Markets price in a flurry of trade deals heading into the July 9 US trade deadline

Will July 9 be an end to trade uncertainty or Liberation Day 2.0?

The next phase of US trade policy under the Trump administration will crystallise on July 9, the final day for countries to secure trade deals before facing steep new tariffs. The deadline follows the administration’s controversial “Liberation Day” tariffs announced in April, which triggered turmoil in global markets and ushered in a 90-day window for trading partners to negotiate agreements or face the higher tariffs.

Markets have since rebounded on the belief that further trade deals will be struck and tariff rates will come in lower than initially feared. However, the risk remains that the Trump administration fails to finalise key agreements, leaving the global economy exposed to another round of volatility.

The July 9 deadline: Will it be Liberation Day 2.0?

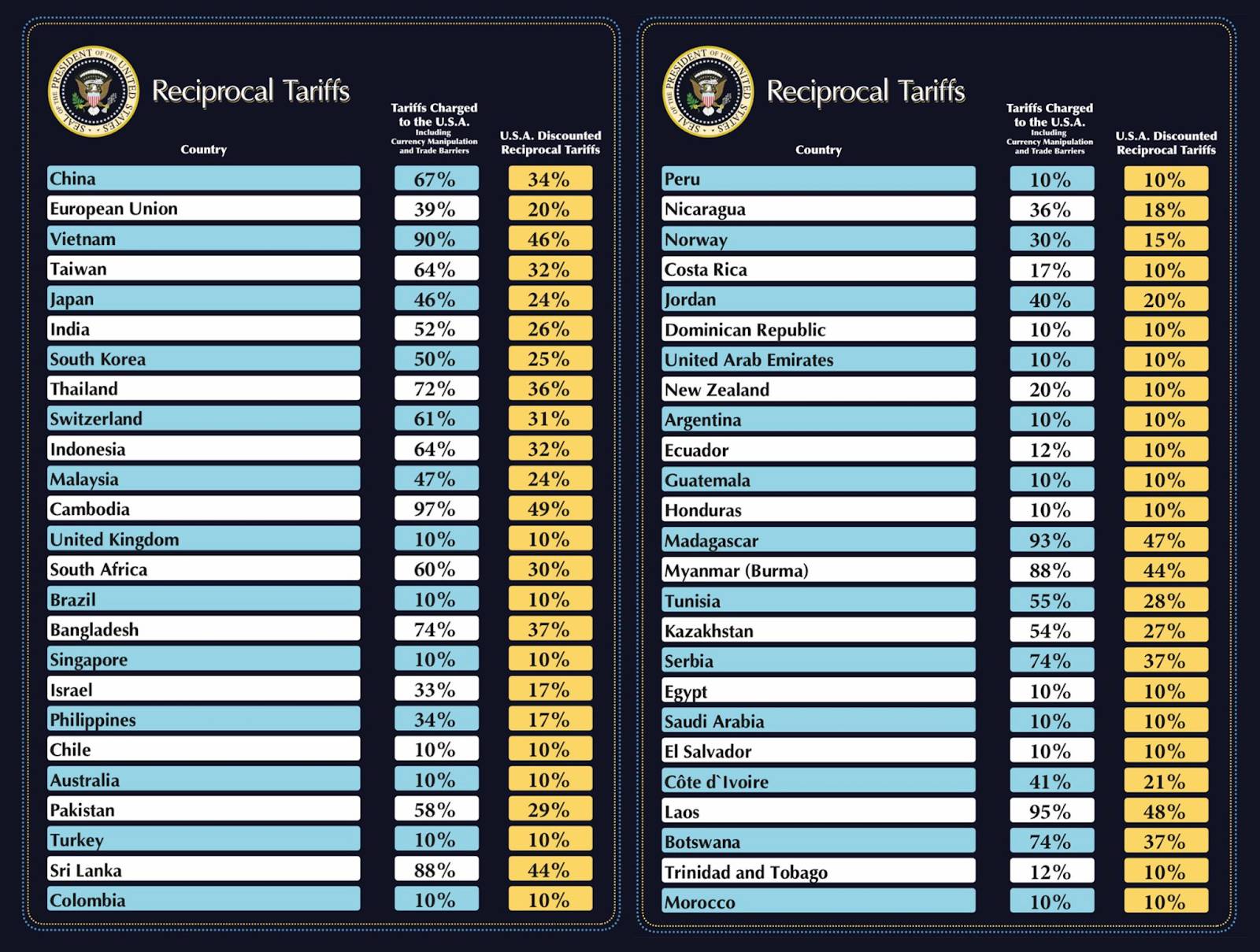

The July 9 deadline stems from the “Liberation Day” tariffs unveiled on April 2, 2025. Under the new policy, the US imposed a baseline 10% tariff on nearly all imports, with far steeper rates—some above 30%—threatened for major trading partners. The move was framed by the Trump administration as an effort to rebalance trade relationships and punish nations deemed to be exploiting the US market. While the administration had suggested tariffs were to be targeted and reciprocal, it instead used a contentious formula that sought to set tariffs at a rate that would neutralise any trade deficit with a trading partner. It also set a default 10% rate for countries with which the US boasts a trade surplus.

(Source: The White House)

Markets were rattled. The announcement triggered one of the worst single-day selloffs in years, with the S&P 500 falling nearly 5% and volatility surging across asset classes. Bond yields spiked as traders braced for higher inflation and an uncertain macro backdrop; technical factors, including arguably the unwinding of a popular hedge fund strategy, the so-called “basis trade”, compounded the stress in funding markets. The US Dollar fell on the shift in expected capital flows from changing trade relations and a crisis of confidence in US assets. The severity of the market reaction prompted the administration to backtrack somewhat, opening the door to negotiations.

The result was a 90-day window—set to expire on July 9—during which the US aimed to strike new trade deals or issue formal letters to individual countries outlining the specific tariff rates they would face.

