Michael Kramer: Why Is Trimmed Mean PCE Kevin Warsh's Preferred Inflation Gauge?

What gets called 'inflation' in the headlines is really the change in a price index — and how that index is built shapes the number.

Author: Michael Kramer, Mott Capital Management | For publication on Capital.com

The Personal Consumption Expenditures (PCE) Index is generally viewed as the Federal Reserve's preferred inflation measure because it attempts to capture the goods and services consumers spend on, while adjusting for changes in spending behaviour over time. It is still ultimately an index, meaning that trimming or excluding certain components can materially alter the inflation rate it reports.

What Is Trimmed Mean PCE

With the change in Fed leadership, alternative inflation measures attracted greater attention. Trimmed Mean PCE is not a gauge typically found in official government reports, because it is not one of the government's official inflation measures — it is produced each month by the Dallas Fed following the Bureau of Economic Analysis's release of the official PCE report.

Trimmed Mean PCE measures inflation by ranking all PCE components each month based on their price changes, then trimming away the outliers. The result is an inflation measure designed to filter out unusually large price swings — different from core PCE, which simply excludes food and energy prices. In the Dallas Fed's methodology, 24% of the weight from the lower tail and 31% from the upper tail are trimmed*1; these percentages are based on historical data and are designed to better capture persistent inflation pressures.

During his Senate testimony, Warsh said he liked looking at measures called trimmed averages*2 because they help filter out shocks and noise. That suggested Warsh viewed the Trimmed Mean PCE as a better gauge of underlying inflation trends. Whether that represented a move away from core PCE as the Fed's primary metric remained a separate question — one that, if answered in the affirmative, would mark a meaningful shift, given that Trimmed Mean PCE has been running below core PCE for some time.

