Apple stock forecast: Q2 2026 earnings in focus

Apple approaches its Q2 2026 results with consensus revenue expectations of $109.30–$109.50 billion, while tariff costs and emerging handset chip competition remain in focus. Explore third-party AAPL price targets and technicals. Past performance is not a reliable indicator of future results.

Apple Inc (AAPL) is trading at $269.05 in early European trading as of 11:49am UTC on 29 April 2026, within an intraday range of $267.37–$271.08. Past performance is not a reliable indicator of future results.

Shares are tracking pre-earnings positioning ahead of Apple's fiscal Q2 2026 results, scheduled for 30 April 2026, with consensus revenue expectations of around $109.30–$109.50 billion for the quarter (9to5Mac, 2 April 2026). Tariff exposure remains a key overhang, as Apple has absorbed an estimated $3.30 billion in cumulative tariff costs since April 2025, with the quarterly run rate reportedly rising from $800 million to $1.40 billion following a February 2026 Supreme Court ruling that replaced variable tariff rates with a flat 10% blanket levy under Section 122 (TECHi, 7 April 2026). Separately, reports that OpenAI is developing smartphone processors in collaboration with Qualcomm weighed on AAPL shares in the prior session, as they raised the prospect of increased competition in the handset chip market (S&P Global, 23 April 2026).

Third-party Apple outlook: Q2 earnings near, targets diverge

As of 29 April 2026, third-party Apple stock forecasts for 2026–2030 reflect a range of views shaped by the upcoming fiscal Q2 2026 earnings report on 30 April 2026, tariff exposure, and AI product momentum.

BNP Paribas (upgrade and target revision)

BNP Paribas upgrades Apple to Outperform from Neutral and raises its price target to $300 from $260. The bank cites improving iPhone demand dynamics and a more constructive view on Apple's AI-linked Services revenue trajectory as the basis for the rating change (MacDailyNews, 17 April 2026).

Bank of America (pre-earnings target lift)

Bank of America analyst Wamsi Mohan reiterates a Buy rating and raises his 12-month price target to $325 from $320. The revision reflects expected strength in iPhone and Services revenues into Q2 FY2026, with the firm's revenue estimate of $109.50 billion broadly aligned with Wall Street consensus (Yahoo Finance, 16 April 2026).

UBS (neutral-rated target adjustment)

UBS raises its 12-month price target on Apple to $287 from $280, while maintaining a Neutral rating. The bank flags continued resilience in personal device demand as a positive, with a persistent memory supply shortage remaining an ongoing constraint on near-term margin visibility (CNBC, 28 April 2026).

Wedbush (Outperform reaffirmation)

Wedbush maintains its Outperform rating and retains its street-high $350 price target following Apple's leadership transition announcement. Analyst Daniel Ives reaffirms the view that Apple's AI integration roadmap and services monetisation potential remain intact despite the CEO change, while flagging tariff costs and macro uncertainty as near-term risks (Investing.com, 20 April 2026).

MarketBeat (consensus overview)

MarketBeat aggregates Wall Street ratings into a Moderate Buy consensus with an average 12-month price target of $301.37. The distribution spans 1 strong buy, 22 buys, 12 holds, and 1 sell across active coverage, with individual targets ranging from $220 to $350 amid differing views on tariff pass-through and AI monetisation timing (MarketBeat, 15 April 2026).

Predictions and third-party forecasts are inherently uncertain, as they cannot fully account for unexpected market developments. Past performance is not a reliable indicator of future results.

AAPL stock price: Technical overview

The AAPL stock price is trading at $269.05 as of 11:49am UTC on 29 April 2026, holding above its key moving-average shelf of approximately $254–$264, with the 20/50/100/200-day SMAs sitting at about $264 / $261 / $264 / $254. A 20-over-50 alignment remains intact across the SMA family, which supports a stable near-term bias. The Hull moving average (9) at $270.62 sits marginally above the last price, suggesting near-term momentum is roughly in equilibrium at current levels.

