Meta Platforms stock forecast: Q1 2026 earnings in focus

Meta Platforms is a US technology company preparing to report Q1 2026 results after announcing a 10% workforce reduction and reaffirming plans for heavy AI infrastructure spending. Explore third-party META price targets and technicals. Past performance is not a reliable indicator of future results.

Meta Platforms, Inc. (META) is trading at $671.73 in early European trading on 29 April 2026, within an intraday range of $667.49–$678.35 on Capital.com's feed as of 10:31am UTC. Past performance is not a reliable indicator of future results.

Price action is underpinned by several intersecting drivers. Meta confirmed on 23 April 2026 that it would reduce its global workforce by approximately 10%, equivalent to around 8,000 employees, with the first wave of cuts beginning on 20 May, alongside the cancellation of 6,000 open roles (CNBC, 23 April 2026). The company framed the move as part of a broader operational efficiency drive amid escalating AI investment (Reuters, 20 April 2026). Meta has also guided full-year 2026 capital expenditure of $115bn–$135bn tied to its AI and data-centre build-out, keeping investor focus on cost discipline ahead of the Q1 print (Reuters, 29 January 2026). Separately, Australia proposed a 2.25% revenue tax on Meta, Google and TikTok on 28 April 2026 if the platforms do not compensate news publishers, adding a regulatory dimension to the near-term outlook (Benzinga, 29 April 2026). Past performance is not a reliable indicator of future results.

Third-party Meta Platforms outlook: Q1 nears, targets diverge

As of 29 April 2026, third-party Meta Platforms stock forecasts for 2026–2030 reflect recalibrations ahead of the company's Q1 2026 earnings release, with most firms retaining constructive ratings while adjusting targets in response to macroeconomic conditions and AI capital expenditure expectations.

UBS (broker target)

UBS maintains a Buy rating on META with a 12-month price target of $908, raised from $872, as analyst Stephen Ju signals confidence in the company's AI monetisation runway ahead of the Q1 print. The target sits above the broader consensus average and reflects UBS's view that GenAI-driven ad revenue growth, including an anticipated 18% year-on-year rise in ad impressions, could drive asymmetrically positive earnings revisions across 2026 and 2027 (The Globe and Mail, 22 April 2026).

Citizens (broker target)

Citizens reiterates a Market Outperform rating on META with a $900 price target, with analyst Andrew Boone maintaining one of the higher targets among covering firms ahead of quarterly results. The rating reflects continued conviction in Instagram-driven engagement growth and the monetisation outlook for Meta's AI products (Insider Monkey, 23 April 2026).

Guggenheim (broker target)

Guggenheim reiterates a Buy rating on META with a price target of $850, as analyst Michael Morris maintains his stance despite near-term uncertainty around AI cost discipline. At the time of the note, the $850 target implied an upside of approximately 27% from the stock's prevailing close (GuruFocus, 23 April 2026).

B of A Securities (broker target)

B of A Securities maintains a Buy rating on META with a price target of $820, trimmed from $885 by analyst Justin Post, as the firm recalibrates its valuation assumption ahead of the earnings catalyst. The cut reflects multiple compression across big tech rather than a change in fundamental outlook, with BofA's channel checks indicating no material reduction in advertiser spending (Yahoo Finance, 20 April 2026).

MarketBeat (consensus snapshot)

MarketBeat aggregates ratings from 50 covering research firms and records a Moderate Buy consensus rating, with an average 12-month price target of $837.72, drawn from four strong buy, 38 buy and eight hold recommendations. The note identifies the 29 April earnings release as a near-term catalyst, where advertising growth commentary and AI expenditure guidance could drive material revisions to the consensus range (MarketBeat, 15 April 2026).

Predictions and third-party forecasts are inherently uncertain, as they cannot fully account for unexpected market developments. Past performance is not a reliable indicator of future results.

META stock price: Technical overview

The META stock price trades at $671.73 as of 10:31am UTC on 29 April 2026, holding above its key moving-average cluster, with the 20-, 50-, 100- and 200-day SMAs at approximately $639, $631, $645 and $680. Price is currently wedged between the 100-day SMA near $645 and the 200-day SMA near $680, with the latter acting as a nearby overhead reference. The 20-over-50 alignment remains intact within the SMA family, consistent with a near-term constructive posture according to TradingView data. The Hull moving average (9) at $672 sits just above the last price, while the Ichimoku base line trails well below, near $606.

