Oil spikes and recession fears: signal or false alarm?

A crude oil spike often precedes a recession. Should we be worried this time around?

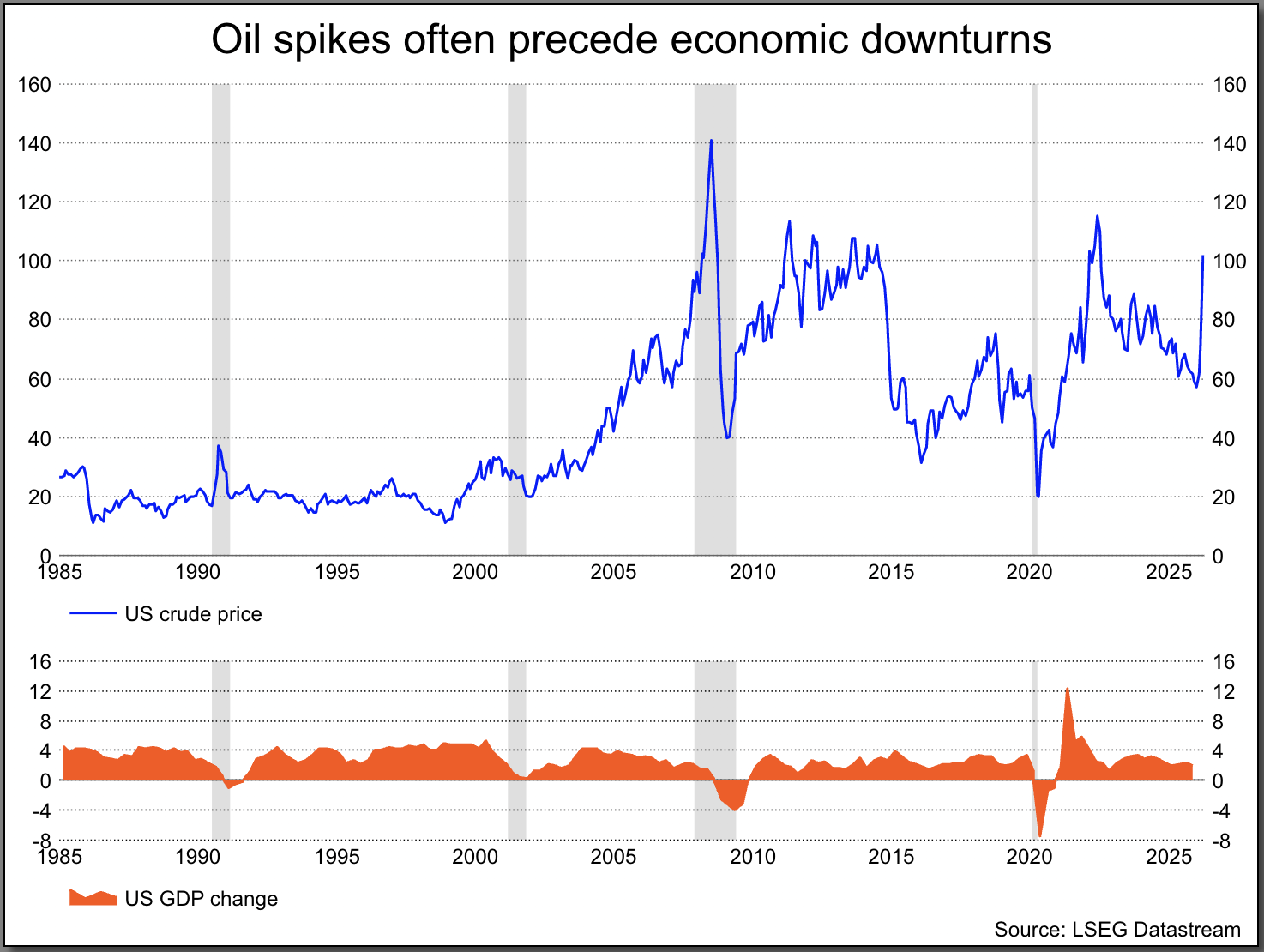

History offers a sobering pattern: nearly every US recession since World War II has been preceded by a sharp rise in oil prices. The mechanism is intuitive — higher energy costs act as a tax on consumers and businesses, squeezing margins, reducing disposable income and tightening financial conditions. Against that backdrop, the recent surge in crude has naturally revived concerns about whether the global economy is heading toward a similar outcome.

