Amazon stock forecast: Q1 earnings and AI spending focus

Amazon heads into its Q1 2026 earnings release with investor focus on whether recent AI investment, including its $5bn Anthropic commitment, is supporting revenue growth across the business. Explore third-party AMZN price targets. Past performance is not a reliable indicator of future results.

Amazon.com, Inc. (AMZN) is trading at $259.80 as of 12:32pm UTC on 29 April 2026, within an intraday range of $256.95–$261.69. Past performance is not a reliable indicator of future results.

Sentiment around AMZN is being shaped by several converging factors ahead of the company's Q1 2026 earnings report, due after the close on 29 April (Amazon News, 15 April 2026). Investors are focused on whether Amazon's substantial AI infrastructure spending, including an additional $5 billion commitment to Anthropic announced on 19 April 2026, is translating into revenue growth (Amazon News, 20 April 2026). The earnings release coincides with the Federal Reserve's April 28–29 FOMC meeting decision, adding a macroeconomic overlay to an already event-heavy session (Federal Reserve, 7 April 2026). At the same time, the S&P 500 has been trading near record highs after 81.3% of reporting companies beat expectations this season (Reuters, 24 April 2026). AWS's recently disclosed partnership with OpenAI, aimed at expanding enterprise AI services, has also drawn attention to Amazon's competitive position in cloud computing amid ongoing US trade-policy uncertainty affecting third-party marketplace sellers (Fortune, 29 April 2026).

Third-party Amazon outlook: Q1 earnings, AI spend

As of 29 April 2026, third-party Amazon stock forecasts for 2026–2030 reflect a broadly positive outlook heading into the company's Q1 2026 earnings report, with most active broker calls carrying buy-equivalent ratings and targets ranging from $285 to $325. The following briefs summarise the most recent dated estimates from this period.

Truist Financial Securities (buy, target raise)

Truist Financial Securities analyst Youssef Squali raised his 12-month AMZN price target to $285 from $280, while maintaining a buy rating ahead of the company's 29 April earnings call. The revision reflects Squali's expectation that AWS revenue growth will accelerate to approximately 25% in Q1 2026, up from 23% in Q4 2025, driven by expanding AI partnerships with Anthropic and OpenAI (Watcher.Guru, 21 April 2026).

Arete Research (buy, target raise)

Arete Research raised its AMZN price target to $301 from $285, maintaining a buy rating. The firm cited improved long-term AWS demand visibility following Amazon's deeper commitment to Anthropic, while noting that near-term capital expenditure intensity and free cash flow timing remain key watchpoints if AI monetisation lags the investment cycle (MarketBeat, 23 April 2026).

Public.com (consensus snapshot)

Public.com aggregates 41 active analyst ratings on AMZN, producing a consensus price target of $287.24 and an overall buy rating. The breakdown shows 46% of contributing analysts at strong buy and 49% at buy, with 5% at hold and none at sell, reflecting broadly constructive sentiment across the sell side ahead of Q1 results (Public.com, 28 April 2026).

Mizuho (outperform, target raise)

Mizuho raised its AMZN price target to $325 from $315, maintaining an outperform rating, making it the highest active target among brokers in this period. The increase followed Amazon's previously reported Q4 2025 revenue beat of $213.39 billion, up 13.6% year on year, with Mizuho noting continued positive sentiment around AWS's AI infrastructure expansion and supply arrangements with major hyperscaler clients (MarketBeat, 28 April 2026).

Predictions and third-party forecasts are inherently uncertain, as they cannot fully account for unexpected market developments. Past performance is not a reliable indicator of future results.

Amazon Q1 2026 earnings

Amazon is scheduled to report its Q1 2026 financial results on 29 April 2026 after the US markets close, with a conference call set for 2:30pm PT / 5:30pm ET; the webcast is available via Amazon's investor relations page (Amazon News, 15 April 2026).

