Arm Holdings stock forecast: Q4 earnings in focus

Arm Holdings is a UK-based chip designer whose shares are under pressure after TSMC exited its stake, as markets also assess its AGI CPU strategy and upcoming 6 May earnings. Explore third-party ARM price targets and technical analysis. Past performance is not a reliable indicator of future results.

Arm Holdings plc (ARM) is trading at $203.95 as of 1:53pm UTC on 29 April 2026, within an intraday range of $195.62–$214.71. Past performance is not a reliable indicator of future results.

The retreat follows TSMC's full exit from its ARM position: subsidiary TSMC Partners sold 1.11 million shares between 28–29 April at $207.65 each, raising approximately $231 million and ending TSMC's remaining equity interest in the company (Silicon Republic, 29 April 2026). That overhang has pressured the stock, even as broader semiconductor sentiment remains constructive, with the iShares Semiconductor ETF (SOXX) up more than 30% since the late-March market low (Intellectia AI, 23 April 2026). ARM's upcoming Q4 fiscal year 2026 earnings release, scheduled for 6 May 2026, is also drawing attention (Arm newsroom, 8 April 2026), while the March 'Arm Everywhere' event, at which CEO Rene Haas unveiled the AGI CPU data centre processor, continues to underpin the stock's multi-week re-rating from its 30 March close near $136.96 (Stock Titan, 23 March 2026).

Third-party ARM outlook: Q4 earnings near as targets diverge

As of 29 April 2026, third-party Arm Holdings stock forecasts for 2026–2030 follow the company's investor day in late March, the unveiling of its AGI CPU, and a near-90% rally from the 30 March close of $136.96.

Morgan Stanley (equal-weight reaffirmation)

Morgan Stanley reaffirms an Equal Weight rating on ARM and lifts its 12-month price target to $150 from $135. The firm cites near-term risks as the main constraint on a more constructive stance, even amid improving fundamentals across the semiconductor sector (Investing.com, 7 April 2026).

Susquehanna (positive target raise)

Susquehanna raises its price target on ARM to $210 from $170, maintaining a Positive rating. The firm cites ARM's AGI CPU product as evidence that the investment case extends beyond smartphone royalties, noting the potential for earnings per share above $10 over the coming years even as smartphone royalty pressure persists (Yahoo Finance, 22 April 2026).

Evercore ISI (outperform target raise)

Evercore ISI lifts its price target on ARM to $227, retaining an Outperform rating, while projecting a path to $15 billion in FY2031 revenue and earnings per share above $9. The firm adds that longer-term earnings scenarios could reach the low-$20s range if ARM executes on server CPUs and agentic AI workloads (StocksToTrade, 24 April 2026).

Wells Fargo (overweight target raise)

Wells Fargo raises its price target on ARM to $220 from $175, maintaining an Overweight rating. Analyst Joe Quatrochi cites ARM's AI infrastructure positioning as the main rationale, with the revision arriving just ahead of the company's Q4 fiscal year 2026 earnings release scheduled for 6 May 2026 (Investing.com, 27 April 2026).

MarketBeat (consensus overview)

MarketBeat aggregates a consensus Moderate Buy rating on ARM from 25 analysts, with a 12-month average price target of $174.83; individual targets span $100–$240. The breadth of that range reflects competing assessments of ARM's royalty-model transition, with the consensus sitting well below the stock's then-current price of $215.88 after the sharp multi-week rally (MarketBeat, 27 April 2026).

Predictions and third-party forecasts are inherently uncertain, as they cannot fully account for unexpected market developments. Past performance is not a reliable indicator of future results.

Arm Holdings earnings: Q4 fiscal year 2026 preview

Arm Holdings is scheduled to report results for the fourth quarter of fiscal year 2026, ending 31 March 2026, on 6 May 2026 after market close, with a conference call via audio webcast at 2pm Pacific Time (10pm BST) (Arm newsroom, 8 April 2026).