Why this cycle looks different

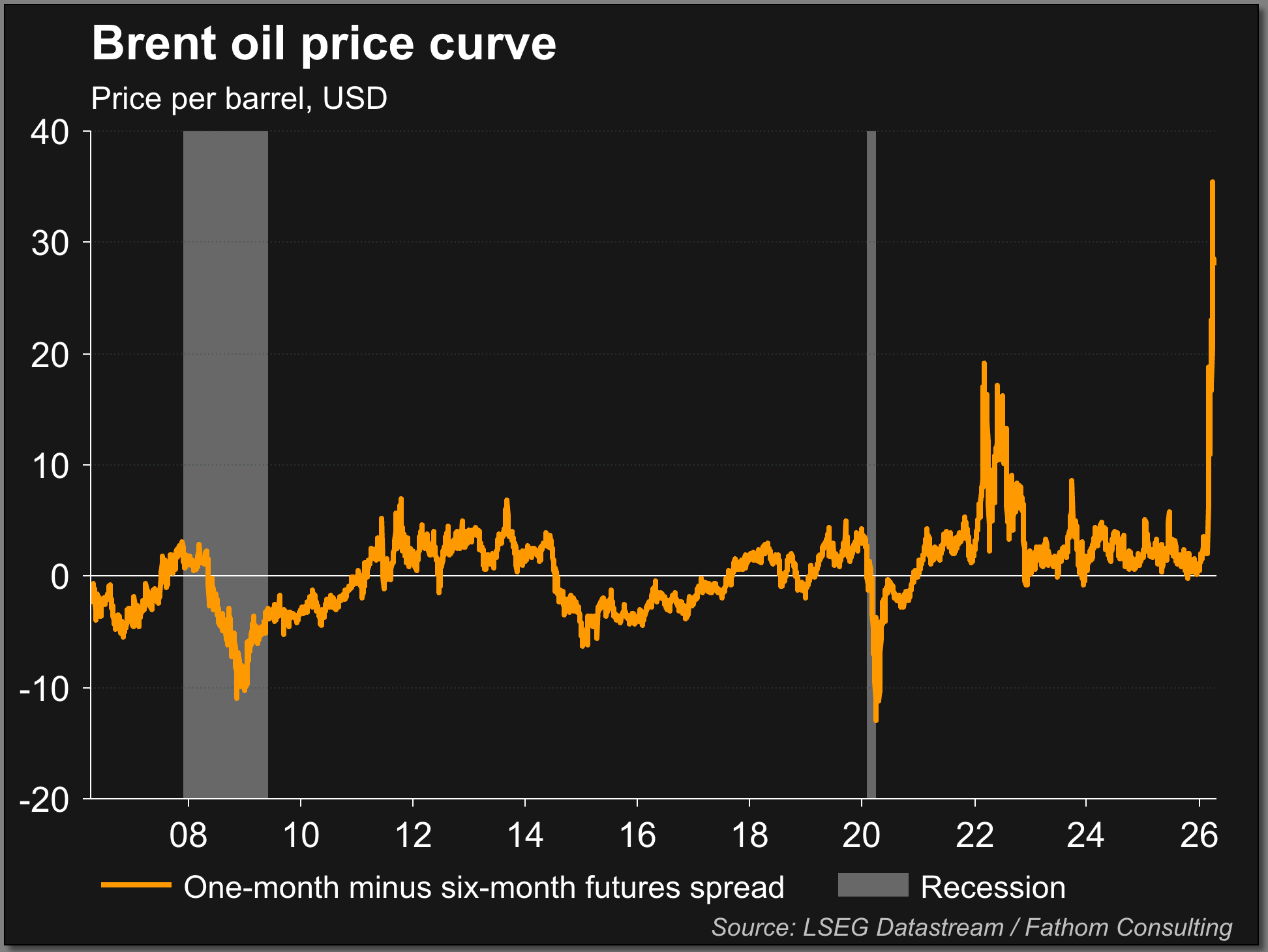

However, the current situation is more nuanced. While front-month crude prices have risen sharply, the futures curve is in steep backwardation, meaning near-term prices are elevated but longer-dated contracts are significantly lower. In simple terms, the market is pricing a short-term shock rather than a sustained structural increase in energy costs. That distinction matters. Historically, the most damaging oil shocks have been those that persist — embedding themselves into inflation, wages and expectations. A temporary spike, even a sharp one, is less likely to trigger a full-blown recession unless it drags on.

That said, the risk cannot be dismissed. Even a short-term energy shock can have second-round effects, particularly if it feeds into broader inflation expectations. This is where the macro backdrop becomes critical. Unlike past cycles, the economy is already dealing with elevated interest rates and tighter financial conditions. If higher oil prices delay rate cuts or push yields higher, the cumulative effect could still weigh on growth, even if the shock itself is temporary.

Oil spread > 0 = backwardation

Earnings season becomes the key test

This is where the upcoming earnings season becomes particularly important. So far, equity markets have shown resilience, in part because earnings expectations remain strong. Analysts are still projecting solid growth, and valuations have adjusted to levels that some consider more reasonable. However, these expectations have yet to fully incorporate the recent rise in energy costs. Companies in energy-intensive sectors, like industrials, transportation, chemicals and parts of consumer goods, are likely to face margin pressure as input costs rise.

The key question is whether companies can pass these costs on. If demand remains resilient, firms with pricing power may be able to protect margins, supporting earnings and justifying current valuations. In that scenario, the market’s resilience could prove justified. However, if higher costs coincide with softer demand, margins could compress more quickly than expected. That would likely trigger downward revisions in earnings, which is often a more powerful driver of equity declines than macro headlines alone.

