US Non-farm Payrolls forecast to show continued labour market sluggishness

The Non-Farm Payrolls data is keenly awaited by traders looking to gauge the path for US interest rates, but may be delayed by the US government shutdown.

The September Non-Farm Payrolls data is due for release on Friday, October 3, but could be delayed because of the US Government shutdown.

Forecasters predict modest jobs growth in September

Consensus forecasts suggest the US economy added around 51,000 jobs in September, with the unemployment rate seen holding steady at 4.3%. That marks a slowdown in headline jobs growth and aligns with broader signs of cooling in the labour market. Fed officials have recently suggested that the economy’s “breakeven” rate of job creation—the level needed to keep unemployment stable—sits between 25,000 and 50,000 jobs. That underscores how slower hiring has so far not translated into higher unemployment, thanks in part to tighter labour supply.

A significant driver of the labour market’s unusual dynamics has been the Trump administration’s restrictive migration policies, which have curtailed labour supply. This supply shock has helped keep the unemployment rate lower than it might otherwise be, even as job creation eases.

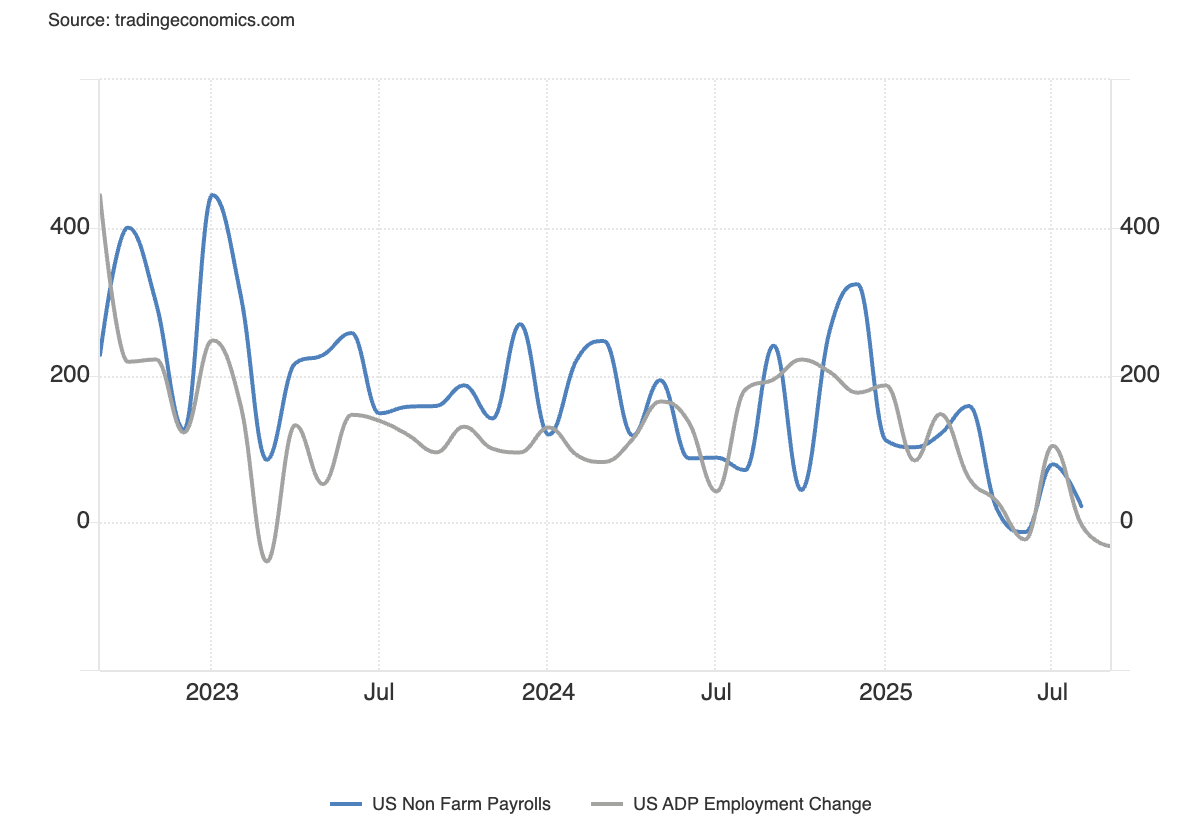

September’s ADP private payrolls report showed a surprise contraction of 32,000 jobs, raising the risk that the official data could soon reflect outright job losses. Economists caution that revisions to prior payrolls releases could reinforce that trend, intensifying concerns about deteriorating labour market conditions.

(Source: Trading Economics)

Adding uncertainty, the release may not go ahead on schedule if the Bureau of Labor Statistics is impacted by the ongoing US government shutdown. Should that occur, the data will be published only once government operations resume, delaying an important signal for markets at a crucial juncture.

The markets position for aggressive Fed rate cuts

The jobs report carries major implications for monetary policy. Markets are already positioned for imminent Federal Reserve rate cuts, with futures pricing a fully priced-in October reduction and a December move carrying an implied probability of around 90%. The markets are implying a trough rate next year below 3% once again. Evidence of further weakness in the labour market could cement those expectations and accelerate the pace of policy easing.

The USD/JPY remains the cleanest expression for US rate expectations, especially with the markets pulling forward the timing of the next Bank of Japan cut. The pair is carving out a broadening formation, reflecting the uncertainty regarding both Fed and BOJ policy expectations. Buyers have generally emerged for the USD/JPY below 147, with 145.50 another key support level in the short-term. Meanwhile, critical resistance for the pair sits around 150.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)