SCOTUS tariff ruling creates fresh uncertainty for US trade policy and global markets

The Supreme Court's decision will have ramifications for trade, fiscal, foreign and monetary policy.

The US Supreme Court's decision to slap down the tariffs levied by the Trump administration under the International Emergency Economic Powers Act has significant implications for trade, foreign, fiscal and monetary policy. The move is unsurprising, given the spurious argument put forward by the administration that any such emergency exists. Nevertheless, the ruling creates significant uncertainty going forward.

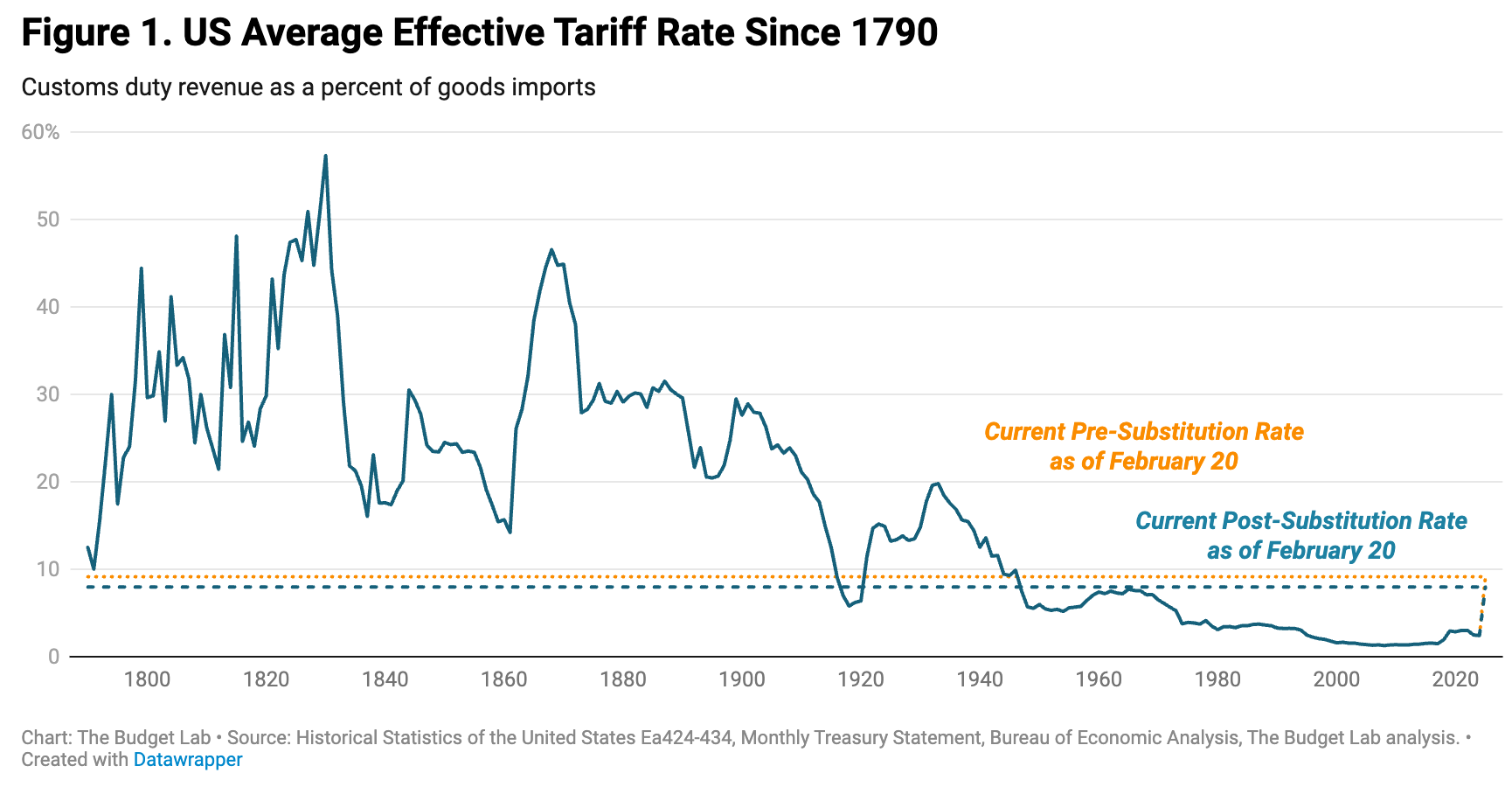

The Trump administration would have been prepared for the ruling. Immediately, it responded by levying new tariffs under the Trade Act of 1974. However, the tariffs are effectively capped at 15% and can only apply for a short period of time – incidentally, lowering the US average effective tariff rate. Any trade deal negotiated with an average tariff rate above that level has been thrown into doubt and basically relies on trading partners to accept tariff rates they may not have to.

