Market Mondays: Equities push higher as peace hopes and AI profits drive risk appetite

AI and strong earnings continue to drive equities higher as markets expect a peace deal outcome in the Middle East.

The dominant theme in markets remains a growing belief that some form of peace agreement between the US and Iran will eventually materialise. Investors have steadily priced a "peace premium" into assets, helping suppress volatility and underpin a rally that has pushed Wall Street to successive record highs. At the same time, the artificial intelligence story has only strengthened, with extraordinary earnings growth from technology companies reinforcing the view that AI monetisation is moving from promise to reality. Together, these forces have created an environment where investors remain overwhelmingly focused on profits rather than risks.

NASDAQ 100 daily chart

Past performance is not a reliable indicator of future results.

The strength of the rally is not evenly distributed, however. The US continues to lead, powered by exceptional earnings growth, rising productivity and expanding margins. The latest reporting season reinforced that narrative, with the Magnificent Seven delivering earnings growth far above already-lofty expectations. Investors are increasingly willing to pay for future growth because the profits are already being delivered today. The AI ecosystem remains at the centre of that story, driving demand for semiconductors, data centres and the raw materials required to build them. This has created a powerful feedback loop where strong profits support investment, investment supports growth, and growth supports further profits.

The contrast with other regions is telling. Europe has largely benefited from the gradual reduction in geopolitical risk, but it lacks the powerful earnings and AI-driven tailwinds present in the US. As a result, European indices such as the DAX and STOXX 600 have recovered, but not at the pace seen in US markets. Meanwhile, Asia has occupied a middle ground, with markets such as Japan and South Korea benefiting from semiconductor exposure and AI-related demand but remaining more vulnerable to energy prices and geopolitical developments. The result is a market landscape where the US has become increasingly dominant once again.

STOXX 600 daily chart

Past performance is not a reliable indicator of future results.

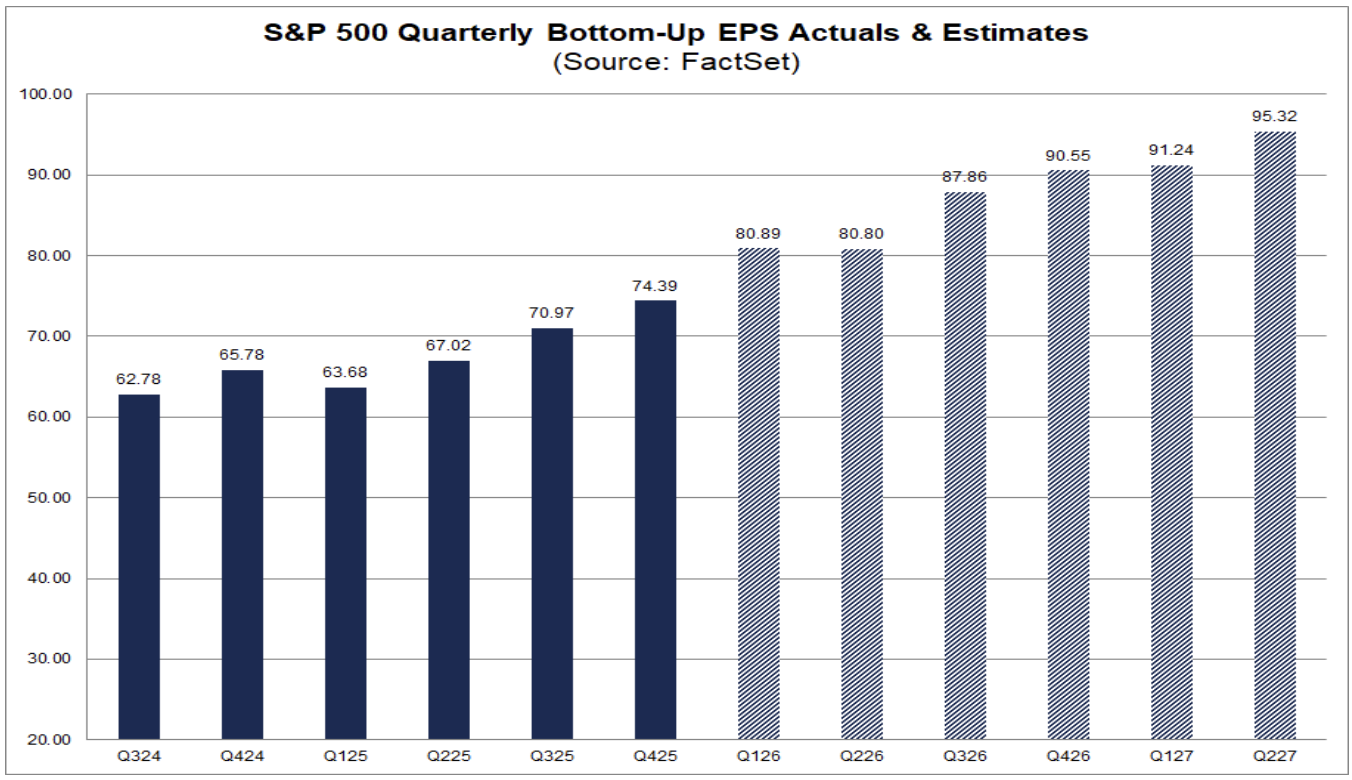

Underpinning this strength is a remarkable earnings backdrop. First-quarter earnings growth for the largest US technology companies dramatically exceeded expectations, with AI-linked firms continuing to deliver strong profitability and guidance. More importantly, investors are now looking beyond current results and focusing on the next phase of growth. The expectation is that AI adoption will continue to drive demand for computing power, creating sustained revenue opportunities across the technology supply chain. That belief has become one of the strongest supports for equity valuations.

Yet beneath the surface, some tensions are beginning to emerge. The very forces driving the rally may also be contributing to inflationary pressures. Demand for semiconductors, energy, copper, silver and other industrial inputs has surged as companies race to expand AI infrastructure. This growing competition for resources is beginning to show up in commodity markets and could eventually influence broader inflation dynamics. While oil prices have moderated from their peak as hopes of a peace agreement have improved, other areas of the economy continue to experience capacity constraints.

That inflation question remains central to the outlook. Recent US PCE inflation data offered some reassurance, coming in slightly softer than feared and helping ease concerns that inflation was accelerating uncontrollably. However, inflation remains elevated, and markets have increasingly shifted from discussing rate cuts to debating the timing of future rate hikes. The European Central Bank, in particular, is now expected to tighten policy further, while the Federal Reserve remains firmly in wait-and-see mode. For now, inflation is being treated as a rates story rather than an earnings story — and that distinction is critical. As long as profits continue to grow, investors appear willing to tolerate higher interest rates.

This leaves markets in an interesting position. On the one hand, valuations are elevated, momentum is extreme and positioning is increasingly stretched. Technical indicators suggest many indices are overbought, and speculative activity has picked up. On the other hand, earnings growth remains genuinely exceptional, providing a fundamental justification for much of the rally. That creates a situation where markets may be vulnerable to short-term pullbacks without necessarily changing the broader trend.

The key question is what could eventually disrupt this momentum. A breakdown in US-Iran negotiations and a renewed surge in energy prices remains one obvious risk. Another would be evidence that inflation is beginning to threaten corporate profitability rather than simply influence interest rate expectations. So far, neither has happened. Instead, investors continue to focus on strong earnings, AI-driven growth and the prospect of eventual geopolitical stability.

For now, the path of least resistance remains higher. But with markets increasingly reliant on a narrow set of assumptions — peace, profits and productivity — the margin for error is becoming smaller. The rally may continue, but the conditions required to sustain it are becoming more demanding.