Momentum indicators are broadly-neutral to firm. The 14-day relative strength index reads 58.26, consistent with upper-neutral territory, while the average directional index at 13.02 sits below the 15 threshold, indicating a weak trend structure rather than a directionally strong move.

On the topside, the classic R1 pivot at $265.04 is now below the current price, with R2 at $276.30 the next reference point if the stock records a sustained daily close above the $270 area. On pullbacks, the classic pivot (P) at $255.28 represents initial support, followed by the 200-day SMA near $254. The S1 level at $244.02 would become relevant on a deeper retreat below that SMA shelf (TradingView, 29 April 2026).

This is technical analysis for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any instrument.

Apple Q2 2026 earnings preview

Apple is scheduled to report fiscal second-quarter 2026 results on 30 April 2026 after market close, with a conference call beginning at 5.00pm ET; the results will be the first under the company's incoming CEO following the leadership transition announced in April 2026 (Apple IR, 30 April 2026).

Wall Street consensus, aggregated across 31–32 analysts by Yahoo Finance, puts Q2 2026 revenue at approximately $109.69 billion, representing roughly 14.8% year-on-year growth from $95.40 billion in Q2 2025, with a diluted earnings per share estimate of $1.95, ranging from a low of $1.56 to a high of $2.16. JP Morgan sits above consensus, projecting revenue of $112.70 billion and EPS of $2.05, citing stronger-than-expected product revenues of $82.30 billion driven in part by iPhone 17 demand; Goldman Sachs forecasts EPS of $2.00, expecting 14% year-on-year Services growth and a modest tailwind from favourable exchange rates (AppleInsider, 26 April 2026). S&P Global Market Intelligence notes that the consensus gross margin expectation sits near 48.4%, with memory cost pressures flagged as the primary downside risk to that figure (S&P Global, 23 April 2026).

Apple has exceeded Wall Street EPS estimates in each of its last four quarters, most recently reporting Q1 2026 revenue of $143.80 billion and adjusted EPS of $2.84, both above prior consensus (Barchart, 20 April 2026).

Past performance is not a reliable indicator of future results.

Apple share price history (2024–2026)

AAPL’s stock price closed at around $170 in late April 2024, near a multi-month low, amid broader concerns about iPhone demand in China and a wider tech sector rotation. The stock recovered through the summer, reaching the $230–$235 range by September 2024, before pushing towards $260 in December 2024 on optimism around Apple’s AI integration roadmap under the Apple Intelligence branding.

In 2025, the stock saw sharper swings. AAPL climbed to a peak of around $280 in early February 2025, then unwound through the spring as the Trump administration announced sweeping new tariffs in April. The stock fell sharply to a low of around $168 on 9 April 2025, its lowest point across the two-year window, as investors weighed the impact of levies on Apple’s China-based manufacturing supply chain. A partial tariff pause and an improved macro tone helped the stock recover, and by August 2025 it had climbed back towards $230, extending further into the $250–$260 range through the autumn.

AAPL entered 2026 around $271, dipped to the $245–$250 range through February and March amid renewed tariff uncertainty and a CEO transition announcement, then moved back above $268 heading into the 29 April 2026 session. That left the stock up approximately 58% from the April 2025 trough and roughly in line with levels seen at the end of 2024.

Past performance is not a reliable indicator of future results. Share prices are indicative and may differ from live market prices.

Apple (AAPL): Capital.com analyst view

Apple’s price action over the past two years reflects both the stock’s resilience and its sensitivity to macro and policy shifts. The recovery from the April 2025 tariff-driven lows near $168 to current levels around $269.05 represents a meaningful rebound, supported by improving iPhone demand expectations, Services revenue growth, and renewed investor interest in AI integration across Apple’s product line. That said, the tariff overhang has not fully dissipated. Ongoing US–China trade friction continues to weigh on supply-chain cost visibility, and Apple’s manufacturing concentration in China remains a structural risk that could reassert itself if trade conditions deteriorate further.