(Source: Yale Budget Lab)

Trump has lost his favourite big stick and is now waving around a twig and yelling really loudly in hope that existing trade deals will be honoured. All else equal, it's not in the interest of US trading partners to stick to these deals. Knowing Trump's past behaviour, he will try to find other ways to cajole them into making or sticking to deals. That could mean bellicose threats about destroying military alliances, or imposing export curbs, sanctions or other measures, amplifying volatility as trade and foreign policy is worked out.

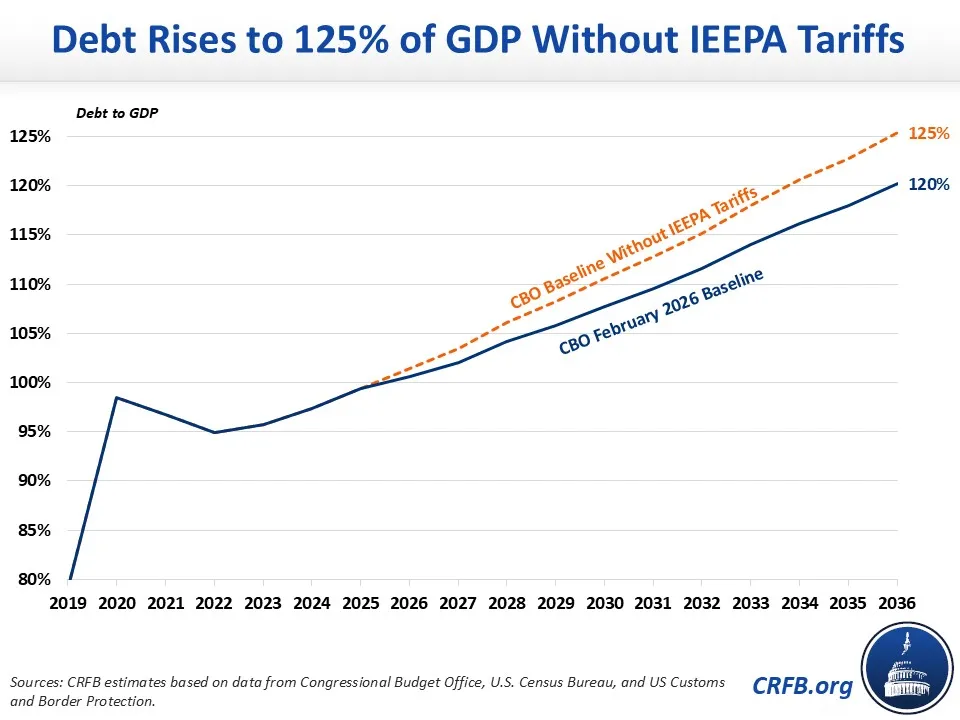

The reduction in the US tax intake from lower average tariffs will also be a problem for the US fiscal position. Although they weren't going to completely fill the hole, tariff revenues were going to help plug very big US fiscal deficits. Removing this revenue source means marginally higher deficits and debt in the long run. The Committee for a Responsible Budget estimates US debt-to-GDP could rise to 125% over the next ten years without the tariffs, compared to 120% with them.

(Source: Committee for a Responsible Federal Budget)

The change in trade policy also raises interesting questions about inflation and rates going forward. While the removal of tariffs could mean a level change in prices vis-a-vis lower goods prices, the elimination of an effective consumption tax is stimulatory and could mean greater spending elsewhere, especially in the services sector. That could lead to stickier and lumpier inflation, and possibly interest rates that are higher than they would otherwise be.

