The real driver behind gold: central bank demand

Central Banks across the globe are leaning into gold as a reserve asset as greater fragmentation, political risks, and fiscal deficits threaten the stability of international monetary systems.

Gold is often discussed through the lens of inflation, interest rates or geopolitical crises. Yet one of the most important drivers of the metal’s remarkable performance over the past several years has been far less visible: central banks.

While private investors tend to buy gold when uncertainty rises and sell it when confidence returns, central banks appear to be operating on a much longer time horizon. Even as gold trades near historically elevated levels, official sector purchases have remained robust. That raises an important question: what are central banks seeing that the rest of the market may be underestimating? The answer appears to lie not in short-term economic forecasts, but in a changing view of the global financial system itself.

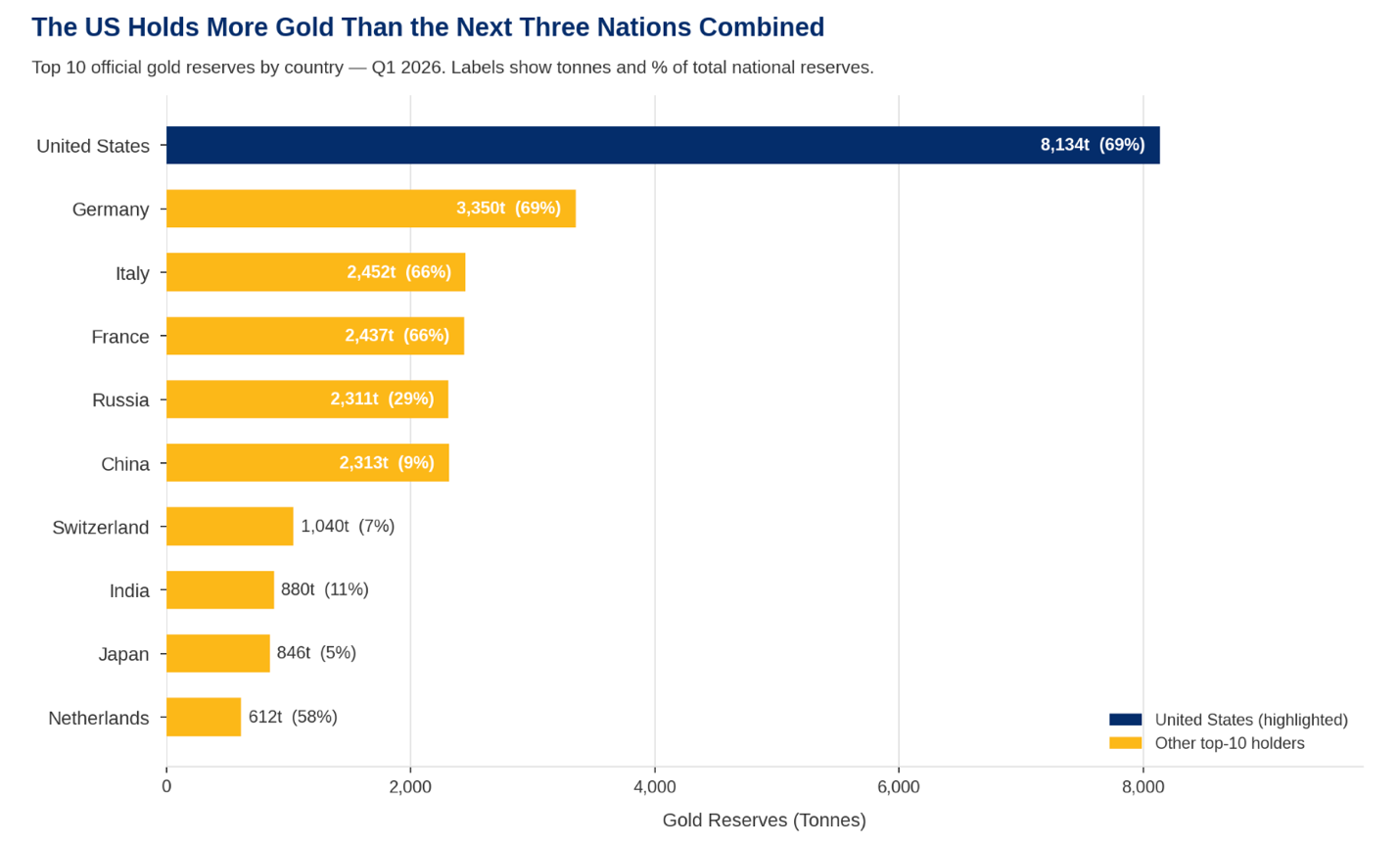

Gold Reserves by Country as of Q1 2026

Source: World Gold Council | IMF International Financial Statistics | goldsilver.com

A shift away from concentrated reserve risk

Historically, reserve management was relatively straightforward. Central banks held large quantities of US Treasuries and other major sovereign bonds because they offered liquidity, stability and security. Gold played a supporting role, but that balance appears to be changing. Rather than viewing gold primarily as an inflation hedge, many reserve managers now see it as a tool for diversification.

Unlike government bonds, gold carries no counterparty risk and is not dependent on the fiscal position, political stability or policy decisions of another nation. As geopolitical tensions have intensified and economic fragmentation has increased, the value of holding a reserve asset that sits outside the traditional financial system has become increasingly attractive.