When Arm issued its Q3 fiscal year 2026 results on 4 February 2026, the company guided for Q4 revenue of approximately $1.18 billion at the midpoint, implying around 18% year-on-year growth, a step down from the 26% expansion recorded in Q3. Adjusted earnings per share guidance was set at $0.54–$0.62 for the quarter, as Arm flagged a moderation in the pace of royalty growth even as licence demand remained firm (Wall Street Journal, 4 February 2026).

At the 'Arm Everywhere' investor event on 23 March 2026, chief financial officer Jason Child reaffirmed the Q4 guidance range, with no material revision to the prior outlook (TipRanks, 24 March 2026). MarketBeat notes that ARM's earnings are expected to grow approximately 28.89% in the next fiscal year, from $0.90 to $1.16 per share, based on analyst consensus as of late April 2026 (MarketBeat, 27 April 2026).

Arm Holdings stock price: Technical overview

The ARM stock price trades at $203.95 as of 1:53pm UTC on 29 April 2026, well above its key moving-average cluster. The 20/50/100/200-day SMAs sit at approximately $170 / $145 / $131 / $140, with price holding a meaningful premium to all four. The 20-over-50 alignment remains intact within that SMA family, which leaves the near-term trend constructive by that measure.

Momentum readings from TradingView place the 14-day relative strength index at 62.92, an upper-neutral reading that reflects firm but not yet stretched buying pressure. The average directional index at 36.68 indicates that an established trend is in place, per TradingView's oscillator data.

On the topside, the classic R1 pivot at $174.89 lies below the current price and has already been cleared. The classic R2 at $198.51 has also been surpassed intraday, with R3 at $253.94 the next reference on the classic pivot framework, per TradingView pivot data. A sustained daily close above the $214.71 intraday high would leave R3 as the next pivot in view.

On pullbacks, the classic pivot point at $143.08 marks initial structural support. Below that, the 100-day SMA near $131 represents the next meaningful moving-average shelf. A retest of S1 at $119.46 would only come into view if the 100-day SMA level were lost (TradingView, 29 April 2026).

This is technical analysis for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any instrument.

Arm Holdings share price history (2024–2026)

ARM listed on Nasdaq in September 2023 and closed April 2024 at $101.35, having pulled back sharply from a peak near $164 earlier that month amid a broad tech sell-off.

ARM’s stock price climbed through mid-2024, briefly touching $188.93 on 9 July 2024 as AI infrastructure enthusiasm lifted semiconductor valuations, before retreating to $96.87 on 5 August 2024 during a wider market rout tied to US recession fears and yen carry-trade unwinding. ARM recovered steadily through the autumn, ending 2024 at $123.80.

2025 opened with further momentum, reaching $182.95 on 22 January before sliding back towards the $100 area by early April 2025, when broader tariff-related market stress dragged the stock to a low of $79.04 on 7 April. A recovery followed through May and summer, with ARM trading in a roughly $130–$165 range through mid-year before easing back to close 2025 at $110.05.

2026 began quietly near $115, but the picture changed sharply in late March after ARM unveiled its AGI CPU at the 'Arm Everywhere' investor event. The stock surged from $135.95 on 30 March to a closing high of $235.85 on 24 April 2026, before retreating amid TSMC's full exit from its stake. ARM closed at $203.05 on 29 April 2026, approximately 84.5% up year on year and 84.5% above its 31 December 2025 close of $110.05.

Past performance is not a reliable indicator of future results. Share prices are indicative and may differ from live market prices.

Arm Holdings (ARM): Capital.com analyst view

ARM's price trajectory over the past two years shows how quickly market narratives can shift in the semiconductor space. The stock spent much of late 2024 and early 2025 consolidating in the $100–$165 range, weighed down by valuation concerns following its Nasdaq debut premium, before a sharp sell-off to around $79 in April 2025 amid broad tariff-related market stress. The subsequent recovery, which accelerated from late March 2026 after the company unveiled its AGI CPU and first-party silicon strategy, illustrates how quickly sentiment can reverse when a company reframes its revenue model. That said, the stock has also demonstrated that it can retrace gains quickly, as seen in the retreat from $235.85 to the current $203.95 following TSMC's full divestment of its ARM stake.

