US unemployment spikes causing markets to lose confidence in the Fed’s policy

The US labour market cools in July causing investors to question the Fed’s decision to hold rates steady.

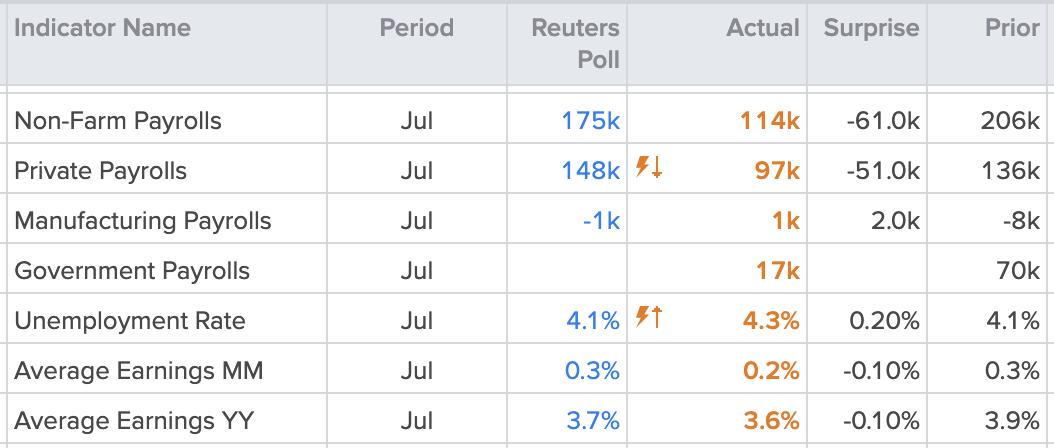

The July US labour market data has sparked some real concern in markets. Most of the data prints came in worse-than-expected, painting a picture of a slowing US labour market. Average hourly earnings and non-farm payrolls came in lower than anticipated, with the unemployment rate rising unexpectedly to 4.3%.

Thursday’s rise in jobless claims let to a market meltdown in the US stock market as investors became concerned that the Federal Reserve made the wrong decision by keeping rates unchanged on Wednesday. Because of this, a lot of emphasis had been placed on the US jobs data released today. Specifically on the unemployment rate because of a theory based on the Sahm rule, which states that we are likely in a recession if the three-month moving average of the unemployment rate rises half a percentage point from its low point in the previous 12 months. A rise to 4.2% would have triggered this rule, but 4.3% makes it even worse.

The reaction in markets has alluded to this. The dollar and US yields pulled back alongside US equities, whilst gold picked up some solid bullish momentum. These all point to increased concern in markets that the Federal Reserve has gone too far, holding rates high for too long. It seems now like Wednesday would have been the perfect time to start cutting rates, at least according to markets.

We’ll have to wait and see what Powell and his team have to say about the data. What seems like a given now is that the Fed will cut rates in September, the question that now arises is by how much. Prior to the jobs data markets were pricing in over a 90% chance of a 25-basis point cut, with no mention of any other amount. Current pricing shows a 70% chance of a 50-basis point cut, with the remaining 30% assigned to 25bps. Once again, this alludes to how much markets think the Fed was mistaken on Wednesday.

It seems unlikely that the central bank would decide to do an out-of-cycle cut following the latest data as this would just induce more panic in markets. But we may see clear some clear messaging from FOMC members that cuts are imminent, in an attempt to calm market jitters.

That said, the stock market had overheated significantly over the past year so the pullback that is currently taking place is well within the bounds of a normal correction. The question now will be whether policy easing over the coming months will be enough to restore the bullish momentum in stocks.

Another area to look out for is the US dollar and bond yields. The 10-year yield, often used as a benchmark, has dropped 20% since mid-April, and is now looking to break to a new one-year low. Meanwhile, gold is likely to continue attracting bullish demand as the precious metals benefits both from fears of a recession and lower rates.

US 10-year yield daily chart

Past performance is not a reliable indicator of future results.