US vs Europe: a widening performance gap driven by fundamentals

US equities are outperforming their European peers as their competitive advantage continues to dominate.

Over the past month, global equity markets have diverged sharply, with US indices pushing to fresh highs while European markets have struggled to keep pace. The S&P 500 and Nasdaq 100 have surged beyond pre-conflict levels, while the DAX 40 and STOXX 600 have lagged, consolidating or drifting lower. This divergence reflects not just sentiment, but a clear structural difference in how each region is absorbing the current macro environment.

DAX 40, EU STOXX 600, S&P 500 and Nasdaq 100 daily charts

Past performance is not a reliable indicator of future results.

Energy exposure: the defining factor

The most immediate driver has been the US–Iran conflict and the resulting energy shock. The US, as a largely energy-independent economy, has been relatively insulated from rising oil prices. Europe, by contrast, remains a net energy importer, making it far more sensitive to disruptions in the Middle East. This is clearly visible in price action. While US equities quickly recovered and pushed higher, European indices such as the STOXX 600 and DAX have remained volatile, reacting more directly to oil spikes and headline risk. In short, Europe is trading the conflict whilst the US is trading through it.

Growth resilience vs fragility

The divergence is also rooted in economic performance. The US economy has continued to show remarkable resilience, with steady growth, a stable labour market and strong domestic demand. Europe, on the other hand, has been dealing with weaker growth dynamics, particularly in industrial-heavy economies like Germany. European indices are more exposed to cyclical sectors and global trade, making them more vulnerable to any slowdown driven by higher energy costs or geopolitical uncertainty.

Earnings: the US advantage

Earnings season has been the clearest differentiator. In the US, results have remained exceptionally strong, with expectations for double-digit growth continuing into the coming quarters. The Nasdaq 100 in particular has been driven by large-cap tech, where profitability remains robust and demand, especially tied to AI, continues to support revenue growth. This has allowed US equities to justify higher valuations and extend their rally. Europe does not have the same earnings engine. While valuations may be lower, earnings growth has been more muted, and the region lacks the same concentration of high-margin, high-growth tech companies that have powered US indices.

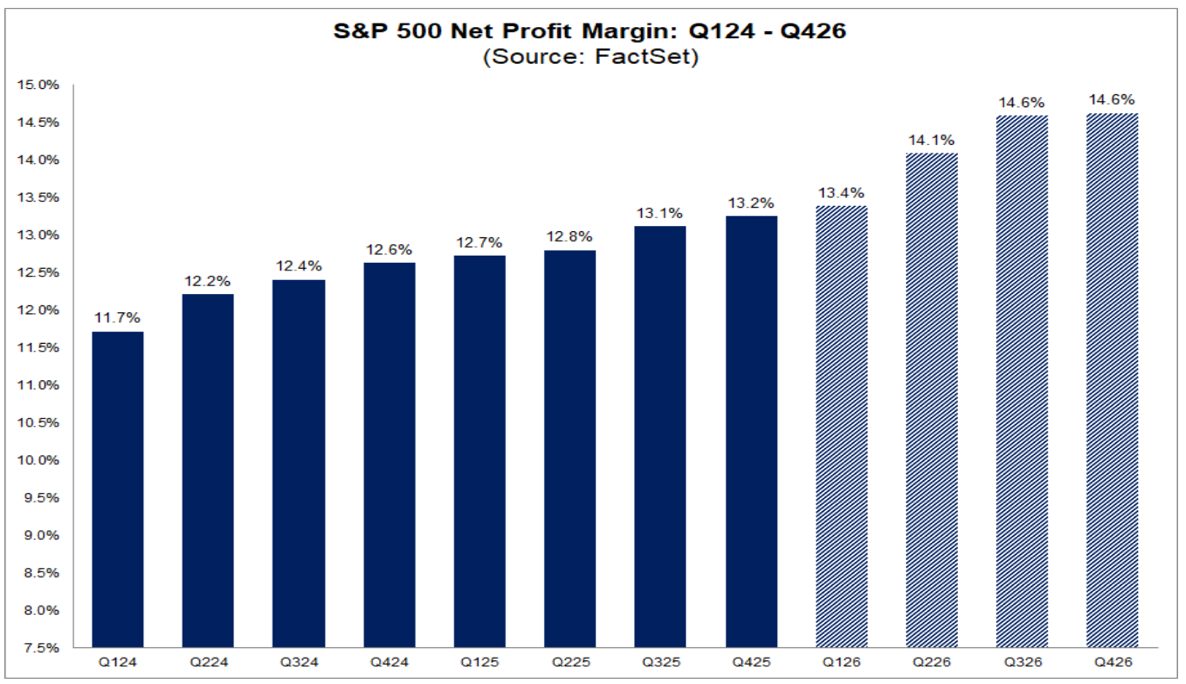

Profit margins and productivity

Another key factor is profit margins. In the US, margins have continued to improve, reflecting strong pricing power and rising productivity. There are growing signs that technology investment and efficiency gains are supporting profitability, even in a higher-cost environment. This contrasts with Europe, where margins are more exposed to input costs — particularly energy — and where productivity gains have been less pronounced. The result is a market that is more vulnerable to cost pressures and less able to absorb shocks.

The bottom line

The past month has reinforced a familiar theme: US exceptionalism remains intact. While European equities are more sensitive to external shocks and cyclical pressures, US markets are being driven by earnings, margins and structural growth.

For now, markets are making a clear distinction:

- The US is a growth and profitability story

- Europe is a macro and energy sensitivity story

However, this divergence also creates a degree of asymmetry in risk, leaving US equities more exposed to downside than upside from here. With the S&P 500 and Nasdaq 100 already pricing in strong earnings, resilient growth and contained geopolitical risk, there is less margin for positive surprise. In contrast, European markets have already priced in a more cautious outlook. That means if any of the key assumptions in the US narrative begin to falter — whether through weaker earnings guidance, margin compression from higher energy costs, or renewed escalation in the Middle East — the adjustment is more likely to come through US equities correcting lower rather than Europe catching up. In short, US markets are trading closer to a best-case scenario, which inherently makes them more vulnerable if reality falls short.