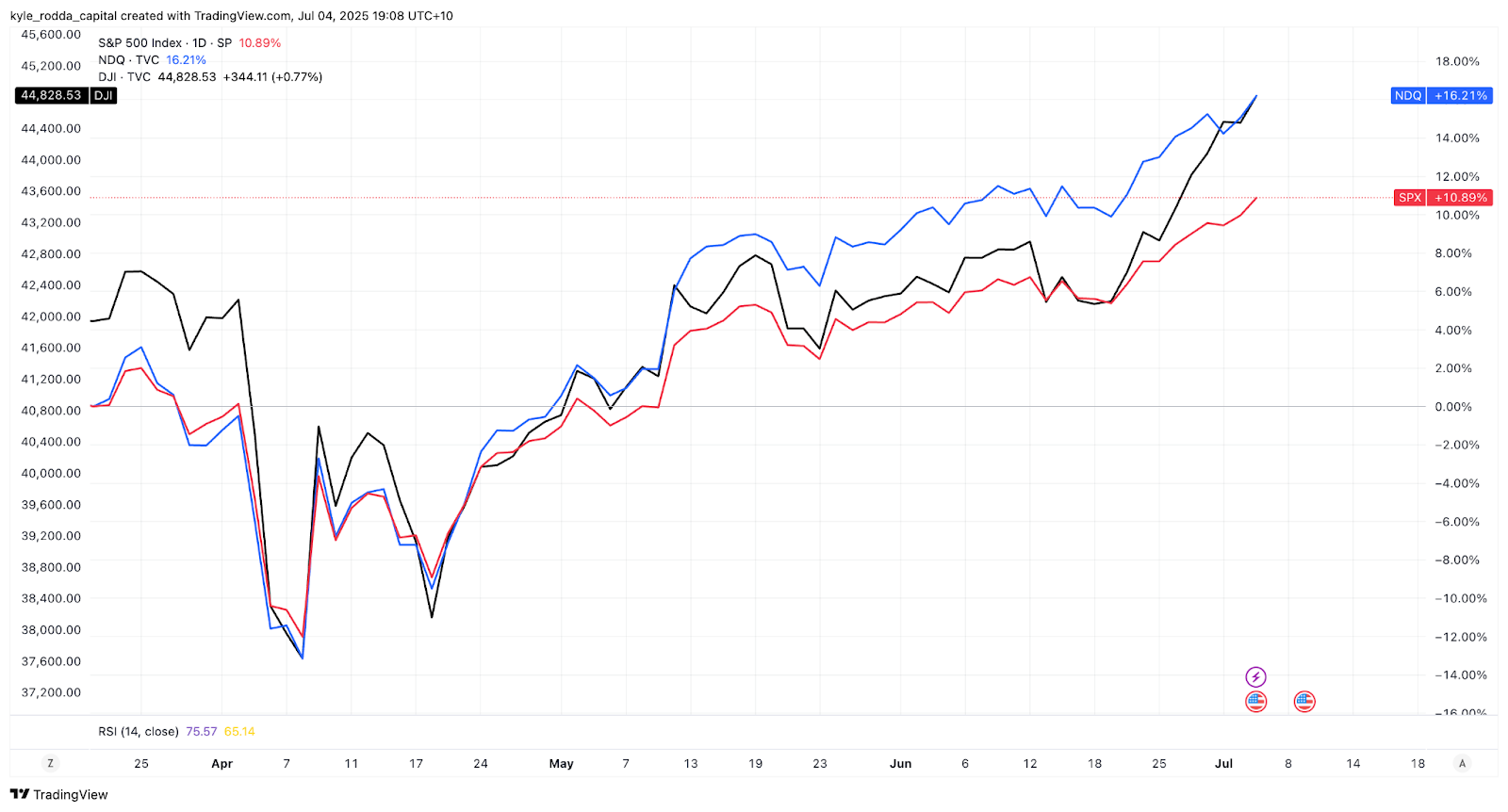

Wall Street climbs to record highs as tariff fears eased

Following the initial shock, financial markets found their footing as the US signalled a willingness to moderate its stance. The administration's walk-back from the highest proposed tariff rates, along with signs of progress in bilateral negotiations, helped restore investor confidence. Strong corporate earnings, especially from US tech stocks exposed to the artificial intelligence complex, along with data that showed resilient economic activity in the US despite tariffs and trade uncertainty, also buoyed sentiment.

US equities have since recovered to all-time highs, with the S&P 500 and Nasdaq both hitting fresh records in late June. The bond market has stabilised, and inflation expectations have remained stable. The prevailing assumption is that the average tariff rate will settle in the low teens—significantly below the worst-case scenarios priced in back in April.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

That optimism is grounded in real diplomatic progress. Trade deals have already been struck with Vietnam, the UK, and China—each providing a blueprint for how the administration might avoid applying maximum tariffs. Yet several major economies, including Japan, South Korea, and the European Union, remain without agreements, leaving room for policy missteps.

Progress made with key partners, but gaps remain

