AUD/USD steady ahead of GDP as markets reassess the RBA outlook

Australian GDP growth is tipped to rise with hotter inflation leading the markets to price in the chance of an RBA hike in the near future.

The latest Australian GDP data for the September quarter will be released on Wednesday, 3rd of December, 2025.

Economists tip a lift in Australia growth in September quarter

Consensus expectations point to quarterly GDP growth of around 0.6–0.7%, lifting annual growth to roughly 2.2%. While still subdued, this would mark an improvement from earlier in the year and reflects tentative improvements in household activity. Real household consumption had been under pressure from high rates, but the sector has shown signs of improving following rate cuts from the RBA. Retail spending has stopped deteriorating, and wage gains are providing a little more support than earlier in the tightening cycle, with real wages growing modestly.

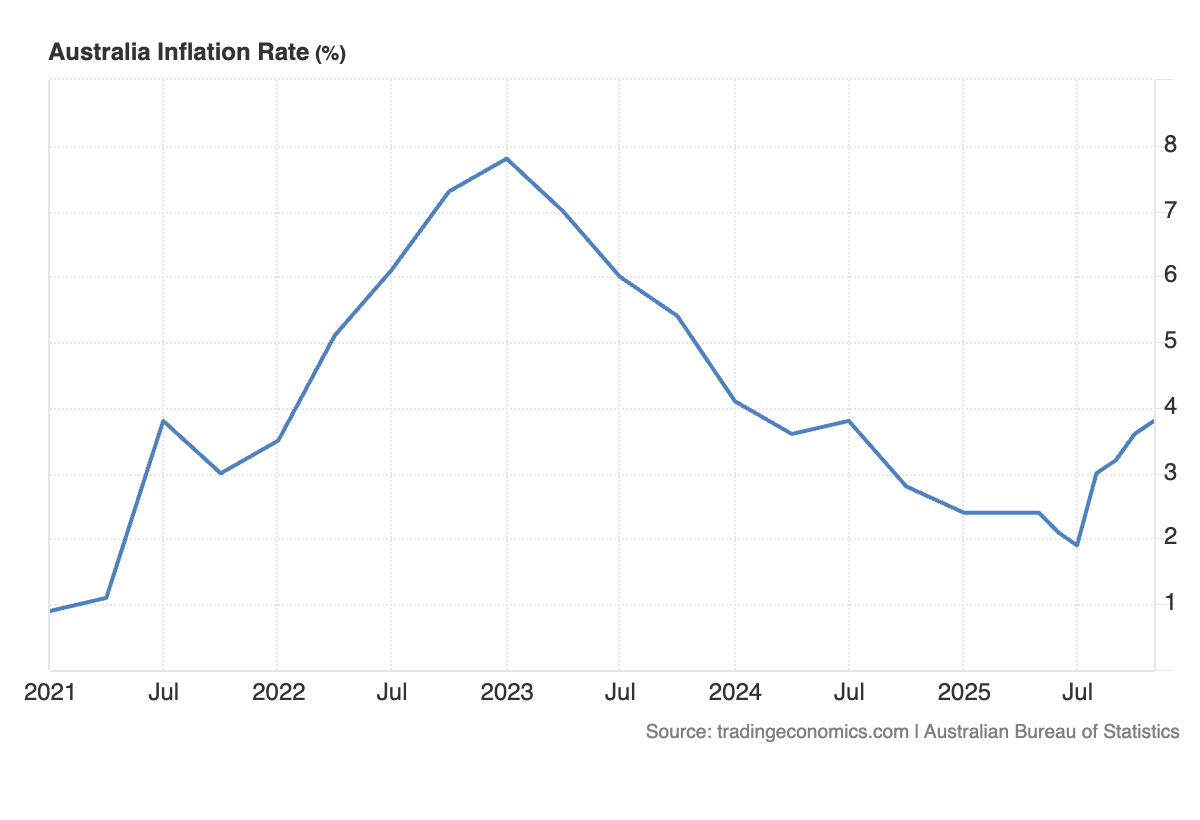

Inflation re-accelerates above the RBA’s target band

The GDP release arrives at a time when inflation momentum is turning higher again. The September-quarter CPI print surprised to the upside, and the latest monthly indicator rose to 3.8%, pushing inflation back above the RBA’s 2–3% target band. Price pressures remain concentrated in services, where demand is still firm, while housing-related inflation continues to be driven by strong population growth and ongoing constraints on supply.

(Source: Trading Economics)

Despite below-trend GDP growth, inflation has proven persistent. Typically, softer demand would be expected to ease price pressures, but Australia’s supply-side constraints are amplifying the inflationary impulse. The most notable issue is extremely weak productivity growth, which has limited the economy’s capacity to absorb demand without generating additional inflation. This means that even modest household and business spending is translating into higher prices rather than higher output.

This dynamic — low growth but insufficient supply — explains why the RBA is finding it harder than expected to return inflation to target. The economy is operating below potential, but potential itself has grown slowly because productivity has been stagnant for several years. With demand running ahead of the economy’s constrained capacity, inflation remains sticky across key categories.

Rates markets shift toward the risk of another RBA hike

A month ago, rates markets were confidently leaning toward RBA rate cuts in late 2025. But the recent inflation surprises and the firming in the monthly CPI series have triggered a meaningful repricing. Futures curves now imply that the next move from the RBA could be a hike, reflecting concern that the central bank may not have done enough to ensure inflation’s return to target in a reasonable timeframe.

(Source: Bloomberg, ASX, Capital.com)

For the AUD/USD, the GDP result will be an important catalyst. A stronger-than-expected print reinforcing the hawkish repricing could offer support to the currency, particularly if US yields stabilise. But a weak outcome — or signs that household momentum is fading again — would likely unwind some of the tightening premium now priced into the curve and weigh on the Aussie heading into year-end.

There is also the matter of the US Dollar, which has pulled back recently because of expectations of a looming US Federal Reserve rate cut. If the Dollar reverses, perhaps because a cut doesn’t materialise, or because the central bank delivers a hawkish cut at its next meeting, that could also weigh on the AUD/USD

From a technical perspective in the short-term, the AUD/USD remains in a downtrend, marked by higher-lows and lower-lows. The pair does remain above its 200-day moving average, having sustained an uptrend for much of 2025. A break above 0.6620 could indicate a reversal of this short-term downtrend. Meanwhile, a push below 0.6420 could signal further bearish and a deeper downtrend.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)