Analyst consensus heading into the release places Q1 2026 revenue at approximately $177.10 billion, representing roughly 14% year-on-year growth, with earnings per share estimated at $1.63, up from $1.59 in Q1 2025 (Investing.com, 29 April 2026). Advertising revenue consensus sits near $16.84 billion, approximately 21% above the year-ago period, while AWS segment revenue is expected at around $36.80 billion, with consensus operating margin at 35.7% within a range that analysts note has widened to 30.9%–40%, reflecting debate around AI and cloud demand (S&P Global, 23 April 2026).

The Q4 2025 results, reported on 4 February 2026, showed AWS growing 24% year on year to $35.60 billion – the fastest growth in 13 quarters at that time – and net income of $21.20 billion, or $1.95 per diluted share; CEO Andy Jassy also noted approximately $200 billion in planned capital expenditure across Amazon for full-year 2026 (Business Wire, 5 February 2026).

Past performance is not a reliable indicator of future results

AMZN stock price: Technical overview

The AMZN stock price is trading at $259.80 as of 12:32pm UTC on 29 April 2026, holding well above its key moving-average cluster – the 20-, 50-, 100- and 200-day SMAs sit at approximately $239, $221, $226 and $227 respectively – with a 20-over-50 alignment intact across both the simple and exponential families, which keeps the near-term trend structure constructive.

Momentum readings are stretched. The 14-day RSI stands at 73.73, a level that typically signals overbought conditions, while the average directional index (14) registers 34.10, consistent with an established directional trend rather than a ranging market (TradingView). The Hull moving average (9), at $263.69, sits above the last price and represents the nearest overhead reference within the moving-average set.

On the topside, the classic R1 pivot at $219.45 has already been cleared. The R2 level at $230.62 is also below the current price, leaving the R3 pivot at $251.95 as the next classic resistance reference. The classic pivot (P) at $209.29 marks initial support on a pullback, with the 100-day SMA near $225.77 forming a broader moving-average shelf below. The S1 level at $198.12 represents the next reference if that shelf comes under pressure (TradingView, 29 April 2026).

This technical analysis is for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any instrument.

Amazon share price history (2024–2026)

AMZN’s stock price opened April 2024 around $177 before rallying sharply through the early summer, touching an intraday high of $201.30 on 11 July 2024 as enthusiasm around AWS and AI spending strengthened. That advance reversed abruptly in early August, when a weak US jobs report and an unwinding of the yen carry trade sent global equities lower. AMZN hit an intraday low of $151.70 on 5 August 2024. The stock then recovered steadily through the rest of the year, closing 2024 at $219.85 as broader market sentiment improved alongside stronger big-tech earnings.

AMZN extended those gains into the new year, briefly pushing above $249 in January 2026 before Q4 2025 results triggered a reset in sentiment. Shares fell sharply from $233.80 on 4 February to close at $198.14 on 5 February 2026, as guidance and capital expenditure plans disappointed some investors. A second leg lower followed in early April 2026, when renewed US tariff escalation dragged the stock to an intraday low of $209.14 on 7 April, before a partial trade-policy reversal and improving sentiment lifted AMZN back towards the $260 area.

AMZN closed at $259.35 on 29 April 2026, approximately 14.4% higher year to date and approximately 46.2% above its level of $177.35 at the close of April 2024.

Past performance is not a reliable indicator of future results. Share prices are indicative and may differ from live market prices.

Amazon (AMZN): Capital.com analyst view

Amazon’s performance over the past two years reflects the company’s expanding footprint across cloud computing, advertising and AI infrastructure. AWS continues to post strong growth rates, while Amazon’s advertising segment has emerged as a high-margin contributor. Together, these factors have supported upward price momentum in AMZN shares. The stock’s recovery from the early April 2026 tariff-driven sell-off to near the $260 area ahead of Q1 2026 earnings also shows how quickly sentiment can shift when macroeconomic concerns ease. At the same time, that volatility illustrates how exposed the stock remains to trade-policy developments, given Amazon’s heavy reliance on third-party marketplace sellers sourcing goods from China.

