Market Mondays: Warsh’s first Fed meeting sets the tone for a new era

Markets adapt to the new Federal Reserve under Warsh leadership as he offers little information in regards to forward guidance.

The Federal Reserve's meeting last week was always going to be about more than interest rates. It marked Kevin Warsh's first meeting as Chair, offering investors their first real insight into how the Fed might operate under new leadership. While the policy decision itself contained few surprises, the broader message was clear: the Federal Reserve remains firmly focused on inflation, and markets may need to adjust to a very different communication style than the one they became accustomed to under Jerome Powell.

Going into the meeting, one of the biggest questions was whether Warsh would prove as dovish as some had expected when he was first nominated. During the disinflationary environment that existed before the Middle East conflict escalated, many investors viewed him as a potential advocate for lower rates and a more accommodative policy stance. Instead, his first appearance suggested a chairman with a much stronger focus on price stability. While he stopped short of signalling imminent rate hikes, the overall tone was unmistakably hawkish relative to market expectations.

Perhaps the most notable change was not the message itself, but the way it was delivered. Under Powell, the Fed became increasingly focused on guiding expectations and reducing surprises. Markets often felt they had a relatively clear understanding of where policymakers stood and how they were likely to react to incoming data. Warsh appears to prefer a different approach. The statement was concise, direct and largely descriptive, while the press conference offered little in the way of explicit forward guidance. Rather than providing a roadmap for future policy, Warsh repeatedly emphasised ongoing reviews, analysis and policy workstreams, leading many observers to joke that there seemed to be a "task force for everything."

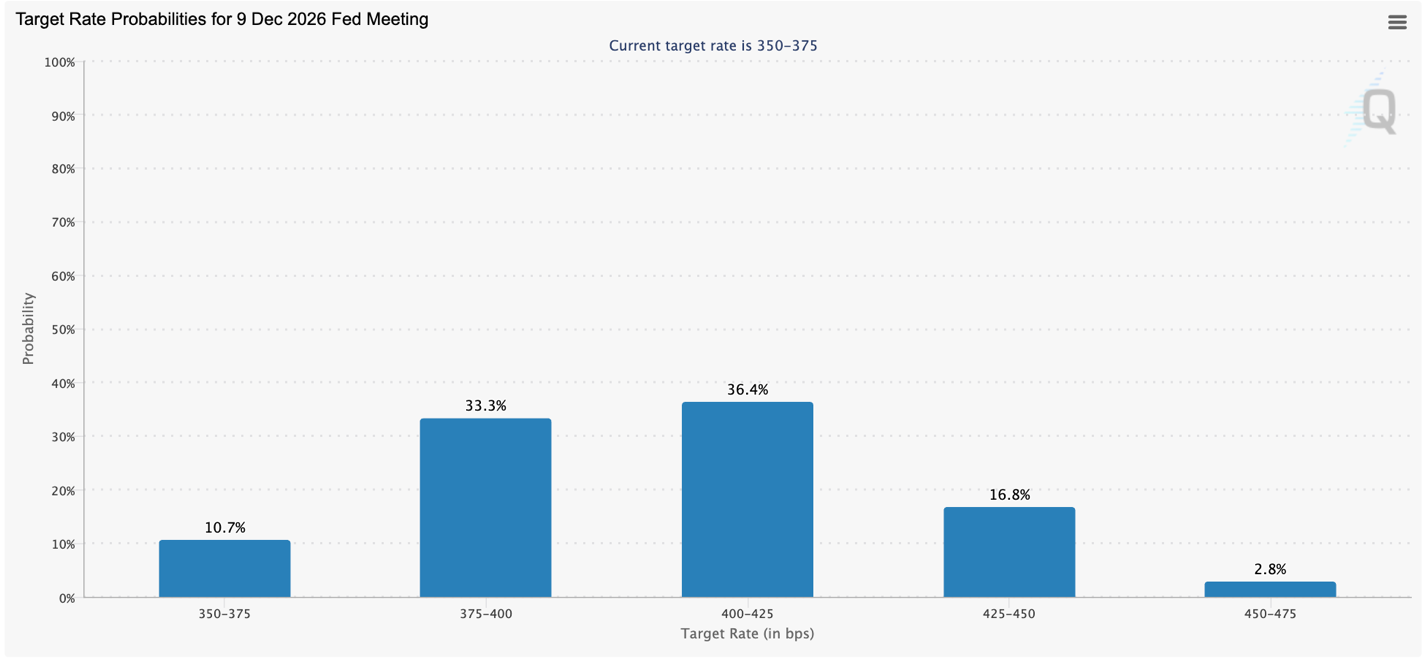

For markets, that shift matters. Less forward guidance means greater uncertainty around the future path of rates. While that can create more volatility, it also allows the Fed greater flexibility in responding to changing economic conditions. Importantly, investors appeared to conclude that the new chairman is willing to tolerate higher rates for longer if inflation remains persistent. As a result, market pricing for a rate hike before year-end increased following the meeting, reinforcing the view that policy may remain restrictive well into 2027.

Fed expectations for December 2026

Source: CME Fedwatch tool

The challenge for the Fed is that inflation risks remain complex. The ceasefire agreement between the US and Iran and the reopening of the Strait of Hormuz have helped push oil prices lower, reducing one important source of inflationary pressure. However, policymakers remain concerned about underlying price dynamics. Strong labour market data, resilient economic activity and the ongoing AI investment boom continue to create demand across large parts of the economy. While lower energy prices reduce some urgency, they do not eliminate the broader inflation challenge.

This leaves the Fed navigating a difficult balancing act. Policymakers are keen to avoid repeating the mistakes of 2022, when inflation was initially viewed as transitory and allowed to become deeply embedded. At the same time, they are conscious of episodes such as the ECB's 2011 tightening cycle, when rate hikes delivered into an energy shock were quickly reversed as growth deteriorated. Warsh appears determined to keep the Fed flexible enough to avoid either outcome.

The implications extend beyond the United States. The Bank of Japan's decision to raise rates to 1%, their highest level in more than three decades, highlights how central banks globally are grappling with similar challenges. Yet despite the hike, Japanese policy remains highly accommodative relative to the United States, contributing to further weakness in the yen and helping push USD/JPY beyond the 160 level once again. The contrast underscores just how important Fed policy remains for global markets.

USD/JPY daily chart

Past performance is not a reliable indicator of future results.

For investors, the key takeaway is that the Warsh era has begun with a clear emphasis on inflation discipline and a reluctance to provide detailed forward guidance. Markets may receive fewer assurances and fewer hints about future policy than they did under Powell. Whether that ultimately leads to better policy outcomes remains to be seen. What is already clear is that investors are being asked to operate in a world where inflation remains the central concern and where the Federal Reserve appears determined to retain maximum flexibility in responding to it.