The FOMC is expected to keep policy unchanged as the markets hope for a “Powell put”

FOMC Meeting: Markets Await Powell's Guidance on Interest Rates

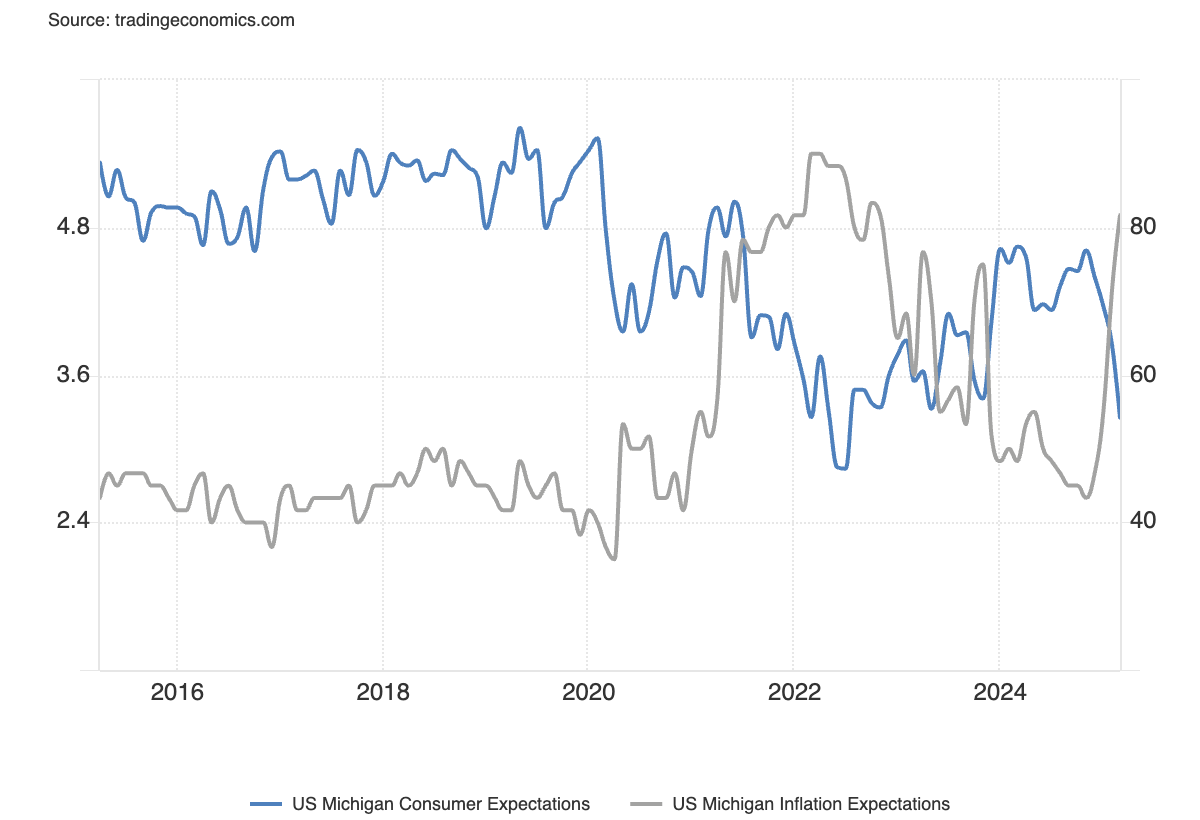

The markets head into the March FOMC meeting rattled by the Trump administration’s trade policy. Uncertainty about tariffs is hurting investor sentiment as well as that of business and consumers. Recent ISM activity surveys revealed the lack of clarity about trade policy is causing businesses to slow or delay employment and investment decisions. Meanwhile, successive University of Michigan Consumer Sentiment data showed a collapse in confidence, as well as a spike in US inflation expectations to 32 year highs.

