Australian inflation data to test expectations of February RBA cut

Discover how Australia's November CPI data could shape expectations for a February RBA rate cut. Key focus on trimmed mean inflation and its implications for monetary policy and AUD/USD trends.

Headline CPI indicator expected to rise but focus remains on trimmed mean data

The Australian Bureau of Statistics (ABS) will release the November CPI data on January 8, 2025, with markets forecasting the annual headline inflation to edge up to 2.2%, slightly higher than October’s 2.1%. This modest increase reflects ongoing disinflationary trends, bolstered by government energy subsidies that have capped energy price growth and helped alleviate pressure on household budgets. While the headline figure garners attention, the trimmed mean CPI, which excludes volatile items, holds greater significance for policymakers. October’s trimmed mean inflation stood at 3.5%, well above the Reserve Bank of Australia’s (RBA) 2-3% target range. For November, markets will be closely watching for signs of a decline in the trimmed mean figure, signaling a convergence toward the RBA’s target. A reduction closer to 3.0% could strengthen the narrative of easing underlying inflation pressures.

(Source: Trading Economics)

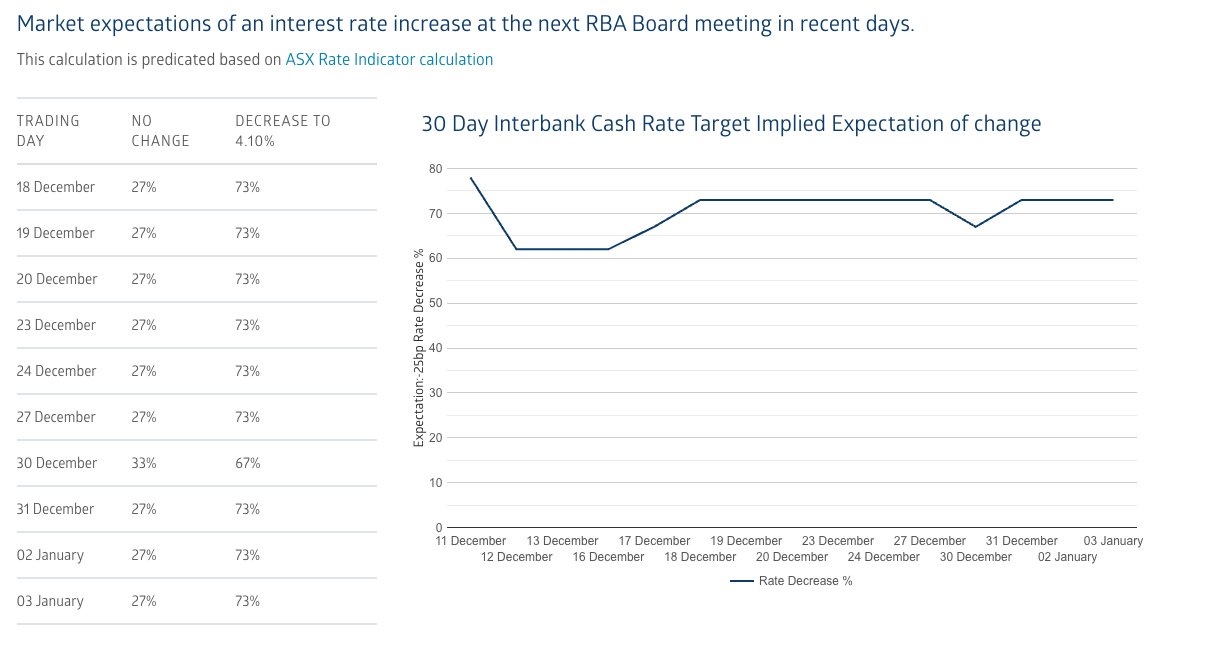

Inflation data to test expectations of a February RBA rate cut

The November CPI data will be pivotal in shaping expectations for the RBA’s February meeting. At its December meeting, the RBA adjusted its communication, notably omitting the phrase “the board is not ruling anything in or out” from its statement and stating it is “gaining some confidence” inflation is moving sustainably towards target. A soft trimmed mean inflation figure this week would reinforce this expectation, aligning with recent indicators of weaker economic activity, especially slowing consumer demand. However, a surprise to the upside could recalibrate market expectations, compounding the effects of recent resilient labour market data and rekindling speculation of extended policy stability or even a return to hawkish rhetoric. Currently, the markets ascribe an approximately 70% chance of an RBA cut in February.

(Source: ASX)

AUD/USD remains in downtrend amidst weak Chinese growth and strong US Dollar

The AUD/USD remains in a primary downtrend, driven by weak Chinese economic activity and a strengthening US Dollar amidst resilient US growth and expectations of supportive fiscal settings under the incoming Trump administration. There are tentative signs of a burgeoning reversal in the pair, with price action carving out a rounding base and the daily RSI returning from oversold territory. Some short-term resistance could be found around 0.6250, with the critical level the downward sloping resistance level at the upper bound of the pair’s trend channel. Meanwhile, support has emerged with dips below 0.6200, with a new lower-low indicating an extended downtrend.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)