Trump’s “Big, Beautiful Bill”: What it means for markets

Trump's signature spending legislation could have a major impact on financial markets

Donald Trump has begun laying the groundwork for a sweeping fiscal and economic policy agenda that he and his allies have dubbed the “Big, Beautiful Bill.” The legislation, after passing the Senate despite objections from several Republican holdouts, has now returned to the House of Representatives for a final vote. While not yet enacted, its broad contours have already been laid bare by the Trump campaign: a mix of tax cuts, broad-based tariffs, major infrastructure investment, and regulatory rollbacks.

What is in the “Big, Beautiful Bill”?

The proposed bill includes an extension and expansion of the 2017 Tax Cuts and Jobs Act, with continued relief for both corporations and individuals, and a potential reduction in capital gains tax rates. In addition, Trump is advocating for a new wave of protectionist trade measures, most notably a 10 percent universal tariff on all imports and sharply higher duties on goods from China, potentially as high as 60 percent.

-

Permanent Tax Cuts for Individuals and Businesses – Makes 2017 tax cuts permanent, with individual rates capped at 37%, higher standard deduction, and expanded child tax credit. Tips and overtime income become tax-free up to $25,000 and $12,500 respectively.

-

Enhanced Corporate Incentives – Keeps the 21% corporate tax rate, boosts pass-through deductions to 23%, and restores 100% expensing for capital investment in the U.S.

-

Strategic Subsidies and Tax Breaks – Provides targeted incentives for firms operating in “America First Economic Zones” and investing in key technologies.

-

Regulatory and Energy Rollbacks – Cuts environmental and labor regulations, fast-tracks fossil fuel projects, and suspends key Biden-era climate policies.

-

Increasing the debt ceiling - Increases the debt ceiling by as much as $5 Trillion.