The most notable deal to date is with Vietnam, agreed on July 2. Under the framework, Vietnam will face a 20% tariff on most exports to the US and a 40% levy on transshipped goods that originate in China. In return, the US will provide duty-free access on select imports, while working with Vietnam to curb illicit trade flows. The deal is seen as a model for managing trade with export-heavy Asian economies.

A bilateral agreement with the UK was finalised in early June, securing tariff reductions and averting a cliff-edge scenario. China also reached a temporary agreement to reduce tariffs to 10% in exchange for a 30% US tariff rate on certain goods, buying both sides more time for a longer-term resolution. A framework for rare earths and technology transfer is also being worked towards, with export curbs on US chips easing market nervousness and bolstering the tech sector, especially chipmakers like Nvidia.

However, deals with Japan and the EU have proved more elusive. Japan faces the risk of a 35% tariff on agricultural exports unless a last-minute breakthrough is achieved. Talks with the EU have stalled amid internal divisions and pushback against what European leaders view as punitive tariff threats. The White House has threatened to impose reciprocal rates on EU exports if an agreement isn’t reached by July 9.

Markets reflect trade optimism but downside risks remain

Market pricing suggests traders expect a relatively smooth outcome from the July 9 deadline. Equity markets remain buoyant, credit spreads are tight, and implied volatility has declined across asset classes. Investors appear confident that the US will strike additional deals or issue tariff letters that fall short of the maximum rates threatened in April.

