Market Mondays: Energy Shock Dominates Markets as Central Banks Face Stagflation Dilemma

Markets remain focused on the developments in the Middle East as central banks will be put on the spotlight this week.

The dominant force shaping financial markets right now is the energy shock stemming from the escalating conflict in the Middle East. With tensions continuing around the Strait of Hormuz, one of the world’s most critical oil transit routes, investors are increasingly pricing in the economic consequences of higher energy prices and weaker global growth.

At its core, the situation is reviving concerns about stagflation: a combination of rising inflation driven by energy costs and slowing economic activity. The longer the conflict drags on, and the longer energy flows from the Gulf remain disrupted, the greater the risk that higher oil prices will feed through into global inflation while simultaneously dampening growth prospects. For equities, that combination is particularly challenging. Higher inflation tends to keep interest rates elevated, while weaker growth pressures corporate earnings, a dynamic that has already begun to trigger risk aversion across markets.

The Strait of Hormuz at the centre of the crisis

The focal point of the conflict has increasingly become control of the Strait of Hormuz. Iran has sought to maintain pressure by restricting energy flows through the waterway, while the United States has attempted to neutralize Iran’s ability to enforce that blockade. Recent strikes targeting Iran’s military assets around the Gulf underscore the strategic importance of the strait.

For the US administration, reopening the strait is essential not only economically but politically. With midterm elections approaching, sustained high energy prices could become a major domestic issue. Yet the situation presents a difficult strategic dilemma. Iran has strong incentives to prolong the disruption as a deterrent against further Western intervention, while the US seeks to dismantle Iran’s capacity to control the shipping route.

The result is a high stakes stalemate that markets are struggling to price. Energy flows remain significantly constrained, and as long as that persists, the risk of a prolonged global energy shock remains elevated.

Central Banks face a policy crossroads

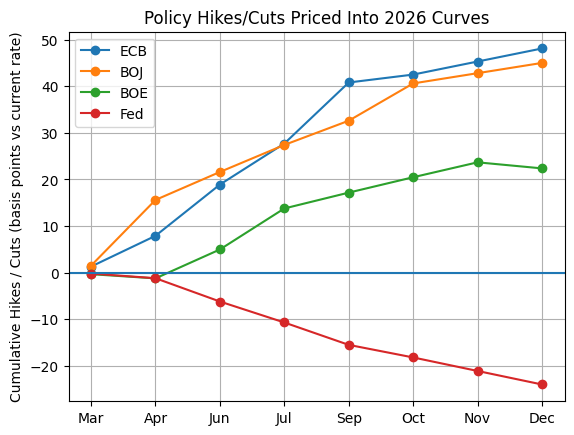

The timing of the conflict could hardly be more complicated for global central banks. A packed week of monetary policy meetings — including the Federal Reserve, Bank of England, European Central Bank, Bank of Japan, and the Reserve Bank of Australia — comes just as some policymakers were beginning to contemplate rate cuts after a period of tightening.

Before the outbreak of hostilities, inflation data had been moving in a relatively encouraging direction. US CPI surprised to the downside earlier in the week, suggesting the disinflationary trend was continuing. However, core PCE inflation remained firm at 3.1%, and that reading reflects January data, well before the recent surge in oil and refined fuel prices.

Now, policymakers must assess how much of the current energy shock will ultimately filter into broader inflation and economic activity. For some economies, particularly the United States where growth has remained relatively robust, there may be more room to absorb higher energy prices. For others, such as the UK, the situation is far more precarious. Growth there has been essentially stagnant, with recent GDP figures showing little to no expansion, while inflation remains above target and likely to remain elevated due to higher energy costs.

This creates a difficult policy environment. Central banks must decide whether to look through the shock, treating it as a temporary supply disruption, or respond to the inflationary implications more aggressively. Markets have already begun repricing expectations, with interest rate cuts being scaled back and, in some cases, even rate hikes being discussed for certain economies most exposed to energy price pressures.

Equity markets under pressure

Equity markets have begun to reflect these stagflation concerns. Markets in energy-importing economies, such as Germany and Japan, have seen particularly sharp declines, reflecting their vulnerability to higher oil prices and supply disruptions. Even US equities have begun to roll over, with the major indices increasingly struggling to maintain the momentum that carried them to record highs in recent months.

This shift may also be interacting with broader themes that were already developing before the conflict. In particular, investor enthusiasm around artificial intelligence and technology stocks had begun to show signs of fatigue, with valuations stretched and expectations increasingly difficult to justify. The geopolitical shock may now be acting as a catalyst for a broader reassessment of risk across equity markets.

S&P 500 daily chart

Past performance is not a reliable indicator of future results.

The dollar rises, gold struggles

One of the more counterintuitive market moves has been the weakness in gold despite rising geopolitical risk. Normally, gold would benefit from a flight to safety. However, several mechanical forces are working against it.

Gold had already experienced a significant rally over the past 18 months, leaving positioning relatively crowded. At the same time, the US dollar had been heavily sold as part of the “sell America” narrative that dominated markets for much of the past year. When the conflict erupted, investors rotated aggressively back into the dollar, which remains the world’s primary safe-haven currency.

There are also structural reasons for the dollar’s strength. Oil is priced in dollars, meaning that higher oil prices increase demand for the currency. Additionally, tighter financial conditions force investors and institutions to cover dollar-denominated liabilities, further boosting demand. These forces have pushed the dollar index back toward the psychologically important 100 level, a key technical resistance point that markets are watching closely.

US dollar index (DXY) daily chart

Past performance is not a reliable indicator of future results.

Looking ahead

For now, markets remain focused on the trajectory of the conflict and the status of the Strait of Hormuz. As long as energy flows remain constrained, the stagflation narrative is likely to persist. That means higher oil prices, a stronger dollar, tighter financial conditions, and continued pressure on risk assets.

At the same time, deeper financial stresses could be building beneath the surface. Rising corporate credit spreads and growing concerns around the private credit market suggest that tighter financial conditions may already be starting to ripple through the system.

Ultimately, the outlook for markets will hinge on how quickly the energy shock can be resolved. If the Strait of Hormuz reopens and energy flows normalize, markets could stabilize quickly. But if the disruption continues, the combination of higher inflation, slower growth and tightening financial conditions could pose a much more serious challenge for both policymakers and investors in the months ahead.