Momentum is broadly positive but not stretched. The 14-day RSI reads 59.49, placing it in the upper-neutral range, per TradingView oscillator data. The ADX (14) at 23.52 sits just below the 25 threshold, suggesting that the trend lacks strong directional conviction at present.

On the topside, the classic R1 pivot at $656.51 has already been cleared, with R2 at $740.90 the next reference in view on a sustained daily close above current levels. To the downside, the classic pivot point at $588.39 represents initial support, with the 100-day SMA shelf near $645 marking the more immediate area of interest. A move back below that shelf could open a path towards S1 at $504, per TradingView pivot data (TradingView, 29 April 2026).

This is technical analysis for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any instrument.

Meta Platforms share price history (2024–2026)

META’s stock price traded around $428 in late April 2024, with the stock having pulled back from earlier highs as investors digested elevated AI capital spending commitments. From that base, the stock climbed steadily through mid-2024, reaching around $539 by early July before a sharp reversal dragged it to a low near $441 on 5 August 2024 – a move that coincided with a broader global equity sell-off triggered by an unwinding of yen carry trades and recession fears.

The recovery was swift. META reclaimed $500 by September 2024 and closed the year at $585.83 on 31 December 2024, representing a gain of roughly 37% from the April 2024 lows. Strong Q2 and Q3 2024 earnings, fuelled by AI-enhanced advertising revenue and daily active user growth, supported the move higher.

In 2025, the stock reopened with renewed momentum, touching $790 in mid-August 2025 – its peak for the period – before fading into year-end to close 2025 at $659.77. In 2026, the picture shifted again. A tariff-related tech sell-off in early April 2026 pushed META down to an intraday low of $564.84 on 7 April, before a sharp recovery lifted the stock back above $670. META trades at $671.73 as of 29 April 2026, up approximately 1.8% year to date but around 15% below its August 2025 high.

Past performance is not a reliable indicator of future results. Share prices are indicative and may differ from live market prices.

Meta Platforms Q1 2026 earnings

Meta Platforms is scheduled to report its Q1 2026 results after the US market close on 29 April 2026 (Meta Investor Relations, 13 April 2026), with analyst consensus pointing to revenue of approximately $55.36bn, implying year-on-year growth of nearly 31% (MarketBeat, 27 April 2026).

The main points of focus for the quarter include the pace of advertising revenue growth amid a macro environment shaped by US tariff uncertainty, the scale of capital expenditure relative to the $115bn–$135bn full-year guidance range, and any updated commentary on Meta's AI product roadmap, including Llama model deployments and Ray-Ban Meta smart glasses (247 Wall St, 28 April 2026). A stronger-than-expected revenue print could reinforce the recovery from early April 2026 lows, while any downward revision to guidance or margin compression from AI infrastructure costs could weigh on sentiment (Business Insider, 28 April 2026).

Meta's decision to cut approximately 10% of its workforce, announced on 23 April 2026, is also likely to feature in the earnings call, with management expected to address how the restructuring aligns with its longer-term AI investment thesis and free-cash-flow outlook (CNBC, 23 April 2026).

Meta Platforms (META): Capital.com analyst view

Meta Platforms' price action over the past two years reflects a stock navigating the tension between substantial AI investment and robust advertising revenue growth. Having climbed from around $428 in late April 2024 to a peak near $790 by mid-August 2025, META demonstrated strong momentum as quarterly earnings consistently exceeded expectations and AI-driven ad targeting showed measurable results. The sharp pullback to around $565 in early April 2026, coinciding with renewed US tariff escalation and broader tech sector de-risking, underlines that sentiment can reverse quickly even for fundamentally sound businesses. The subsequent recovery above $670 suggests that buyers re-engaged, though the stock remains well below its 2025 high.

The key debate heading into Q1 2026 results centres on whether Meta's $115bn–$135bn capital expenditure guidance for 2026 will weigh on near-term free cash flow or be viewed as the foundation for a durable competitive advantage in AI infrastructure. Bulls argue that AI-enhanced products – including Llama model integrations and smart glasses – can sustain advertising revenue growth above 25% year on year. Bears caution that ad spend is cyclically sensitive and that any macro deterioration, trade policy shock or regulatory development – such as Australia's proposed 2.25% digital revenue tax – could compress margins faster than the investment cycle can offset.