Core vs. Trimmed Mean PCE

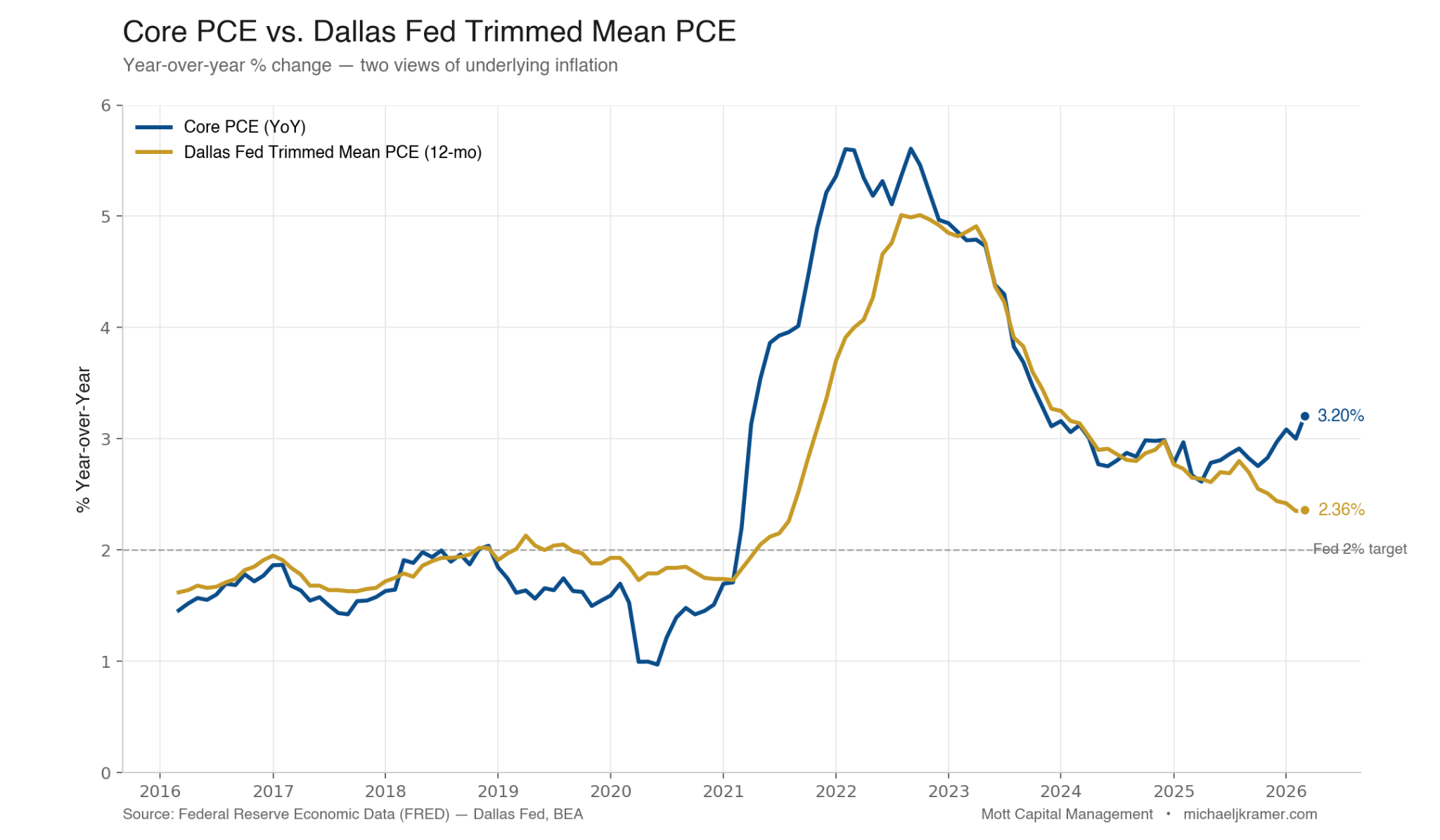

In March 2026, Trimmed Mean PCE was running at roughly 2.4% year-on-year, while core PCE was closer to 3.2%. The divergence between the two measures over the past year has been marked. Taken at face value, the lower Trimmed Mean reading could be read as suggesting less underlying inflation pressure than core PCE implied. That said, Trimmed Mean PCE was slower to pick up the rise in inflation during 2021, and continued to rise until August 2022, even after core PCE peaked in March 2022.

Relying more heavily on the Trimmed Mean PCE has at times produced unintended outcomes. In 2018 and 2019, Trimmed Mean PCE remained noticeably higher than core PCE, which was steadily declining. Had the Fed focused more heavily on trimmed mean measures during that period, it might have remained more hawkish through the 2019 rate-cutting cycle and perhaps would not have cut rates at all.

(Source: Federal Reserve Economic Data (FRED) - Dallas Fed, BEA)

(Past performance is not a reliable indicator of future results)

