ECB preview: rate hike expected as inflation risks return

Stubborn inflation has led markets to price in a rate hike from the ECB, but the tone of the meeting will be key.

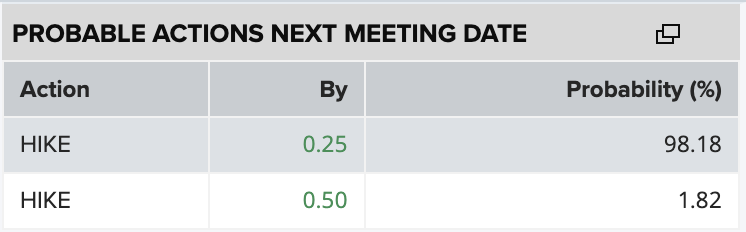

The European Central Bank meets this week with markets overwhelmingly expecting a rate hike, marking a clear shift from the easing narrative that dominated earlier in the year. The deposit rate is currently at 2%, and markets are pricing roughly a 98% chance of a 25-basis-point increase, with some probability attached to a larger move. The reason is straightforward: inflation risks have re-emerged, largely because the Middle East conflict and disruption around energy flows have pushed oil and input costs higher across the eurozone.

Source: Refinitiv

Data and ECB members support a hike

The data supports the case for tightening. Eurozone inflation rose to 3.2% in May from 3.0% in April, while core inflation also moved higher, suggesting the pressure is not limited to headline energy effects. Services inflation and manufacturing input costs have also increased, raising concern that the energy shock is starting to broaden into other areas of the economy.

ECB commentary has also leaned in this direction. Governing Council members have made it clear that a June hike would be warranted if the inflation outlook failed to improve materially. Bundesbank President Joachim Nagel said that if the inflation outlook did not improve markedly, that would argue for a rate hike, while other policymakers have warned that the ECB must remain ready to act if the energy shock proves persistent.

The difficulty for the ECB is that this is not a clean inflation story. Europe is facing risks of a stagflationary environment: weaker growth momentum, higher imported energy costs and renewed pressure on household purchasing power. That makes this meeting important not only because of the rate decision itself, but because of what President Lagarde says about the path ahead. Markets will be watching whether the ECB frames June as a one-off adjustment or the start of a broader tightening cycle.

Market impact

For European equities the impact is likely to depend on the tone. A 25-basis-point hike is largely priced in, so the immediate reaction may be limited if the ECB delivers without sounding too aggressive. However, a signal that further back-to-back hikes are possible could weigh on rate-sensitive and cyclical sectors, particularly industrials, autos and real estate. The DAX 40 has benefited recently from improving sentiment around a potential Middle East de-escalation, but Germany’s energy dependence and industrial-heavy composition mean it remains vulnerable if higher rates and higher energy costs combine to pressure margins.

DAX 40 daily chart

Past performance is not a reliable indicator of future results.

The euro could find support if the ECB refuses to rule out further hikes, especially if markets believe the Fed is moving more cautiously. A hawkish ECB would improve the euro’s rate differential relative to currencies where central banks are more hesitant to tighten. However, the upside may be capped if investors conclude that tighter policy will worsen Europe’s already fragile growth outlook.

EUR/USD daily chart

Past performance is not a reliable indicator of future results.

Overall, the ECB is likely to deliver a tentative hike: tightening because inflation risks demand it, not because the economy is strong. For markets, the key question is whether this is viewed as inflation discipline or a policy mistake in the making. That distinction will determine whether the euro extends gains and whether European equities can continue to recover or begin to lag again.