Netflix tipped to post solid growth but outlook in focus amid Warner acquisition

Investors expect solid fourth quarter earnings but the focus remains on future sales and the Warner acquisition.

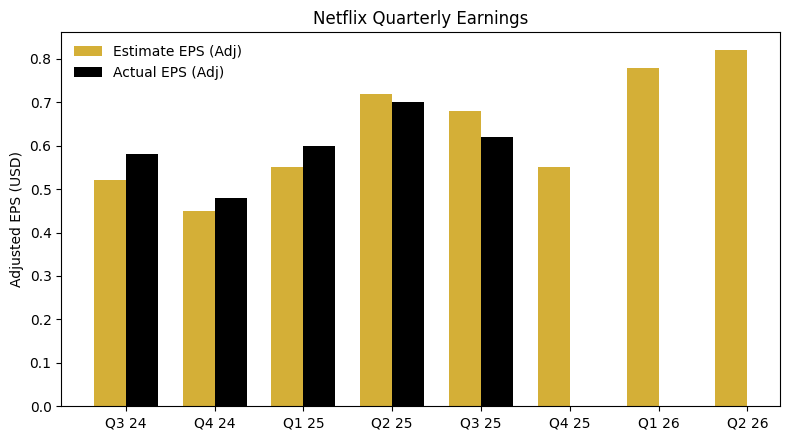

Netflix posts its 4Q earnings on January 20th, 2026 with analysts forecasting solid quarterly results.

Earnings tipped to rise on stable of original and live content

The markets are expecting a strong end to 2025 by Netflix. Earnings are projected to rise 28% from a year earlier to $0.55 per share, supported by revenue growth of around 16%. The robust topline was underpinned by a blockbuster line-up of content during the quarter. The highlights included the finale of marquee program Stranger Things and live events like the Anthony Joshua vs. Jake Paul fight and the NFL on Christmas Day.

(Source: Bloomberg, Capital.com)

Netflix’s outlook in focus amid sales headwinds and M&A activity

Investors will be homing in on the outlook for future earnings growth amid both topline and bottomline pressures ahead. Organic growth appears to be slowing down. Although Netflix no longer publishes subscriber numbers, user engagement growth appears to be on the wane, implying a slower rate of growth for the company going forward. Meanwhile, Netflix also confronts cost and cash flow uncertainty due to the planned acquisition of competitor Warner. The deal confronts regulatory uncertainty because of antitrust fears. It’s exposed to a possible bidding war for Warner with Paramount Skydance that could drag out the acquisition, blow out the costs and increase the value of the takeover.

The markets will also be hypervigilant of any unexpected shocks from Netflix after last quarter’s results. Netflix shares plunged by more than 10% off the back of Q3 earnings after an unexpected hit to profits due to an ongoing tax dispute in Brazil.

Netflix shares trend lower heading into quarterly earnings

Netflix shares are trending lower in the short-term albeit in a long term trend that is skewed to the upside. Momentum continues to point lower as the weekly RSI flirts with oversold territory. A significant support level looks to be around $US82 per share, which if broken brings into view the stock’s long-term upward trendline. Options markets currently imply an approximately 7% one day move, suggesting an implied range of $US82 to $US94.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)