(Source: Trading View)

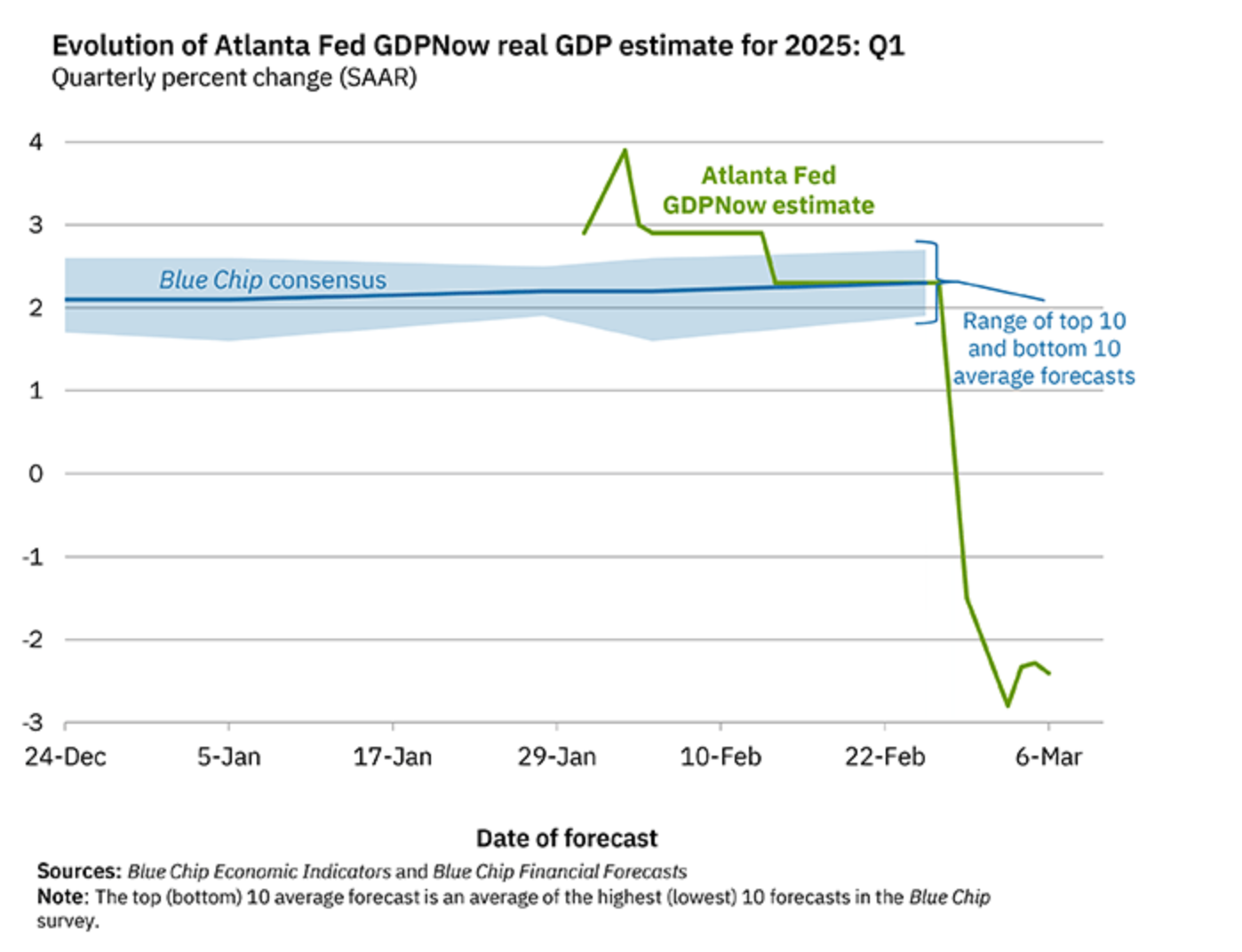

The deterioration in forward looking data and the increase in downside surprises in backward looking figures is positioning the US economy for a quarter of negative growth in Q1. While some of the dynamic can be explained by a cratering in the US trade position due to forward buying ahead of the imposition of tariffs, the oft-cited Atlanta Fed GDPNow forecast for growth this quarter has plummeted, with the latest update indicating a likely 2.4% contraction in economic activity.