Fiscal Consequences: A Heavier Debt Burden

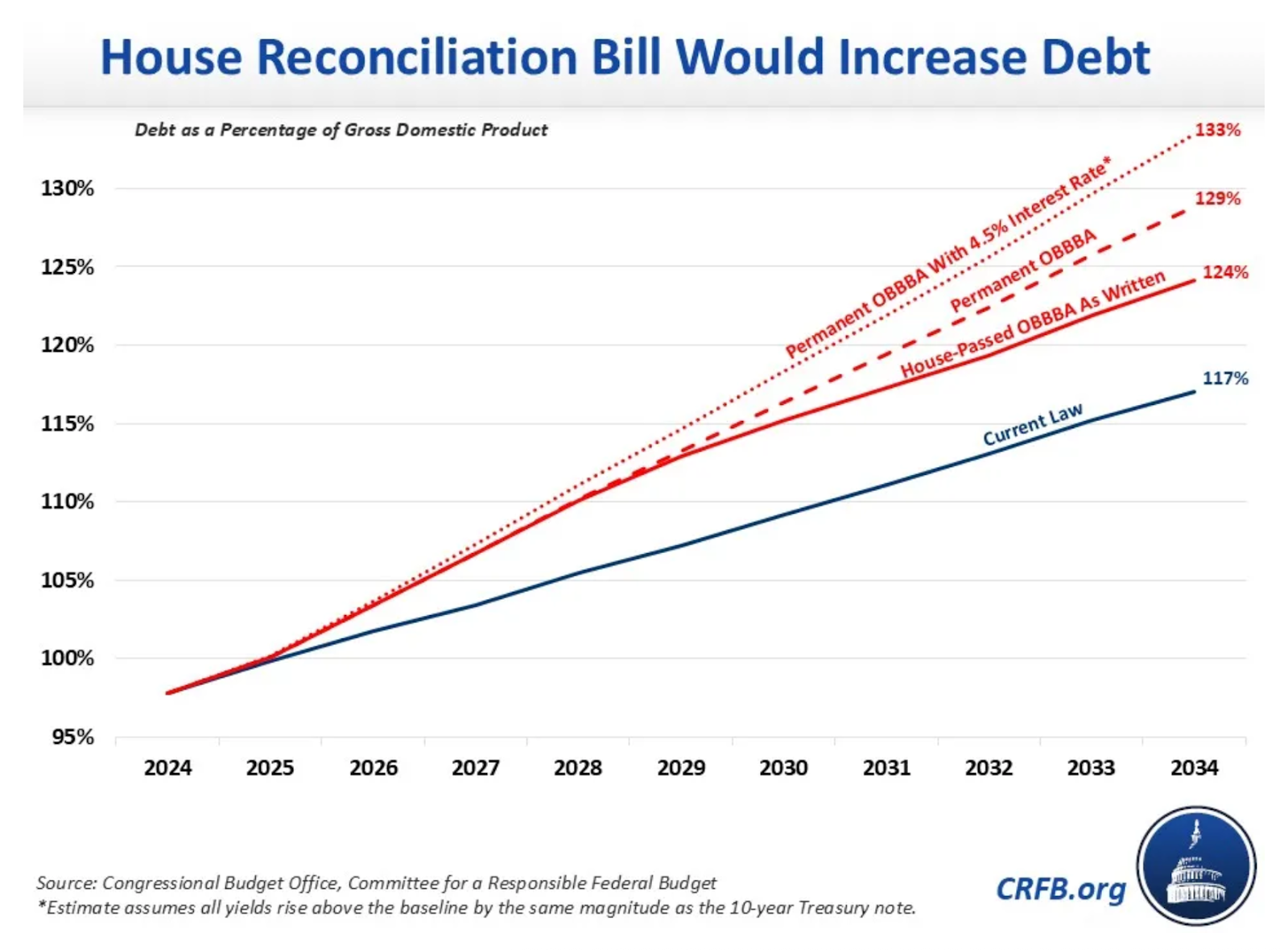

According to analysis by the Committee for a Responsible Federal Budget (CRFB), the policies proposed under Trump’s agenda could add between $5 trillion and $7 trillion to the national debt over the next decade. The bulk of this increase would come from the extension of the 2017 tax cuts, which alone could cost more than $3 trillion. While new tariffs may provide some revenue, they are unlikely to offset the revenue loss from tax reductions and may also dampen growth. With trade negotiations ongoing, the rate of tariffs and the subsequent revenue it would generate to cover spending commitments is unclear.

Spending increases, particularly in infrastructure and defence, would further strain public finances. The US debt-to-GDP ratio, already exceeding 120 percent, would climb significantly higher under this plan, particularly as rising interest costs compound the burden. The CRFB has warned that the bill risks entrenching unsustainable fiscal dynamics at a time when the US is already on an increasingly precarious budgetary path.

(Source: Committee for a Responsible Federal Budget)

Demand Surge Meets Supply Constraints

If implemented, the bill would deliver a sizable positive shock to aggregate demand. Tax cuts and public investment would increase disposable income and business activity, while protectionist trade policies would redirect consumer spending toward domestic goods and services. On the surface, this might appear stimulatory and supportive of growth.

However, these policies come at a time when the US economy is already operating near full capacity, with inflation still above the Federal Reserve’s 2 percent target and labour markets relatively tight and nominally at or above the Fed’s estimate for full employment. Injecting additional demand into an already overheated economy risks reigniting inflationary pressures. Complicating matters further is the supply-side impact of tariffs, which would raise input costs, disrupt supply chains, and reduce overall economic efficiency. This combination of a positive demand shock and a negative supply shock creates fertile ground for stagflation, with higher prices and weaker real growth outcomes.

Higher Yields, Rising Risk-Free Rates

One of the most immediate market implications of the “Big, Beautiful Bill” is likely to be upward pressure on US interest rates. Inflation expectations could become more entrenched at higher levels if the fiscal outlook deteriorates and the Federal Reserve is perceived as constrained in its policy response. At the same time, the Treasury would be forced to ramp up bond issuance to fund growing deficits, increasing the supply of government debt just as demand—particularly from foreign investors—could wane.

The result would likely be higher nominal and real yields across the curve, particularly at the long end. Ten-year Treasury yields could move well above 5 percent under such a scenario, repricing the cost of capital globally and exerting a powerful influence on all asset classes. In saying this, partly due to the drag on growth from the Trump administration’s policy volatility, the 10 year yield has been more volatile but well anchored around pre-election levels.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

Equity Valuations and the US Dollar

The impact on equities would be complex and time-dependent. In the short term, stimulus measures could support earnings growth in cyclical sectors tied to infrastructure, energy, and defence. However, higher real yields would exert downward pressure on equity valuations, particularly for growth and technology stocks, where future cash flows are more sensitive to discount rates. As a result, the broader market may face valuation headwinds through multiple compression, even if nominal earnings remain solid.

The outlook for the US dollar is similarly nuanced. In the initial phase, higher yields and safe-haven flows driven by geopolitical tensions or policy uncertainty could push the dollar higher. However, over the longer term, the twin deficits—fiscal and current account—would likely widen substantially, weighing on the dollar’s valuation. Concerns over US fiscal sustainability, coupled with deglobalisation and the potential acceleration of de-dollarisation efforts by rival economies, could ultimately weaken the dollar’s position in the global financial system.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)