Palantir stock forecast: Q1 earnings in focus

Palantir is a US software company due to report Q1 2026 results on 4 May, with investors also tracking NHS contract scrutiny in the UK and Project Maven in the US. Explore third-party PLTR price targets and technical analysis. Past performance is not a reliable indicator of future results.

Palantir Technologies Inc. (PLTR) is trading at $141.33 in early European trading as of 9:56am UTC on 29 April 2026, within a session range of $140.70–$142.84. Past performance is not a reliable indicator of future results.

Sentiment ahead of the Q1 2026 earnings release on 4 May 2026 after market close, with consensus expecting revenue of approximately $1.54 billion, is shaping near-term positioning as investors weigh prior-quarter US commercial revenue growth of 137% year-on-year against broader valuation concerns (MarketBeat, 27 April 2026). At the same time, the UK government's public consideration of invoking a break clause in Palantir's £330 million NHS Federated Data Platform contract has added uncertainty around the company's international commercial pipeline (The Register, 20 April 2026), while the Pentagon's March 2026 formalisation of Project Maven as a long-term programme of record continues to underpin Palantir's US defence revenue outlook (Military.com, 25 March 2026).

Third-party Palantir outlook: Q1 earnings near, targets split

As of 29 April 2026, third-party Palantir stock forecasts for 2026–2030 reflect a range of views shaped by Palantir's AI platform demand, US government contract momentum, and multiple compression across high-growth software names ahead of the Q1 2026 earnings report. The following targets summarise leading third-party views on PLTR.

Mizuho Securities (outperform, target trimmed)

Mizuho analyst Gregg Moskowitz reduced PLTR's 12-month price target to $185 from $195, maintaining an outperform rating. The firm cites valuation recalibration in large-cap software ahead of Q1 earnings as the driver of the trim, while noting that demand conditions for AI-linked platforms remain healthy and that Palantir's risk/reward profile is seen as more compelling than that of several peer software names (MarketScreener, 14 April 2026).

D.A. Davidson (neutral, reaffirmed)

D.A. Davidson reiterates a neutral rating and maintains a $180 price target on PLTR, noting that the firm continues to regard Palantir as one of the strongest businesses in the software sector. The neutral rating reflects valuation concerns alone, with the stock trading at approximately 225 times trailing earnings; the firm states that the price target is under review pending Q1 results (MarketBeat, 16 April 2026).

Morgan Stanley (equal-weight, maintained)

Morgan Stanley analyst Sanjit Singh maintains an equal-weight rating and a $205 price target on PLTR, flagging that the company could modestly accelerate growth and raise its full-year guidance ahead of the Q1 report due on 4 May. The bank notes that even stronger earnings outperformance may be needed for the stock to move materially higher in the near term, given that blockbuster quarters are already the baseline expectation, while field checks point to sustained US momentum (TheStreet, 17 April 2026).

Citigroup (buy, target reduced)

Citigroup analyst Tyler Radke lowered PLTR's price target to $210 from $260, retaining a buy rating. The firm raised its Q1 earnings estimates ahead of the May report while cutting the target to reflect recent multiple compression across the software sector; Citi flags continued contract momentum, including large renewals with Airbus and Stellantis, and describes Palantir as one of the top AI beneficiaries (Yahoo Finance, 28 April 2026).

MarketBeat (consensus overview)

MarketBeat aggregates ratings from analysts covering PLTR and reports an average 12-month consensus price target of $196.35, with a moderate buy consensus rating. The breakdown includes 15 buy, 11 hold, and 2 sell ratings; individual estimates range from $45 to $260, reflecting persistent divergence over whether Palantir's valuation premium, at approximately 232 times earnings, is sustainable against its 61% guided revenue growth for fiscal 2026 (MarketBeat, 24 April 2026).

Predictions and third-party forecasts are inherently uncertain, as they cannot fully account for unexpected market developments. Past performance is not a reliable indicator of future results.

PLTR stock price: Technical overview

The PLTR stock price trades at $141.33 as of 9:56am UTC on 29 April 2026, sitting just below its 20-day simple moving average (SMA) near $143 and beneath the 50-day SMA at $145. The short-term moving average cluster of 20-, 50-, 100- and 200-day SMAs at approximately $143, $145, $157 and $164 sits above the current price, indicating that PLTR trades below all four key reference levels on the daily chart, according to TradingView data.