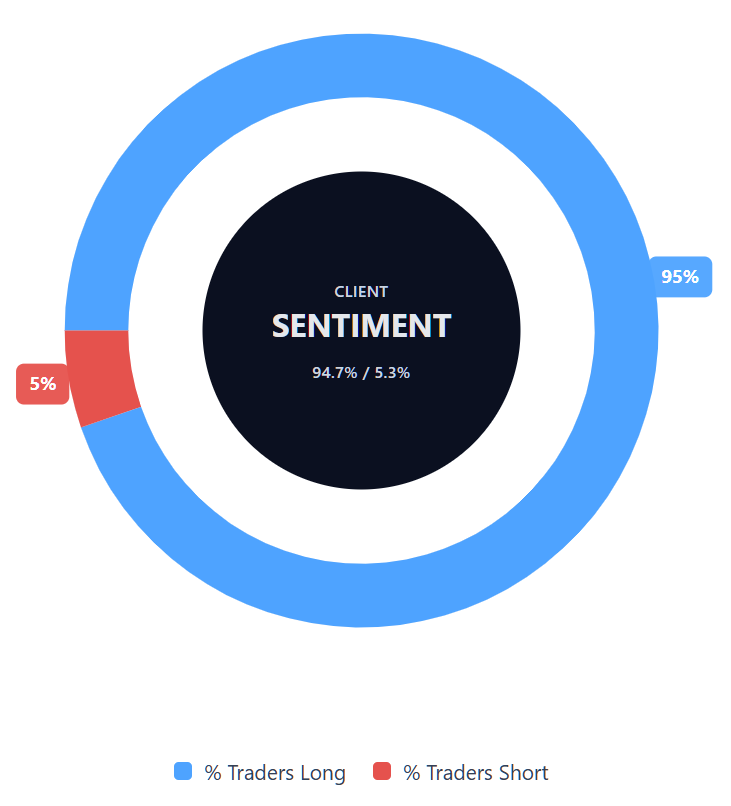

Capital.com’s client sentiment for Meta Platforms CFDs

As of 29 April 2026, Capital.com client positioning in Meta Platforms CFDs stands at 94.7% buyers and 5.3% sellers, putting buyers ahead by 89.4 percentage points and placing sentiment firmly in heavy-buy, one-sided-towards-longs territory. This snapshot reflects open positions on Capital.com and can change.

Summary – Meta Platforms 2026

- META trades at $671.73 as of 10:31am UTC on 29 April 2026, up sharply from April 2024 lows near $428 but around 15% below its August 2025 high of approximately $790.

- Key price drivers include Meta's $115bn–$135bn AI capital expenditure plan for 2026, its digital advertising revenue trajectory, and macroeconomic sensitivity to US trade policy and a broader tech sector risk environment.

- Meta confirmed a 10% workforce reduction of approximately 8,000 employees on 23 April 2026, with the first wave of cuts beginning on 20 May, and described the move as an operational efficiency measure alongside its AI investment push.

Past performance is not a reliable indicator of future results.

FAQ

Who owns the most Meta Platforms stock?

What is the five-year Meta Platforms share price forecast?

Is Meta Platforms a good stock to buy?

Could Meta Platforms stock go up or down?

Meta Platforms stock could move in either direction depending on earnings results, forward guidance, advertising trends, AI-related spending, regulation and broader market sentiment. In the near term, the market appears focused on whether large capital expenditure commitments will support longer-term growth or weigh on margins and free cash flow. Technical levels can also influence price action, but they do not guarantee outcomes. As with any share, volatility can increase around earnings releases and major policy or macroeconomic developments.

Should I invest in Meta Platforms stock?

Can I trade Meta Platforms CFDs on Capital.com?

Yes, you can trade Meta Platforms CFDs on Capital.com. Trading share CFDs lets you speculate on price movements without owning the underlying asset and to take long or short positions. However, contracts for difference (CFDs) are traded on margin, and leverage amplifies both profits and losses. You should ensure you understand how CFD trading works, assess your risk tolerance, and recognise that losses can occur quickly.