expectations are steady, with core CPI projected to remain at 3.2% for September while headline inflation moderates to its lowest level since February 2021. Despite the US Federal Reserve delivering a 50 basis point interest rate cut in September, stronger-than-expected job market data has raised concerns about sustained economic demand and inflation pressures.

Forecasters predict steady core inflation in the United States

Market economists expected no further progress on returning US inflation back to target in August. US core CPI is projected to remain unchanged at 3.2% in September, although headline price growth forecast to moderate to 2.3% – the lowest level since February 2021.

Source: Trading Economics

Upside risks to inflation have receded as a major concern and cause of volatility in financial markets recently, with signs of deterioration in the US labour market replacing them with fears about slowing economic growth. The dynamic led the US Federal Reserve to begin cutting interest rates in September, with the central bank delivering a 50 basis point cut – a move normally reserved for emergency situations. Questions have arisen about whether such a move was premature, however, following a stronger than expected September Non-Farm Payrolls release. Signs of resilient growth have raised fears about the ongoing strength of US demand and the potential stickiness of price pressures.

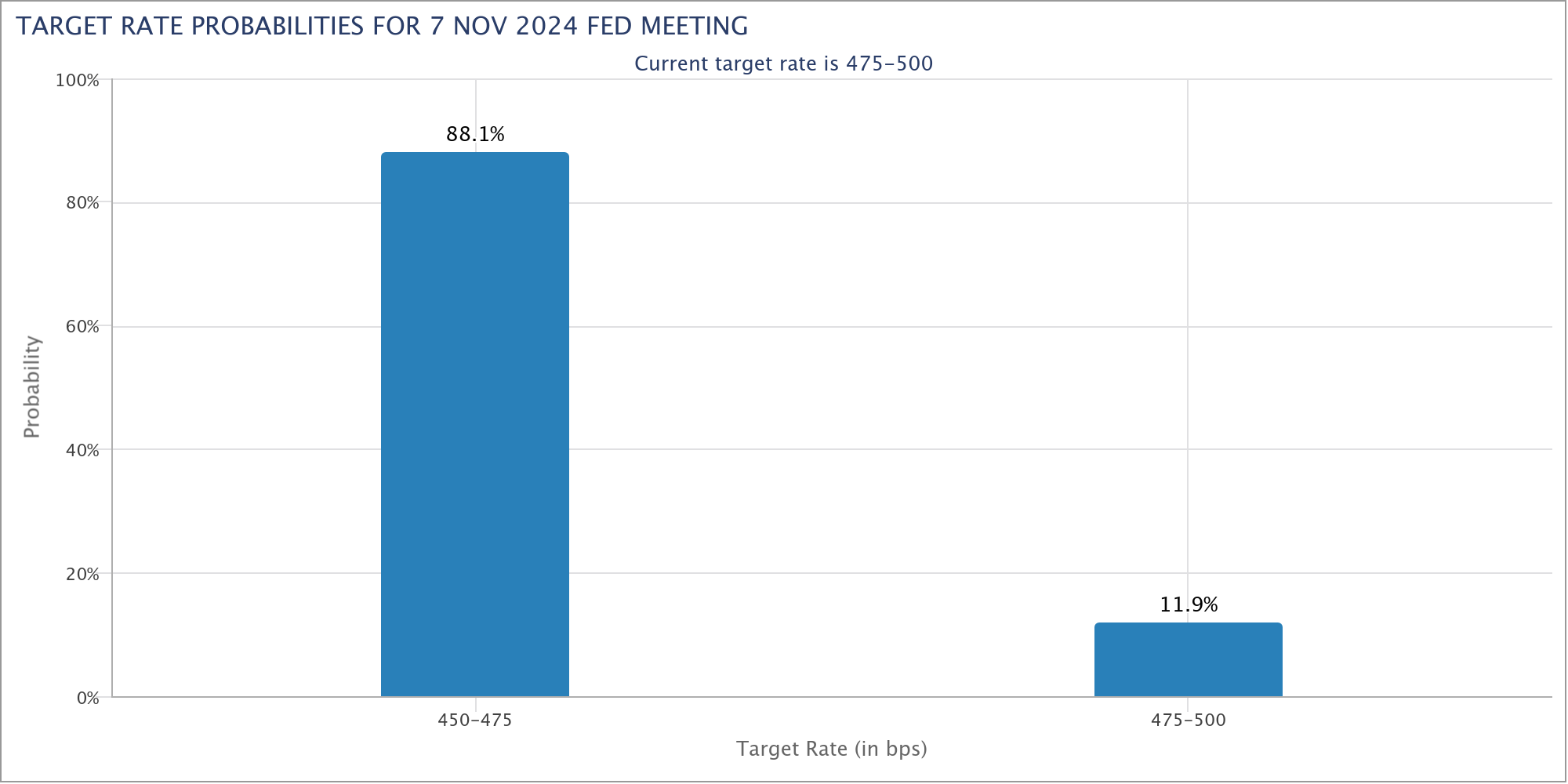

Markets dial down expectations for future Fed rate cuts

The strong September Non-Farm Payrolls data sparked an aggressive repricing of US Federal Reserve rate cut expectations. Following the September FOMC decision, at which the central bank shifted decisively to a dovish bias, market participants were discounting a high probability of the equivalent of three 25 basis point cuts before the end of 2024, implying another 50 basis point reduction at either the November or December meeting. Leading into the monthly CPI data, the markets are pricing in an 88% chance of a 25 basis point cut at the November meeting according to the CME Group’s FedWatch tool, and 12% chance rates will remain unchanged.