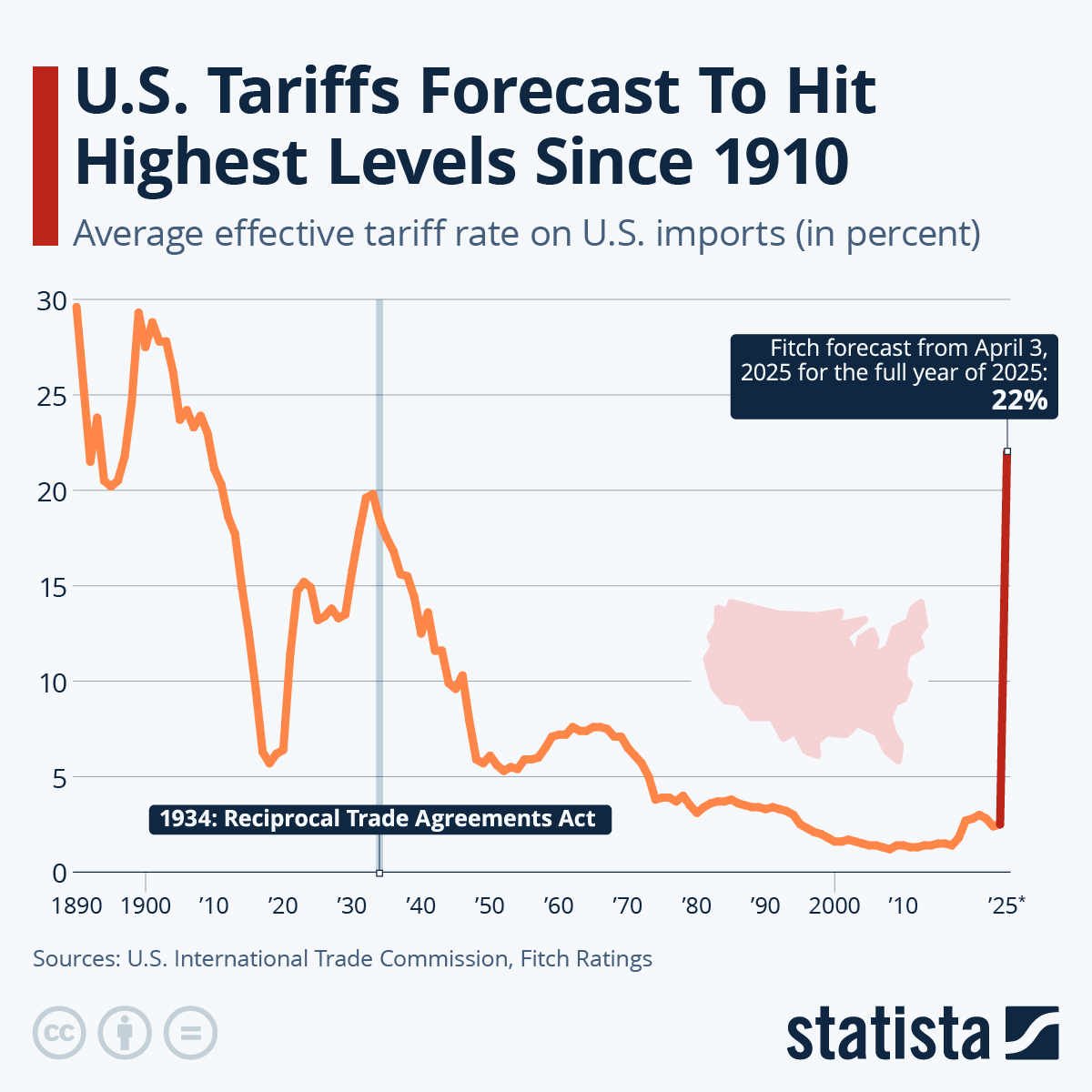

The markets are likely expecting an average effective tariff across US imports of between 10–15%, significantly lower than the 20–30% rates proposed at the height of the Liberation Day panic. The return of risk appetite, particularly in equities, reflects that expectation.

(Source: Statista)

However, this creates an asymmetric risk profile. Much of the “good news” is already priced in. Any shortfall in trade negotiations—or an aggressive stance in the letters issued to remaining trading partners—could quickly unwind recent gains. A failure to reach deals with Japan or the EU, for instance, would likely trigger a repricing in equities, a widening of credit spreads, and renewed pressure in the bond market. The US Dollar would likely retreat once again, with flow likely to be driven into gold as well as other safe haven currencies like the Euro and JPY.