If there was a turning point, it was arguably the freezing of Russia’s foreign reserves in 2022. Regardless of the political justification, the event fundamentally altered how reserve managers think about sovereign assets. It demonstrated that reserves held within the global financial system could become inaccessible under certain circumstances. For many countries, particularly emerging economies, this transformed reserve management from a purely financial exercise into a question of national resilience and financial sovereignty.

Gold suddenly looked different. Unlike foreign currency reserves held abroad, physical gold remains one of the few assets that cannot be frozen, sanctioned or restricted by another government. That characteristic has become increasingly valuable in a world where geopolitical relationships appear less stable than they once did.

Why Emerging Markets are leading the trend

The largest buyers of gold in recent years have generally been emerging-market central banks rather than their developed-market counterparts. This is not particularly surprising. Countries such as China, India and Turkey typically hold lower proportions of their reserves in gold than many Western economies and therefore have greater room to diversify.

China, in particular, appears to be pursuing a long-term strategy that reduces dependence on the US dollar while simultaneously strengthening confidence in the renminbi. Gold fits naturally into that objective. Importantly, this does not necessarily represent an attempt to replace the dollar. Rather, it reflects a desire to reduce concentration risk within reserve portfolios. The distinction matters as the world is not moving toward a gold standard. Instead, it may be moving toward a more diversified reserve system where gold plays a larger role alongside traditional reserve currencies.