On the risk side, Amazon’s commitment to approximately $200bn in capital expenditure for 2026 – focused on AI and cloud infrastructure – could weigh on near-term free cash flow if those investments take longer than expected to generate returns. At the same time, some analysts argue that this level of spending is consistent with Amazon’s efforts to capture long-term cloud and enterprise AI market share. Tariff uncertainty adds another layer of complexity: cost pressures on marketplace sellers could weigh on retail volumes, while Amazon’s logistics infrastructure and Prime ecosystem may offer some relative resilience compared with smaller e-commerce competitors.

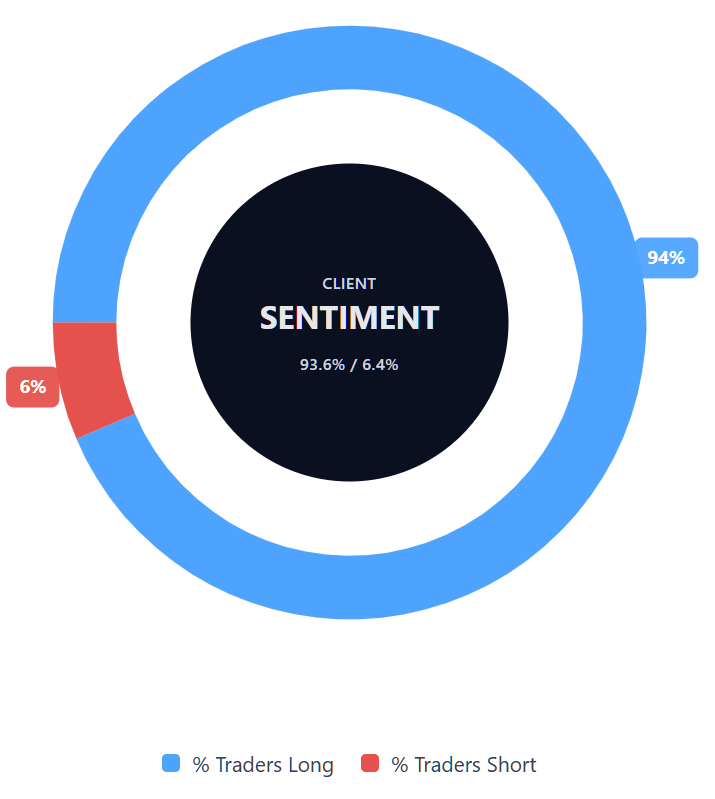

Capital.com’s client sentiment for Amazon CFDs

As of 29 April 2026, Capital.com client positioning in Amazon CFDs shows 93.6% of open positions are buyers versus 6.4% sellers, putting buyers ahead by 87.2 percentage points and placing sentiment firmly in one-sided territory. This snapshot reflects open positions on Capital.com at the time of writing and can change rapidly as market conditions evolve.

Summary – Amazon 2026

- AMZN is trading at $259.80 as of 12:32pm UTC on 29 April 2026, up approximately 46% from $177.35 in April 2024 and 14.4% year to date.

- Technical indicators on TradingView show the price holding above all major moving averages, with the 14-day RSI at 73.73, signalling stretched momentum and an established uptrend according to the ADX reading of 34.10.

- Key drivers include AWS growth, Amazon’s $200bn 2026 capital expenditure commitment to AI infrastructure, and ongoing US tariff uncertainty affecting third-party marketplace sellers.

- Amazon reports Q1 2026 earnings on 29 April after the US markets close. Analyst consensus points to revenue of about $177.10bn and EPS of $1.63, with AWS growth remaining the central focus.

Past performance is not a reliable indicator of future results.

FAQ

Who owns the most Amazon stock?

What is the five-year Amazon share price forecast?

Is Amazon a good stock to buy?

Could Amazon stock go up or down?

Should I invest in Amazon stock?

Can I trade Amazon CFDs on Capital.com?

Yes, you can trade Amazon CFDs on Capital.com. Trading share CFDs lets you speculate on price movements without owning the underlying asset and to take long or short positions. However, contracts for difference (CFDs) are traded on margin, and leverage amplifies both profits and losses. You should ensure you understand how CFD trading works, assess your risk tolerance, and recognise that losses can occur quickly.