The near-term narrative centres on ARM's pivot towards merchant silicon and AI data centre royalties, which some analysts view as a meaningful expansion of the addressable market. However, the timeline for material revenue from these initiatives remains uncertain, and the stock's elevated valuation relative to near-term earnings leaves it sensitive to any guidance disappointment, including at the Q4 fiscal year 2026 results due on 6 May 2026. Macro conditions, including US trade policy and broader semiconductor demand trends, also cut both ways and could amplify moves in either direction.

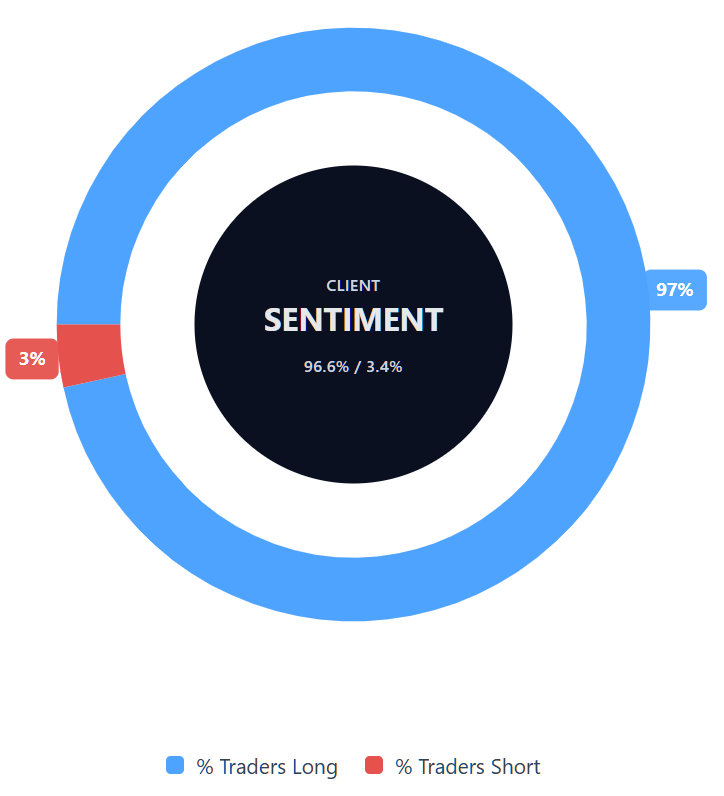

Capital.com’s client sentiment for Arm Holdings CFDs

As of 29 April 2026, Capital.com client positioning in Arm Holdings CFDs stands at 96.6% buyers vs 3.4% sellers, which puts buyers ahead by 93.2 percentage points and places sentiment firmly in heavy-buy, one-sided-long territory. This snapshot reflects open positions on Capital.com and can change rapidly as market conditions evolve.

Summary – Arm Holdings 2026

- ARM trades at $203.95 as of 1:53pm UTC on 29 April 2026, up approximately 84.5% year on year from $110.05 at the end of 2025.

- Key upside drivers include ARM's AGI CPU launch, AI data centre royalty potential, and a broad semiconductor re-rating; downside risks include elevated valuation and near-term earnings uncertainty.

- Q4 fiscal year 2026 earnings are due on 6 May 2026; ARM guided for revenue of approximately $1.18 billion at the midpoint, with adjusted EPS of $0.54–$0.62.

Past performance is not a reliable indicator of future results.

FAQ

Who owns the most Arm Holdings stock?

What is the five-year Arm Holdings share price forecast?

Is Arm Holdings a good stock to buy?

Could Arm Holdings stock go up or down?

Should I invest in Arm Holdings stock?

Can I trade Arm Holdings CFDs on Capital.com?

Yes, you can trade Arm Holdings CFDs on Capital.com. Trading share CFDs lets you speculate on price movements without owning the underlying asset and to take long or short positions. However, contracts for difference (CFDs) are traded on margin, and leverage amplifies both profits and losses. You should ensure you understand how CFD trading works, assess your risk tolerance, and recognise that losses can occur quickly.