US Dollar slides on “sell America” trade and ahead of critical economic data

The latest batch of US jobs and inflation data could inform the timing of the next Fed cut

The US Dollar continues to come under pressure from persistent political risk premium and going into US Non-Farm Payrolls and CPI data.

The “sell America” trade persists and weighs on USD

The US Dollar remains under pressure amidst the ongoing so-called “sell America” trade. In response to erratic trade and foreign policy, the US Dollar has depreciated as investors reduce exposure to US Dollar denominated assets.

The narrative has been amplified in recent days, following reports that the Chinese government has instructed its financial institutions to reduce exposure to Treasuries due to uncertainty and volatility. The story comes off the back of similar reports in Europe, where some funds flagged their intent to lighten allocations to US debt following ongoing trade policy uncertainty and US threats to take-over Greenland.

US economic data to test Fed rate cut expectations

Recent US economic data continues to paint a mixed picture of the US economy. Economic activity remains strong, with recent US GDP figures for Q3 showing robust growth and the Atlanta Federal Reserve’s “nowcaster” indicating q/q growth of 4.2%.

Despite strong growth, labour market conditions in the US remain lukewarm. The source of this weakness remains a cause for debate. While some indicators suggest weaker labour demand because of pockets of weakness in the US economy, supply side factors like immigration policy or the impacts of artificial intelligence are also possible contributors.

The delayed Non-Farm Payrolls data for January is tipped to show this lukewarmness continues. Economists forecast that the US economy added 68,000 jobs in November, with the unemployment rate unchanged from a month earlier at 4.4%. Market participants are preparing for a potentially soft print, however, after Director of the National Economic Council Kevin Hassett warned of smaller jobs growth due to slowing population growth and higher productivity.

Reassuringly, the week’s inflation data is projected to show easing price pressures in the US economy. Forecasters estimate that both headline and core CPI moderated to 2.5% in January, the lowest level for headline inflation since the introduction of the “Liberation Day” tariffs and the lowest level for core inflation in almost five years.

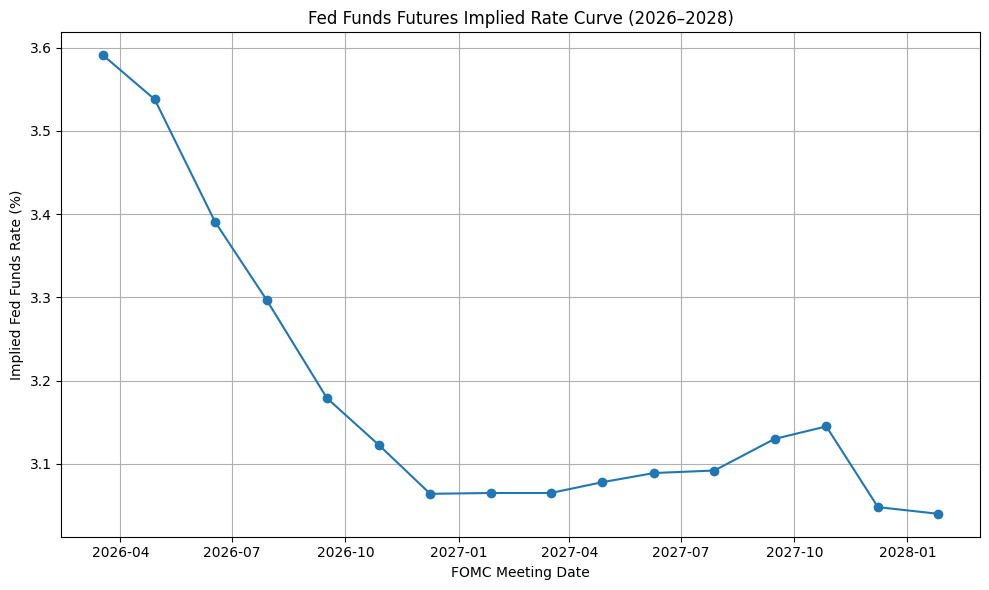

The combination of moderate jobs growth and moderating inflation is fuelling expectations for further rate cuts from the US Federal Reserve this year. The first move is fully baked-in for June, incidentally, the likely first meeting of Fed Chair nominee Kevin Warsh, who has advocated for lower rates.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

USD remains in downtrend on rate cuts and “Sell America”

The combination of expected rate cuts and the risk premium being baked into US assets is keeping the US Dollar in a downtrend. A benign inflation print and soft Non-Farm Payroll report could bring forward the timing of the next Fed cut at the margins and deepen the implied trough rate slightly. Meanwhile, an upside surprise in inflation could cast doubts over the Fed’s ability to continue easing and lean against the Dollar’s primary trend.

The EUR/USD remains in a steady uptrend as traders seek-out alternatives to Dollars. From a technical point of view, short-term support appears to be around 1.1767 and the 20-day moving average. Resistance looks to be around the pair’s recent higher-high at 1.2084.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)