Source: CME Group

The minutes from the FOMC’s September meeting will be released a day earlier than the inflation figures and may frame how the markets interpret the data. Given the almost unanimous dovishness from board members implied in the meeting’s Statement of Economic Projections and policy statement, expectations are for a similarly dovish tone to come through the minutes. The markets will be attuned to any mention about upside risks to inflation and to what extent it may impact their future reaction function and ability to continue cutting rates aggressively.

The aggressive cuts still priced-in to the futures curve implies an upside surprise in inflation would stoke the greatest volatility. An unexpected, albeit unlikely, jump in core inflation and smaller than expected drop in headline inflation could force the markets to reconsider the Fed’s capacity to ease policy and compound concerns that a strong labour market is keeping inflation above target. Conversely, a downside surprise could still spark movement in the markets. Signs of continued disinflation could stoke bullishness and lead to a pricing back in of deeper Fed cuts, with any such dynamic likely to affirm the narrative that solid productivity growth is offsetting the impacts of strong demand.

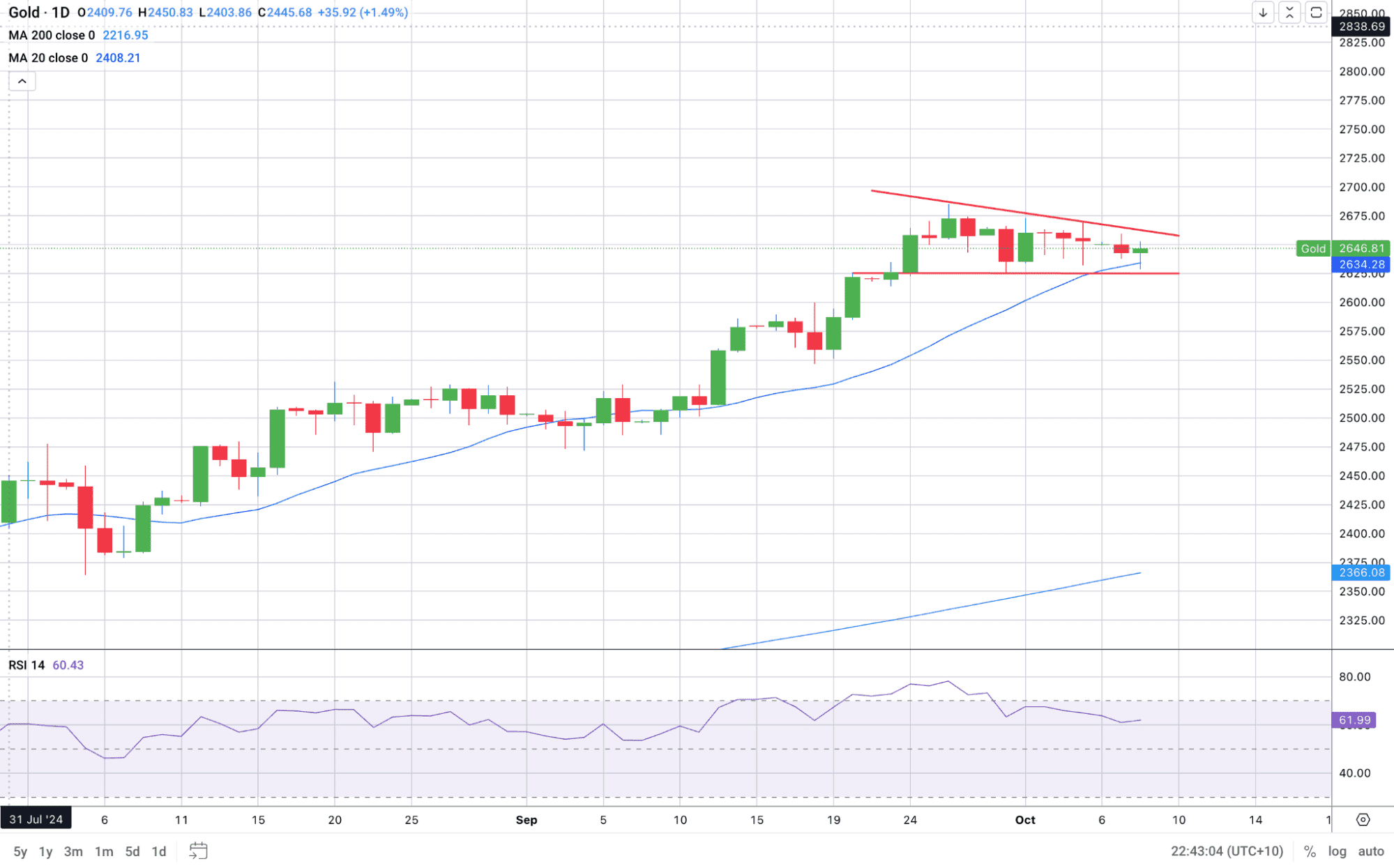

Gold traders may look for next cue in US inflation data

Gold prices remain in an uptrend as the prospect of US interest rate cuts coupled with heightened geopolitical tensions in the Middle East support demand for the commodity. The upside surprise in the Non-Farm Payrolls figures has led to a pull back towards gold’s 20-day moving average. However, the technical set-up looks constructive, with price action carving out a bullish continuation pattern. A break of downward sloping resistance could open a push to fresh record highs. Meanwhile, a break of support at $US2625 could signal a deeper pull back.

Past performance is not a reliable indicator of future results