The Jackson Hole Symposium: Will the Fed pivot or stick to its guns?

The Fed must balance a softening labour market with inflationary risks

The annual Jackson Hole symposium arrives this week at a critical juncture for global markets. With equity indices hovering near record highs, the US dollar softening, and investors positioning for Federal Reserve rate cuts, attention will be firmly fixed on Fed Chair Jerome Powell’s speech.

Wall Street rises heading into Jackson Hole as Fed rate cut bets grow

US equities have extended their upward run despite mixed economic signals. Robust corporate earnings have supported sentiment, even as recent data hinted at a softer labour market. The S&P 500 and Nasdaq 100 have pushed to fresh highs, while a rotation into smaller-cap and cyclical stocks suggests breadth is improving – a hallmark of healthier bull markets.

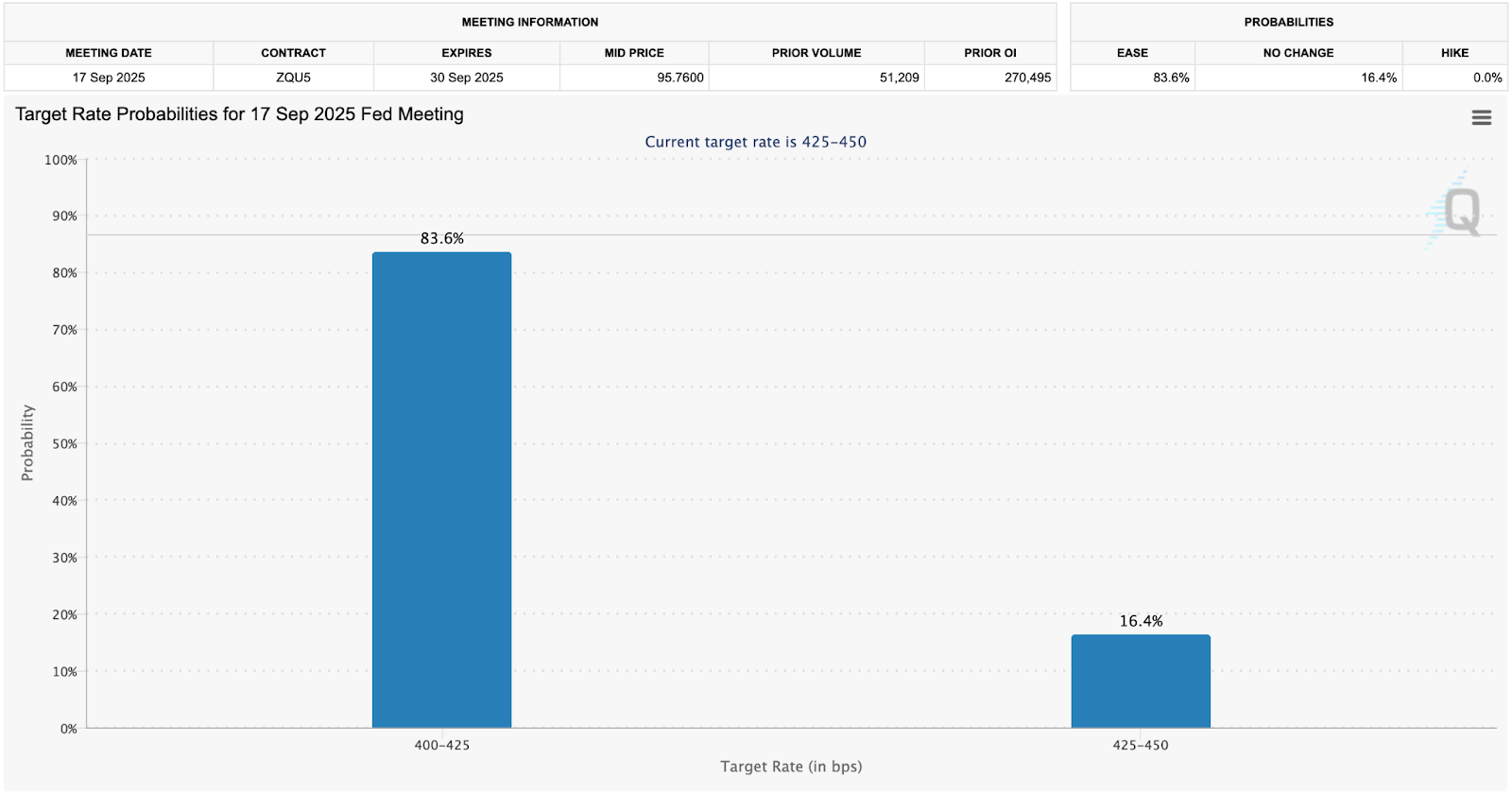

Driving much of this optimism is the expectation that the Fed will soon begin easing policy. After a period of speculation about the scale of cuts – including fleeting bets on a 50 basis-point move – markets are now pricing an almost 85% chance of a 25 basis-point cut in September. Traders see further cuts possible into the end of the year, as policymakers attempt to calibrate policy closer to neutral territory.

(Source: CME Group)

The question, however, is whether the Fed sees recent data as weak enough to justify such a dovish tilt, or whether sticky inflation pressures – partly fuelled by tariffs – will keep policymakers cautious.

The markets look for how the Fed balances employment and inflation risks

The backdrop to Jackson Hole is far from straightforward. Producer price data last week surprised to the upside, highlighting the persistence of cost pressures. Tariff effects on consumer prices remain an open question, raising the risk that inflation proves stickier than policymakers would like.

That tension – between a labour market showing signs of fragility and an inflation outlook complicated by tariffs – lies at the heart of the Fed’s dilemma. Powell’s speech will offer crucial insight into how the central bank weighs these risks, and whether the balance of its reaction function is shifting.

History shows markets don’t just respond to the direction of policy, but also to the messaging around it. Cuts can be bullish for equities when seen as insurance against downside risks, but bearish if interpreted as a response to looming economic weakness.

That makes Powell’s Jackson Hole remarks critical. If he maintains the Fed’s recent “wait-and-see” framing – prioritising vigilance on inflation while downplaying labour market risks – markets may interpret it as a sign the central bank remains behind the curve. Such an outcome could be a risk-off moment.

On the other hand, a subtle pivot toward acknowledging the downside risks to growth, and emphasising the Fed’s role in protecting the labour market, could validate market optimism. This would echo last year’s dynamic, when the Fed’s acknowledgement of softer conditions underpinned a renewed rally in risk assets.

S&P 500 remains in an uptrend by is at risk of a hawkish surprise

The S&P 500 remains in an uptrend, marked by a series of higher-highs and higher-lows, and within a clear trend channel. The recent push to fresh record highs is also a bullish signal. However, upside momentum is slowing down, with a bearish divergence emerging on the daily RSI, implying possible exhaustion in the short-term. Combined with lofty valuations and a market heavily weighted towards equities, a hawkish surprise at Jackson Hole could spark a reversal in US stocks. Upward sloping support looms as the critical level for the S&P500; a break below previous resistance at the index’s former all-time highs may also signal a looming pullback. Meanwhile, a dovish surprise may give the market a boost, with a push to new record highs marking a possible further trend continuation.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)