Federal Reserve meeting preview: strong data is making it hard to justify cutting rates

Markets expect the Fed to keep rates unchanged as strong economic data continues

The Federal Reserve is expected to keep rates unchanged at its meeting on Wednesday. Data from Reuters shows a 98% chance of no changes to the current range of 5.25% - 5.50% despite data released on Friday showing the core PCE index – the Fed’s preferred measure of inflation as it measures the change in prices of what consumers buy – dropped to 2.9%. This was the lowest level since March 2021. Meanwhile, the CPI – which measures the price change of a basket of goods in the marketplace – rose marginally to 3.4% in December, highlighting how the disinflation process becomes trickier the closer it gets to the 2% target.

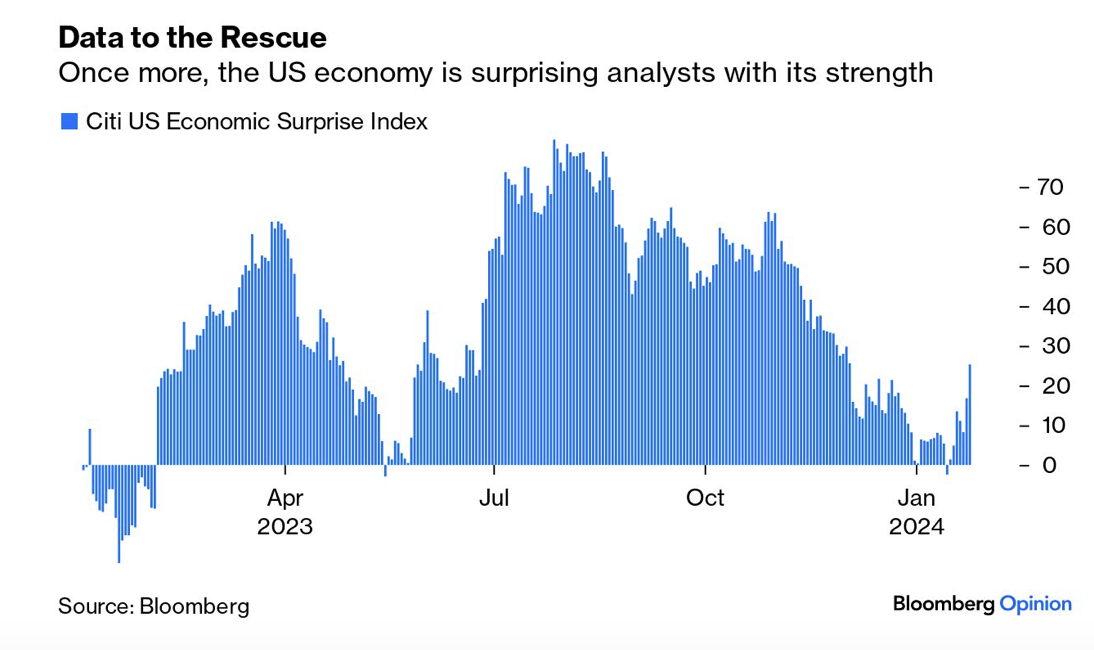

Nonetheless, inflation is becoming less of an obstacle to cutting rates. The question is whether there is any pressing need to do so. The latest GDP data showed the US economy grew 3.3% in the last quarter of 2023, following on from a rise of 4.9% in Q3. This evidences that the economy has been gliding along gracefully even with rates where they are, a stark contrast to that seen in the UK and the Eurozone. The chart below shows that after a significant drop in Q3 2023, the data being released in the past few weeks is coming in higher than expected. So, should Powell and his team consider cutting rates anytime soon?

Past performance is not a reliable indicator of future results.

It seems to be getting harder to justify pricing in immediate rate cuts. If we take the ECB as an example, Lagarde and her team left rates unchanged at their meeting last week and failed to acknowledge a timeline for cutting rates, avoiding entirely giving any forward guidance. The latest data in the region showed the CPI rose marginally in December but it remains below 3%, whilst growth is forecasted to have contracted 0.1% again in Q4, pushing the Euro Area into a technical recession. So, some may ask themselves, if Lagarde hasn’t felt the need to cut rates yet, or even suggest doing so anytime soon, why should Powell?

Yes, technically rates in the US are higher, but as mentioned above, the economy is in a much better place. That said, unlike Lagarde and BoE Governor Bailey, Powell did show a dovish inclination at the December FOMC meeting, which shocked markets at the time. We did see Fed policymakers push back on market expectations of immediate rate cuts after the meeting, which gave the feeling that Powell had gotten slightly ahead of himself with the dovish remarks. But the fact that he was willing to openly talk about rate cuts sometime in 2024 does put him at the top of the list of the central bankers most willing to cut rates. This alone could affect market positioning this week depending on how Powell presents himself this time around.