(Source: Atlanta Fed)

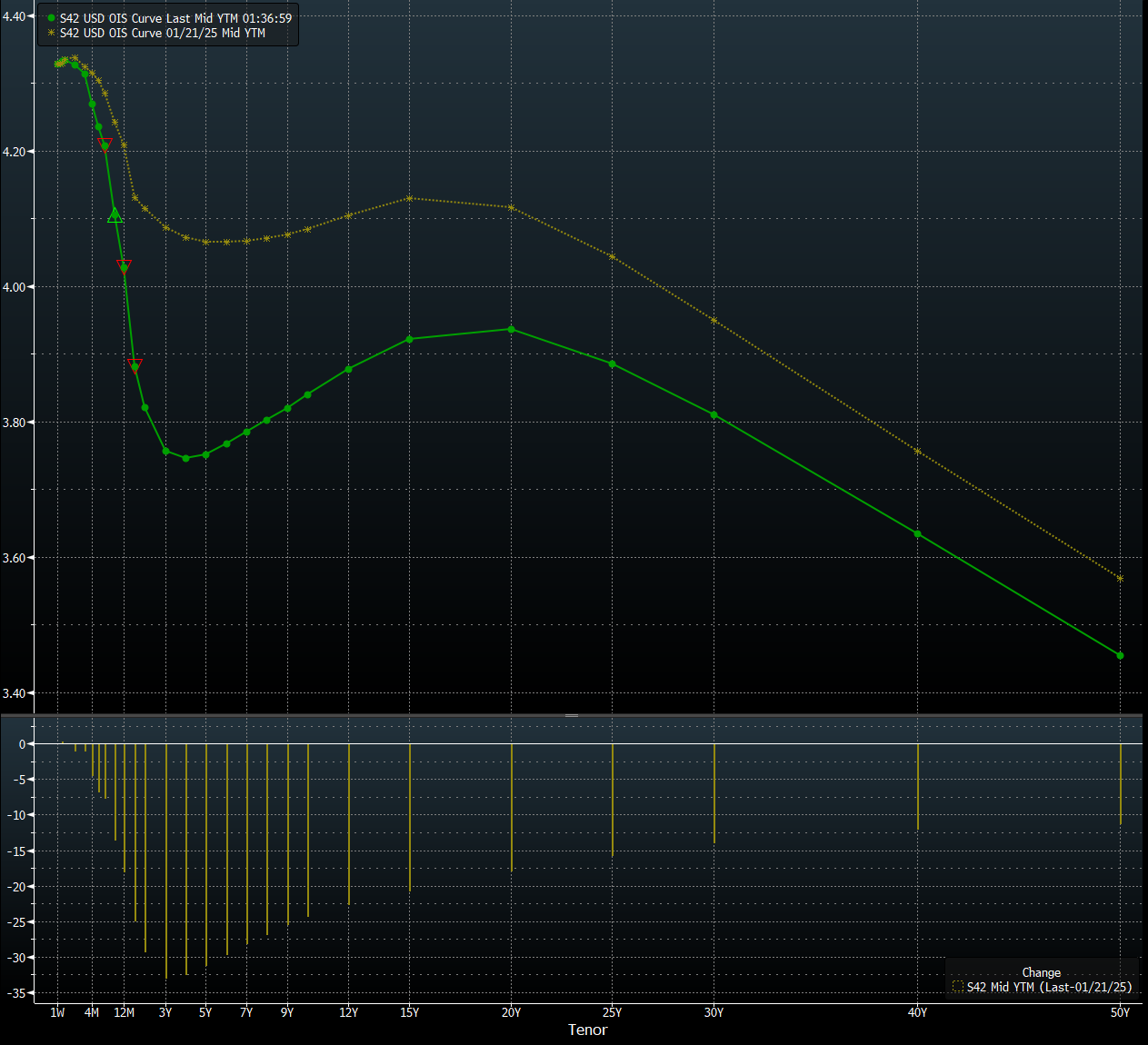

The downturn in the economy has led the markets to bring forward expectations for the next Fed rate cut and the number of times the Fed will cut this year. According to the US Dollar swaps curve, there is a high implied probability of a cut in June, with the markets practically fully baking in three cuts by the end of 2025. This contrasts with pricing from before US President Donald Trump took office which implied the Fed would hold off cutting further until September, with only a 50/50 chance the central bank would cut again after that.