The 14-day relative strength index (RSI) sits at 46.79, a neutral reading that carries no directional bias in isolation. The average directional index (ADX) of 12.12 signals a weak trend environment, suggesting that recent price action lacks clear directional conviction.

On the classic pivot framework, the pivot point at $148.33 represents the first reference overhead; a daily close above that level would put the R1 level near $160 in view. On the downside, the Hull moving average at $141.74 and the volume-weighted moving average (VWMA) at $140.21 sit close to the current price, with the classic S1 at $134.25 as the next downside reference if those near-term levels give way (TradingView, 29 April 2026).

This technical analysis is for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any instrument.

Palantir share price 2024–2026

PLTR’s stock price closed at approximately $22 on 30 April 2024, trading in a relatively narrow range through the spring and summer of that year as the broader AI investment narrative began to gather pace.

The stock broke out sharply in Q4 2024, climbing from around $37 in late September to above $75 by year-end, lifted by strong quarterly earnings and growing enthusiasm around its AI Platform (AIP), and it closed 2024 at $75.24. That momentum carried into early 2025, with PLTR reaching an intraday peak of $222.05 on 3 November 2025 amid post-US election sentiment and accelerating US government AI contract awards, including Project Maven and a $1 billion Department of Homeland Security deal.

A retracement followed through Q1 2025, with the stock sliding to around $65–$67 in January 2025 before recovering gradually through the remainder of that year. A sharp sell-off struck in early April 2025, with PLTR touching lows near $65.59 on 7 April, coinciding with broad market volatility triggered by the Trump administration's tariff announcements. A recovery through the summer saw the stock climb back towards the $155–$190 range by August and September 2025.

PLTR closed 2025 at $177.60 and opened 2026 around $169–$174, before pulling back through the first quarter. As of 29 April 2026, the stock trades at $141.33. That leaves it approximately 20.4% down year to date and around 36.4% below its November 2025 high.

Past performance is not a reliable indicator of future results. Share prices are indicative and may differ from live market prices.

Palantir Q1 2026 earnings: History and upcoming results

Palantir is scheduled to report Q1 2026 results on 4 May 2026 after market close, with analyst consensus pointing to revenue of approximately $1.54 billion (BusinessWire, 13 April 2026). This aligns closely with Palantir's own guidance of $1.532–$1.536 billion for the quarter and is in line with its full-year 2026 revenue guidance of $7.182–$7.198 billion, implying roughly 61% year-on-year growth (Tickeron, 23 April 2026).

The Q4 2025 report, published on 2 February 2026, delivered revenue of $1.41 billion – up 70% year-on-year – with US commercial revenue surging 137% year-on-year and US government revenue growing 66% year-on-year on expanded AI platform contracts (Yahoo Finance, 2 February 2026). Palantir raised its full-year 2026 guidance on the back of those results, projecting revenue of $7.18–$7.20 billion, citing strong pipeline conversion through its AIP bootcamp model and accelerating enterprise AI adoption (Investing.com, 2 February 2026).

Despite that beat, PLTR shares fell sharply in the sessions that followed as investors rotated out of high-multiple software names amid a broader sector re-rating, with the stock declining approximately 27% over the 30 days following results (TIKR, 15 February 2026). This serves as a reminder that at elevated valuation multiples, strong results do not automatically translate into price gains, as multiple contraction can offset fundamental outperformance (MarketBeat, 27 April 2026).

The Q1 2026 report will be watched for updates on US government contract renewals, commercial customer count growth – which rose 34% year-on-year in Q4 2025 – and any management commentary on the trajectory of the AIP bootcamp pipeline and international expansion (Yahoo Finance, 13 April 2026).

Past performance is not a reliable indicator of future results.

Palantir (PLTR): Capital.com analyst view

PLTR's price trajectory over the past two years reflects the sharp swings that can accompany high-growth, high-valuation technology stocks. The stock rose roughly 650% between April 2024 and its November 2025 peak near $222.05, driven by expanding US government AI contracts, strong commercial platform adoption, and broad enthusiasm around artificial intelligence investment themes. That said, PLTR's premium valuation, with the stock trading at over 200 times earnings for much of 2025 and into 2026, means that it remains sensitive to shifts in macro sentiment. The April 2025 tariff-driven sell-off and the subsequent 2026 drawdown both illustrate how quickly risk appetite can reverse for high-multiple names.