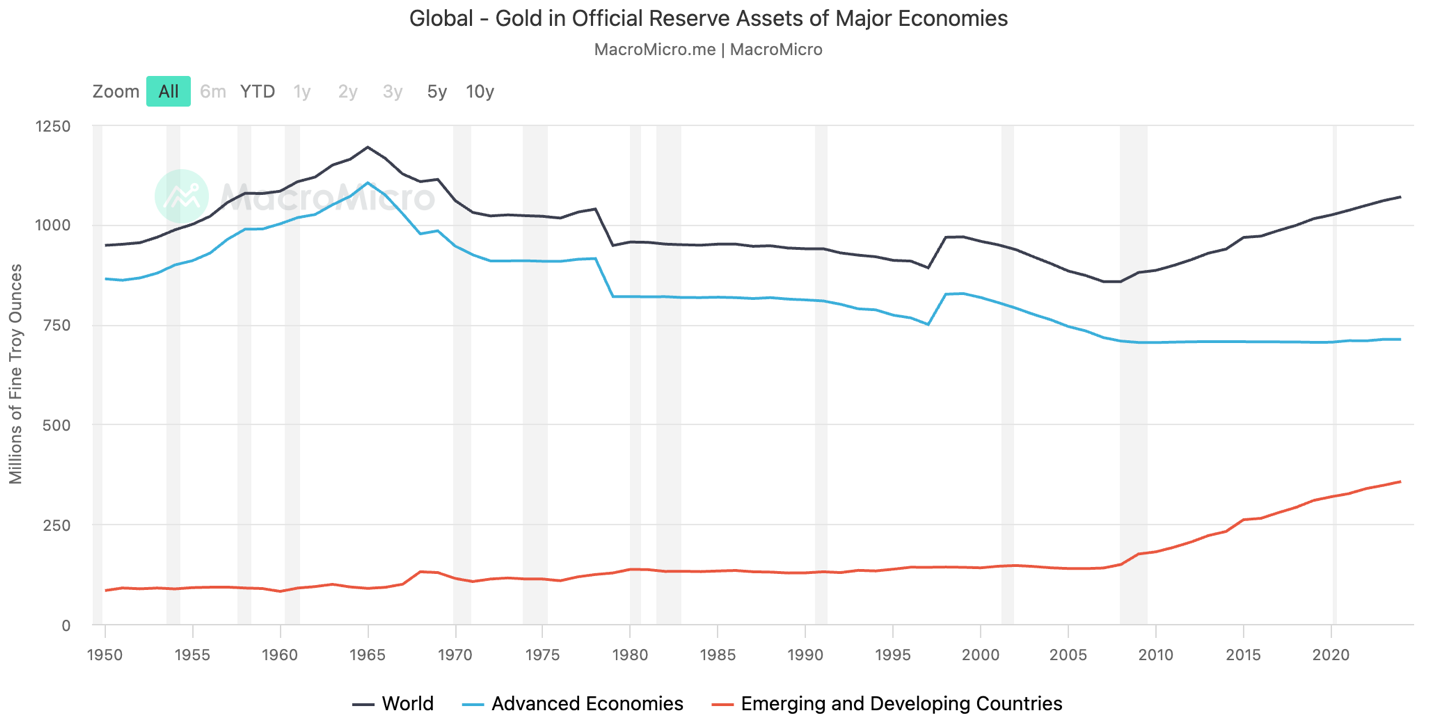

Gold in Official Reserve Assets of Major Economies

Source: MacroMicro.me

What Central Banks are saying about the future

Perhaps the most significant signal from central-bank buying is what it implies about their outlook. They are not positioning for a single event, they are preparing for a range of possible outcomes over many years. Persistent fiscal deficits, rising government debt, geopolitical fragmentation, trade realignment and periodic inflation shocks all create an environment where diversification becomes increasingly valuable.

In that context, gold is not necessarily a bet against the global economy, it is a hedge against uncertainty about how the global economy evolves. That distinction helps explain why purchases have continued despite the metal’s strong performance.

What it means for gold’s long-term outlook

The most compelling aspect of central-bank demand is its persistence. Unlike speculative investment flows, reserve allocation decisions tend to unfold over years rather than months. If official-sector purchases continue at their current pace over the next few years, it would suggest that reserve managers increasingly view the world as becoming more multipolar, less predictable and more prone to geopolitical and economic shocks.

For gold, that would represent a powerful structural tailwind. Short-term price movements will still be influenced by yields, inflation expectations and investor sentiment. Periods of consolidation and correction are inevitable. However, the long-term demand story appears increasingly anchored by institutions that are not buying gold because they expect a quick gain. They are buying it because they view it as a strategic asset for a world that looks fundamentally different from the one that existed a decade ago. And that may prove to be the most important bullish factor of all.

Gold (XAU/USD) daily chart

Past performance is not a reliable indicator of future results.