Some issues could now arise on how to define when the time is right to cut. The Federal Reserve has a dual mandate – inflation and employment. Whilst the former has come a long way in the last year, the jobs market remains very tight. In the past, Powell has insisted on the need to see some weakness in the labour market to consider loosening financing conditions. Some of that persistence seems to have gone away in recent months, but we cannot forget the fact the central bank will still be monitoring the tightness in the labour market closely. Meanwhile, there are various ways to measure what tight financial conditions are. Real rates can be expressed by subtracting core CPI from the Fed funds rate, by taking the yield on 10-year Treasury Inflation-Protected Securities (TIPS), or by subtracting the one-year bond market breakeven rate of inflation from the effective Fed funds rates, which Powell has expressed in the past was his favourite way to measure. All of these will offer a different view of real rates, so representational bias may present as an issue.

But regardless of how real rates are measured, the resilience in the stock market could make it risky for the Fed to cut rates. Rising asset prices create wealth that can be spent, therefore fuelling inflation. The ongoing geopolitical risks are also an inflationary pressure to watch out for, as are rebounding energy prices, which highlights the tough job of balancing high growth and disinflation.

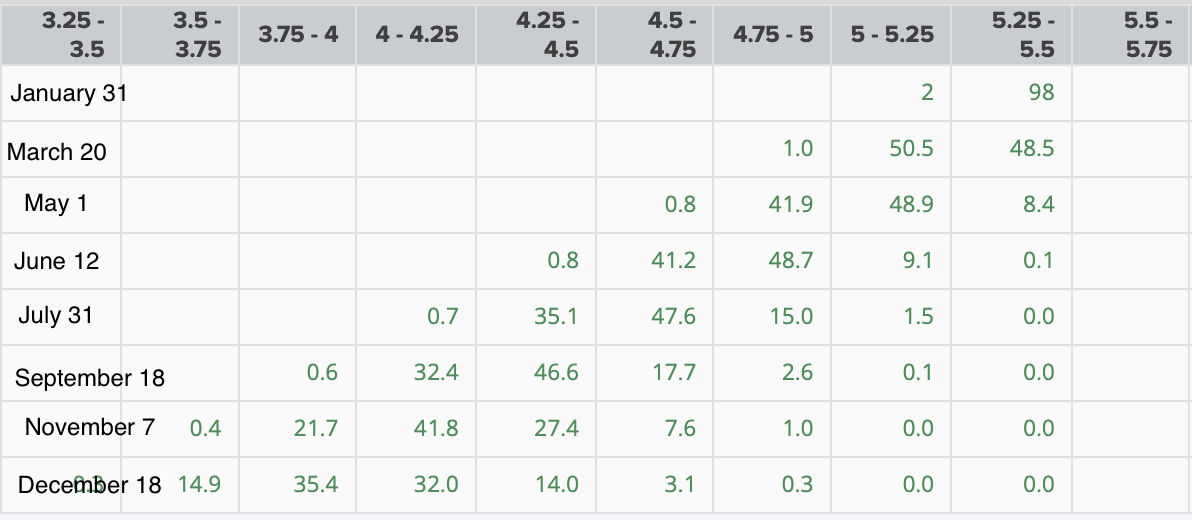

The data provided by Reuters suggests it is a done deal that the Fed will not cut rates this week, but markets are dying to know when rate cuts will eventually start. The Fed is known for being conservative, and they want to avoid cutting and then having to reverse course. Because of this, it may not be until the second half of the year that we see the first 25bps rate cut. Also, because whilst recent data enables rate cuts, there is no urgency to do so. Markets are currently pricing in a 50% chance that rates may be cut 25bps in March – this still seems way too soon. By December, markets are pricing in a 35% chance that rates will be between 3.75% and 4%, suggesting 150bps of cuts in 2024. This seems overly ambitious and therefore some repricing is likely to occur over the coming months.

Federal Reserve probability distribution 2024

Source: Refinitiv

Forward guidance is going to be eagerly sought out as market participants want to know how the Fed views the upcoming months. If they focus on the strong data and push back the likelihood of rate cuts, then the repricing may favour the US dollar and yields, and weigh on equities. Alternatively, if the dovish messaging continues, equities may be looking to extend the recent rally, whilst the US dollar could reverse the positive momentum seen in January so far.

US dollar index (DXY) daily chart

Past performance is not a reliable indicator of future results.