Heading into the Q1 2026 earnings report due on 4 May, several factors pull in competing directions. Palantir's expanding US defence and intelligence contract base, including programme-of-record status for Project Maven, supports a structural revenue argument; however, ongoing scrutiny of its £330 million NHS contract in the UK and broader questions about customer concentration introduce execution risk. The company's 2026 revenue guidance of approximately $7.19 billion implies continued rapid growth, but whether that is already priced in at current multiples remains a key point of debate among analysts, with consensus price targets ranging widely from $45 to $260.

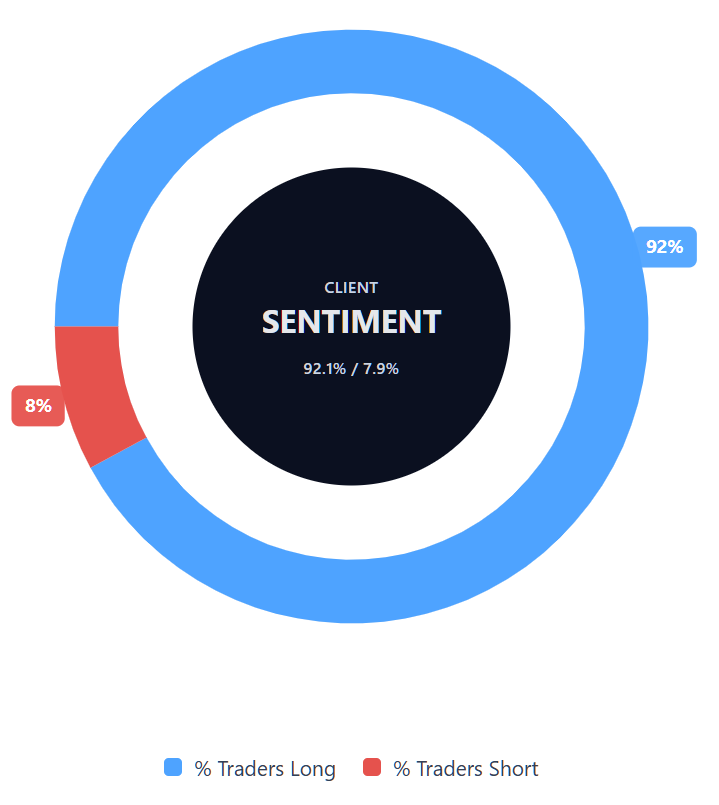

Capital.com’s client sentiment for Palantir CFDs

As of 29 April 2026, Capital.com client positioning in Palantir CFDs stands at 92.1% buyers versus 7.9% sellers. That puts buyers ahead by 84.2 percentage points and places sentiment firmly in one-sided long territory. This snapshot reflects open positions on Capital.com and can change rapidly as market conditions evolve.

Summary – Palantir 2026

- As of 9:56am UTC on 29 April 2026, PLTR trades at $141.33, down roughly 20% year to date and around 36% below its November 2025 all-time high near $222.05.

- Key price drivers include US government AI contract momentum, Palantir's 2026 revenue guidance of approximately $7.19 billion, and broader tech sentiment ahead of the 4 May Q1 earnings report.

- The UK government's consideration of a break clause in Palantir's £330 million NHS contract adds international revenue uncertainty alongside the company's existing valuation premium concerns.

Past performance is not a reliable indicator of future results.

FAQ

Who owns the most Palantir stock?

What is the five-year Palantir share price forecast?

Is Palantir a good stock to buy?

Could Palantir stock go up or down?

Should I invest in Palantir stock?

Can I trade Palantir CFDs on Capital.com?

Yes, you can trade Palantir CFDs on Capital.com. Trading share CFDs lets you speculate on price movements without owning the underlying asset and to take long or short positions. However, contracts for difference (CFDs) are traded on margin, and leverage amplifies both profits and losses. You should ensure you understand how CFD trading works, assess your risk tolerance, and recognise that losses can occur quickly.