In the near term, the Q2 FY2026 earnings release on 30 April 2026 presents a potential catalyst in either direction. A beat on revenue and earnings per share, alongside a constructive management tone on tariff mitigation and Services margin, could reinforce the recent move back above the $265–$270 area. Conversely, softer-than-expected guidance, particularly around the tariff cost trajectory or China iPhone sales, could weigh on sentiment and test the support cluster below $260. The recently announced CEO transition also adds a layer of uncertainty around strategic continuity that the market is still pricing in.

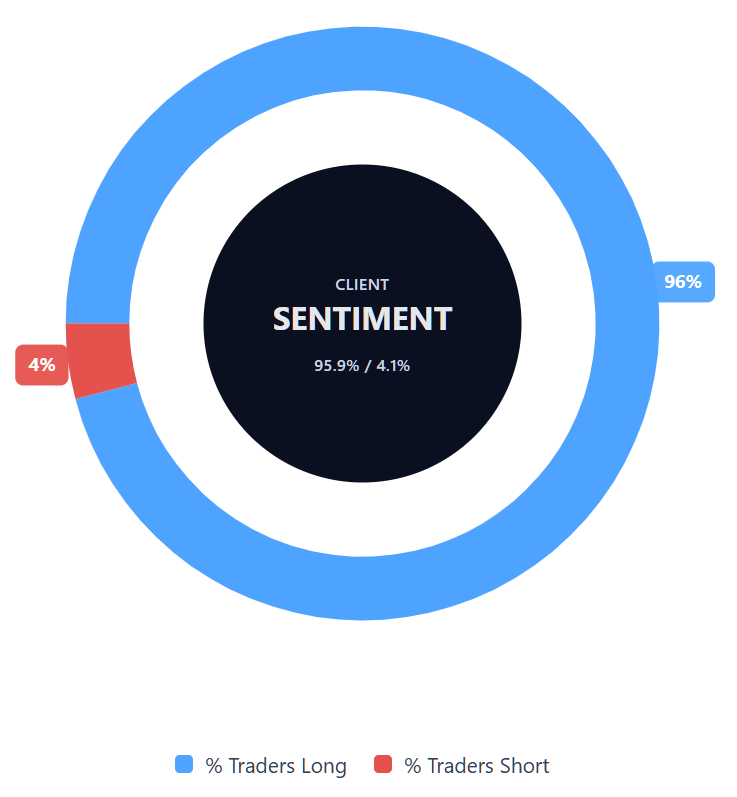

Capital.com’s client sentiment for Apple CFDs

As of 29 April 2026, Capital.com client positioning in Apple CFDs stands at 95.9% buyers and 4.1% sellers, putting buyers ahead by 91.8 percentage points. This places positioning firmly in heavily long-biased territory. This snapshot reflects open positions on Capital.com and can change.

Summary – Apple 2026

- AAPL is trading at $269.05 as of 11:49am UTC on 29 April 2026, recovering sharply from an April 2025 tariff-driven low near $168.

- Key drivers include ongoing US–China tariff exposure, Apple’s CEO transition, Services and AI monetisation momentum, and pre-earnings positioning ahead of the 30 April 2026 Q2 FY2026 results.

- Technical indicators on TradingView show the price holding above the 20/50/100/200-day SMA cluster ($254–$264), with the 14-day RSI at 58.26 in upper-neutral territory and the ADX at 13.02 signalling a weak trend structure.

Past performance is not a reliable indicator of future results.

FAQ

Who owns the most Apple stock?

What is the five-year Apple share price forecast?

Is Apple a good stock to buy?

Could Apple stock go up or down?

Should I invest in Apple stock?

Can I trade Apple CFDs on Capital.com?

Yes, you can trade Apple CFDs on Capital.com. Trading share CFDs lets you speculate on price movements without owning the underlying asset and to take long or short positions. However, contracts for difference (CFDs) are traded on margin, and leverage amplifies both profits and losses. You should ensure you understand how CFD trading works, assess your risk tolerance, and recognise that losses can occur quickly.