(Source: Bloomberg)

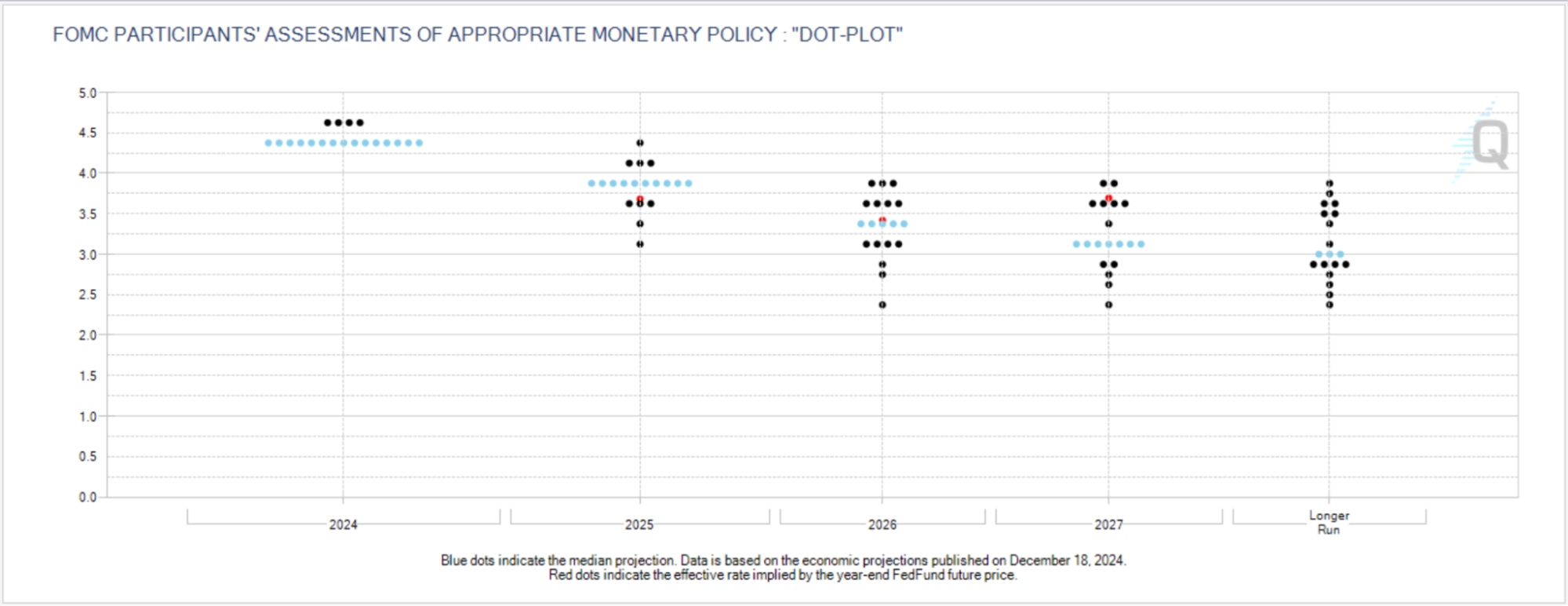

While it is all but certain the US Federal Reserve will keep policy unchanged at this meeting, the markets will be searching for guidance from the central bank that it is prepared to ease policy in order to support the economy from the impacts of tariffs and trade uncertainty. The Fed releases its latest Summary of Economic Projections with this month’s decision, with the markets implying a higher chance that the Fed revises its forecasts to include more than the two cuts for 2025 it had projected in its December update.

(Source: CME Group)

In the absence of a so-called “Trump-put”, Wall Street will be searching for a “Powell put” at this meeting to support shaky equity markets. From a technical point of view, the S&P 500’s 18-month uptrend could be reversing, with the weekly RSI showing significant downside momentum and price action carving out a double top on the charts. The index finished last week around its 50-week moving average, with the next critical support level around 5400.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

The US Dollar Index is also forming a short-term downtrend as the Dollar positive elements of tariffs like smaller trade deficits is being offset by the weaker demand brought by higher costs and policy uncertainty. Price action suggests the DXY could be oversold in the short-term, with the daily RSI attempting to climb out of oversold territory. A break of 103.40 support could herald a deeper drop in the DXY, while a break above 104 resistance could see the Greenback retrace further.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)