BoE and ECB preview: caught between inflation shock and growth risks

The Bank of England and European Central Bank are expected to leave rates unchanged as they balance rising inflation and slowing growth.

This week’s Bank of England and European Central Bank meetings come at a particularly delicate moment, with policymakers facing a classic energy-driven dilemma: inflation is rising again due to the Iran conflict, but growth is already fragile.

Markets and economists are broadly aligned in expecting no change in rates from either central bank. The Bank of England is likely to keep Bank Rate at 3.75%, while the ECB is expected to hold its deposit rate around 2%. But the real story is not the decision, it’s the shift in the reaction function.

The war in the Middle East has reintroduced upside risks to inflation and downside risks to growth, a textbook stagflation setup. Higher oil and gas prices are already feeding into headline inflation, and both central banks have acknowledged that this will likely push inflation above target in the near term. That leaves policymakers in a bind: either tighten policy and risk choking growth, or ease policy and risk entrenching inflation.

BoE: stuck in the middle

The Bank of England arguably faces the toughest position. The UK is a net energy importer, making it more sensitive to rising prices, while growth remains weak.

What to expect:

- A hold with a cautious tone

- Emphasis on sticky services inflation and wages

- Pushback against immediate rate cuts, but also reluctant to commit to rate hikes

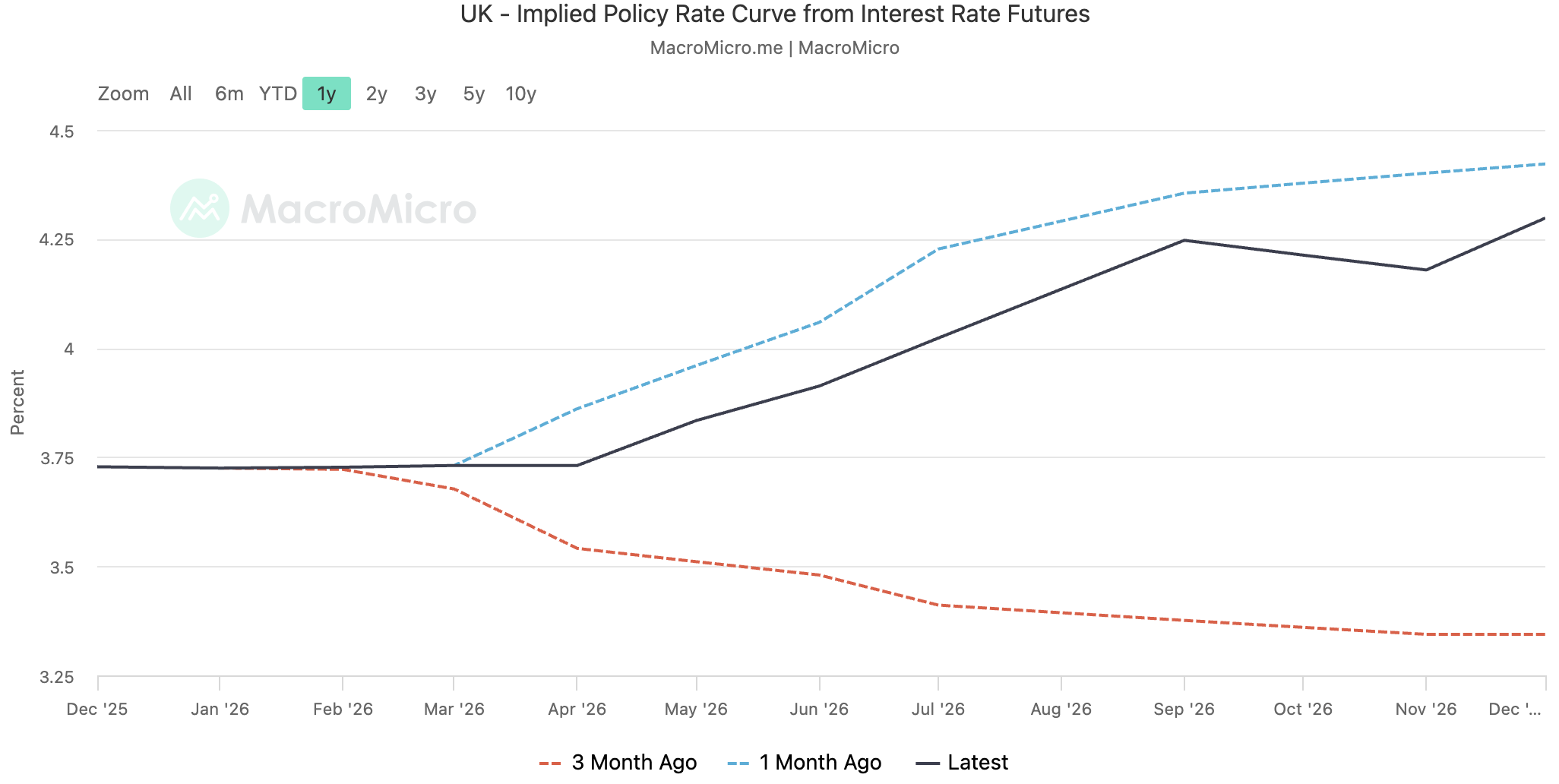

Markets may come away with the message that cuts are further away than previously thought, even if hikes are no longer expected. The current pricing reflects a year-end rate curve with two rate hikes from where the rate is now. The chart below highlights the swing in expectations as markets have reacted to the conflict in the Middle East, moving from two rate cuts before the conflict started, as a result of easing inflation and growth at the end of 2025, to the likelihood of a rate hike or two. The BoE pushed back on these expectations at the previous meetings, highlighting that the markets had gotten too far ahead of itself given the rise in energy is expected to be transitory, or at least that’s the hope.

ECB: closer to tightening bias

The ECB, by contrast, may sound slightly more hawkish. Inflation in the eurozone has already been revised higher due to the conflict, and policymakers have explicitly said rate hikes are “an option” if energy pressures persist.

What to expect:

- A neutral-to-hawkish hold

- Strong focus on inflation risks from energy

- Less urgency around supporting growth than the BoE

Data from the ECB Watch tool shows that current pricing reflects two 25bps rate hikes from the central bank in the next five meetings, with the first one potentially in the next meeting in June. The ECB may want to push back against these expectations if it believes markets are getting ahead of themselves.

What markets will really be watching

With no major policy changes expected, the focus will shift firmly to communication. Investors will be paying close attention to forward guidance, particularly whether expectations for rate cuts are being pushed further out. The tone on inflation will also be key, with any emphasis on persistence likely reinforcing a higher-for-longer narrative. Finally, policymakers’ assessment of the energy shock — whether it is viewed as temporary or more structural — will play a crucial role in shaping market expectations.

Both central banks are likely to deliver a broadly “wait-and-see” message, but with a subtle shift in emphasis. The easing cycle appears to have been paused, inflation risks are back in focus, and policy uncertainty remains elevated. In short, this week is less about what central banks do, and more about how they reframe the path ahead in a world where energy is a dominant driver of the macro narrative.