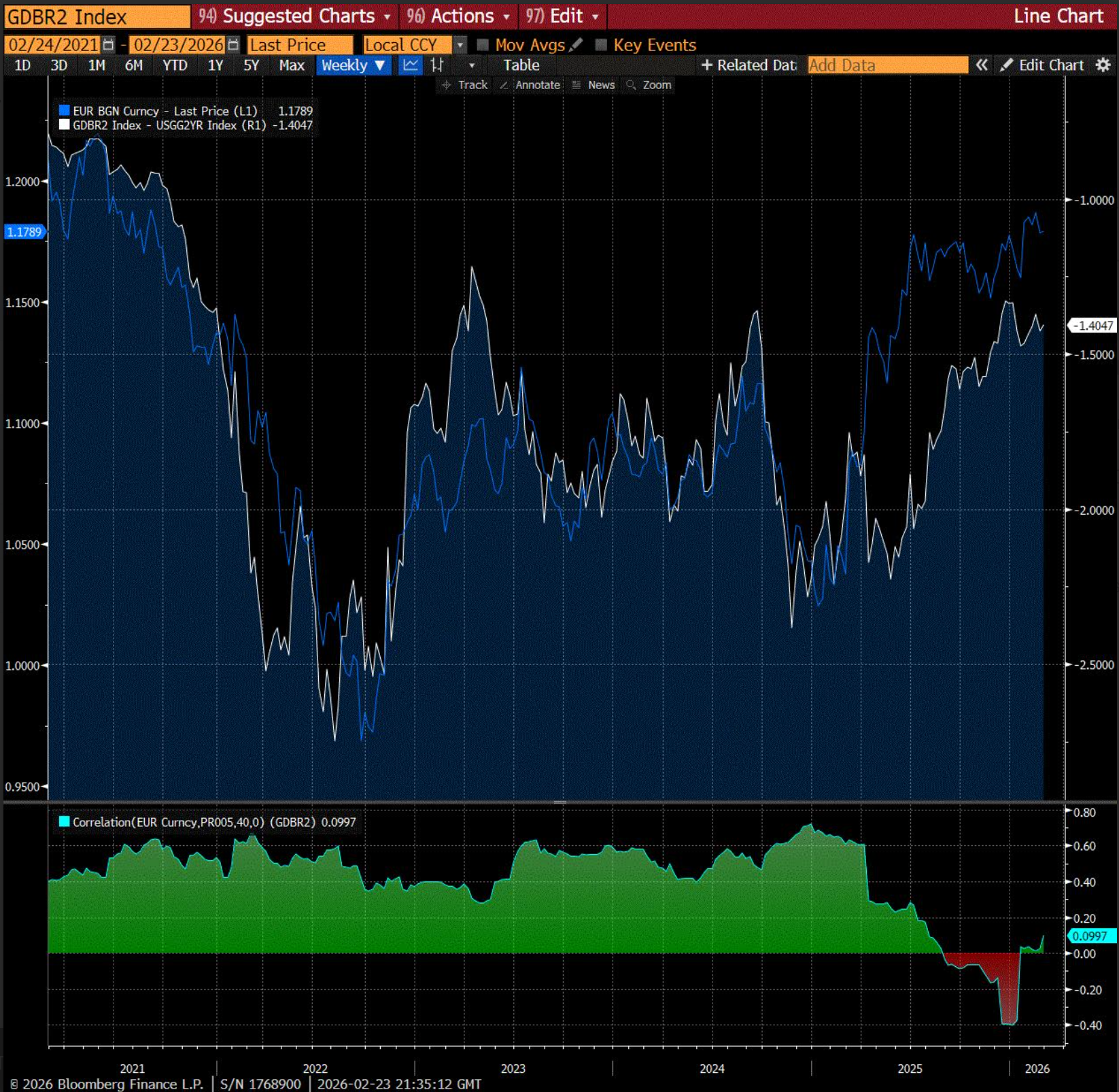

For the markets, trade policy volatility, and its knock on effects, is a source of uncertainty and has been reflected in a lower US Dollar and lower Treasury prices. As can be seen in the chart below of the EUR/USD and the 2-year spread between Treasury and Bund yields, it inflames the “sell America” trade. It has also supported another rally in gold. The situation is more nuanced for equities. On the one hand, it too increases the risk premium in equities. On the other hand, a lower level of tariffs is a boost to growth and profits.

(Source: Bloomberg, Capital.com)

While uncertainty will prevail for a while, there is a silver lining in the long run. The Supreme Court ruling shows that the judiciary remains independent and more loyal to the constitution than their political allies or a President that, for at least three of the justices, put them in the job. That should be reassurance that the system is working as intended, watering down the “sell America” narrative eventually and restoring trust in the government, all else equal.