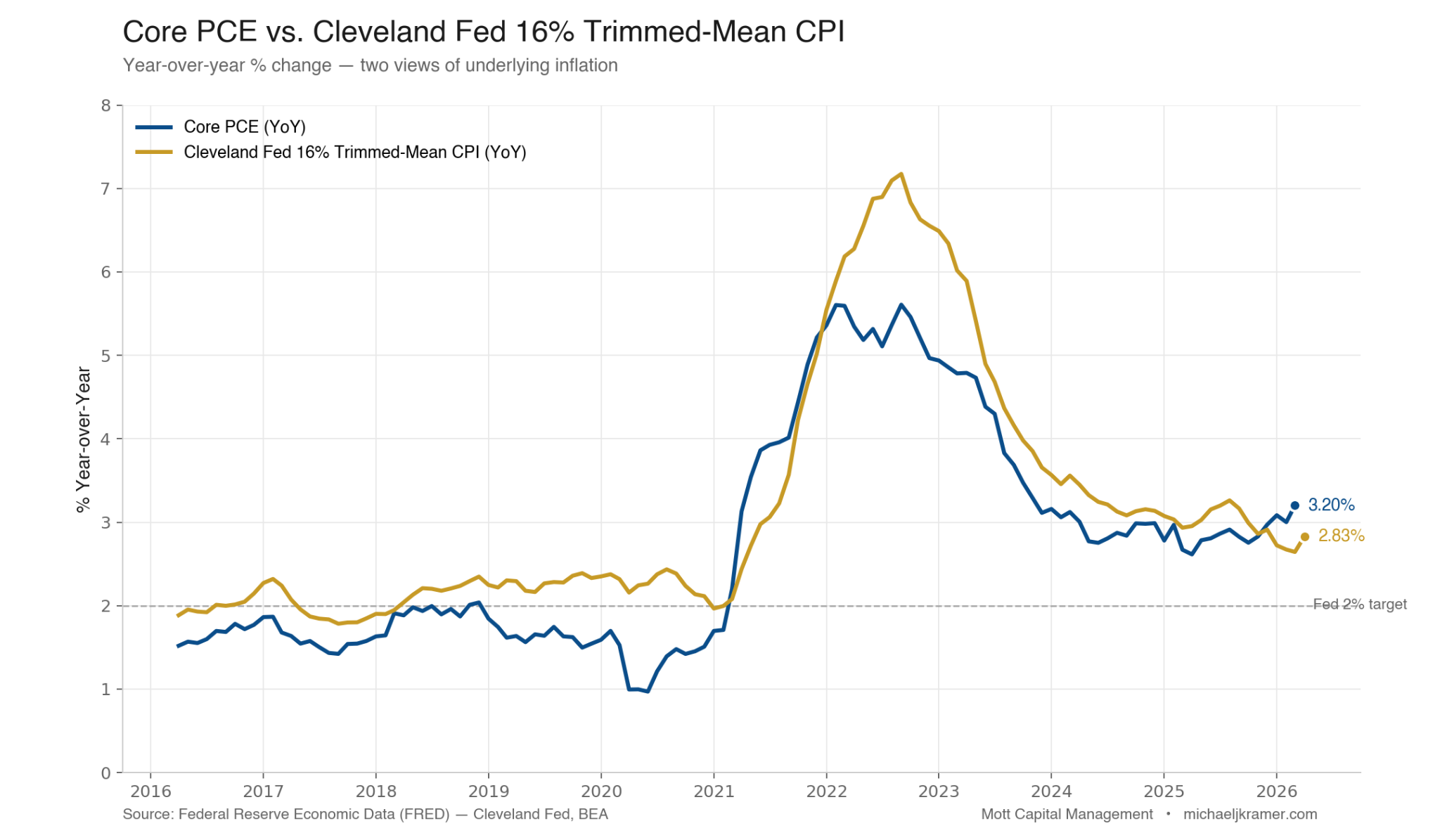

Another trimmed inflation measure comes from the Cleveland Fed: the 16% trimmed-mean CPI. That gauge trims the 8% highest and 8% lowest monthly price changes from CPI components. It tends to run at a higher rate than core PCE and is not a particularly close match for it, given methodological differences between CPI and PCE.

(Source: Federal Reserve Economic Data (FRED) – Cleveland Fed, BEA)

(Past performance is not a reliable indicator of future results)

Transition Away From Core PCE

The timing of any transition towards a different inflation measure would be challenging during an energy or supply shock. While such moves would generally be filtered out of a Trimmed Mean PCE reading, by the time they appeared in the data, the inflation impulse may have already spread more broadly — much like what occurred in 2021.

Trimmed Mean PCE has proven a useful lens for policymakers, but it has not displaced the inflation measures the Fed relies on. Much like the 'super-core'*3 measures that gained prominence in recent years, Trimmed Mean PCE has continued to serve as a supplementary tool rather than a replacement for the Fed's primary inflation benchmarks.

Sources

*1 Dallas Fed — Trimmed Mean PCE methodology: https://www.dallasfed.org/research/pce/descr

*2 CNBC — Kevin Warsh on inflation measures (April 2026): https://www.cnbc.com/2026/04/22/kevin-warsh-inflation-trend-pce-trump.html

*3 St. Louis Fed — Measuring inflation: headline, core, and super-core: https://www.stlouisfed.org/on-the-economy/2024/may/measuring-inflation-headline-core-supercore-services

This article is written by Michael Kramer of Mott Capital Management and is published on Capital.com for educational and informational purposes only. The content does not constitute financial advice or a recommendation to buy or sell any financial instrument. Past performance is not a reliable indicator of future results. CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. The majority of retail investor accounts lose money when trading CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.