Forward guidance will be even more telling than the backward-looking numbers. Investors will be watching closely for any shift in tone, particularly around cost pressures, demand trends and capital expenditure plans. If companies begin to signal caution or uncertainty, it could challenge the market’s current optimism. Conversely, if guidance remains broadly constructive, it suggests that the economy is absorbing the shock better than feared.

The bottom line

Ultimately, the oil-recession link is a warning, not a certainty. The current backwardation in crude suggests the market does not yet believe in a prolonged energy crisis. But that view is contingent on the geopolitical situation stabilising. If the conflict persists and keeps energy prices elevated, the risk of a more sustained economic slowdown will increase.

For now, markets are walking a fine line. They are acknowledging the risk but not fully pricing a recession. Earnings season will be the first real test of whether that stance is justified or whether the oil shock is beginning to feed through in ways that history suggests should not be ignored.

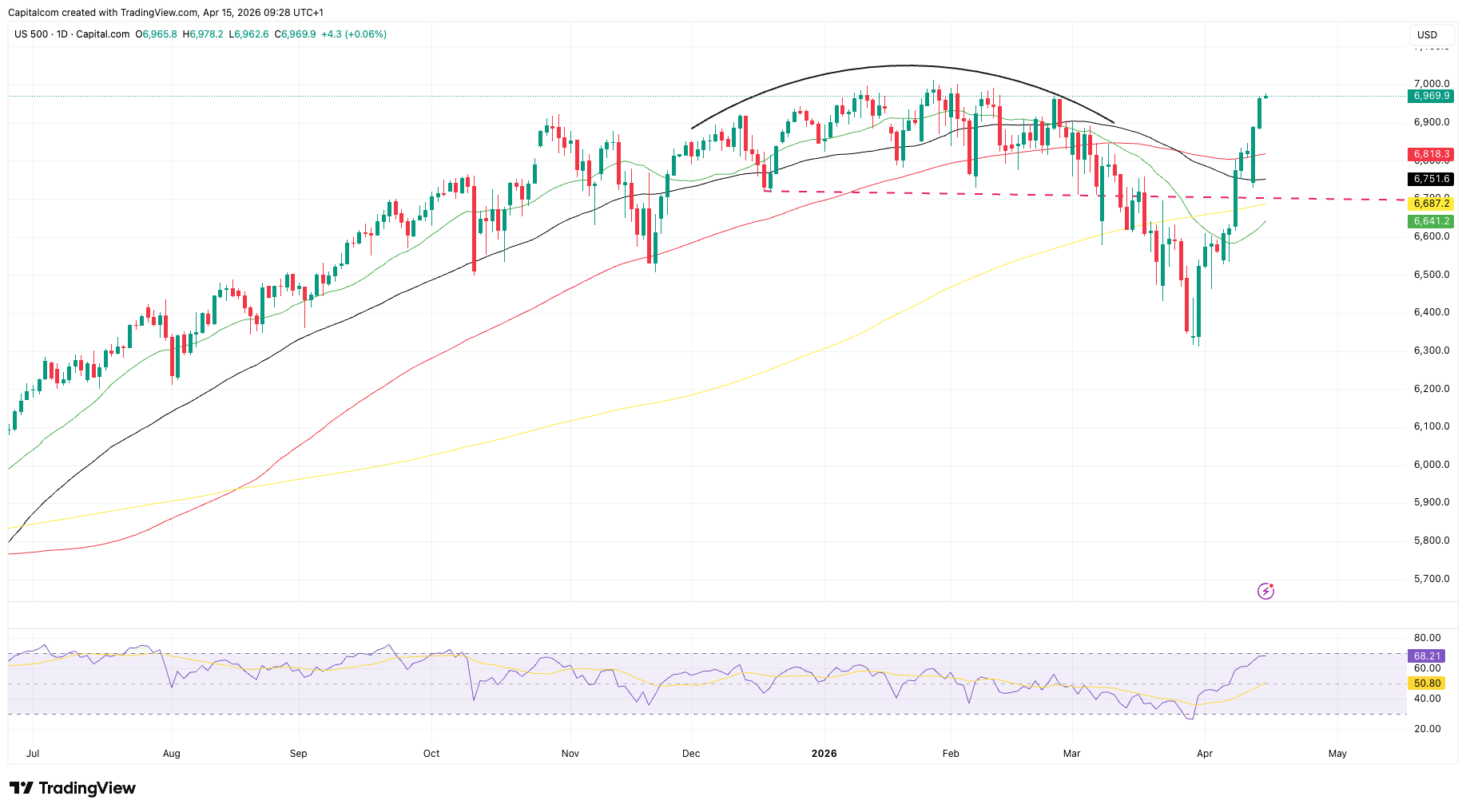

S&P 500 daily chart – resilience in the stock market despite higher energy

Past performance is not a reliable indicator of future results.