The markets look for evidence of easing inflation as US economy hits potential air pocket

Discover how US inflation data and Federal Reserve rate cut expectations are shaping market trends. Learn about economic slowdown concerns, trade policy impacts, and the US Dollar’s performance.

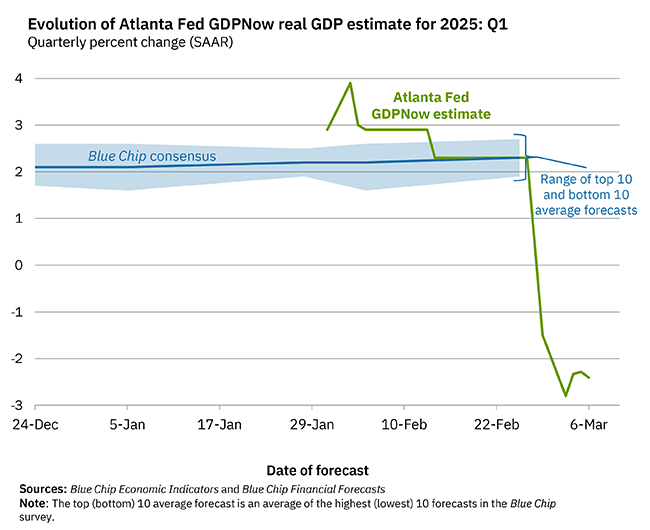

The latest US inflation data comes amidst increased uncertainty about US trade policy and its impact on economic activity. US indices and the US Dollar have plunged as the markets price-in a slowdown in growth caused by the imposition of tariffs and the lack of clarity about future trade restrictions. Recent forward looking indicators of economic activity have shown a deterioration in consumer confidence and business conditions, with PMI surveys revealing the drag on employment and investment intentions caused by unstable economic policy. The dynamic has contributed to rising expectations that the US economy will experience a contraction in growth in the first quarter, with the oft-quoted Atlanta Fed GDPNow model pointing to a 2.4% decline in GDP.

(Source: Atlanta Fed)

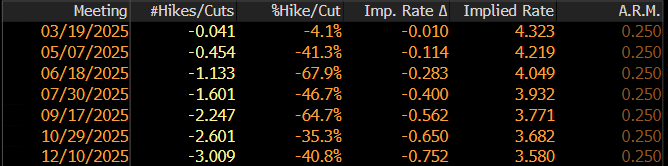

As a result of an expected economic slowdown, the markets have brought forward the timing of the next US Federal Reserve interest rate cut and increased the number of cuts priced into the futures curve in 2025. The next cut is fully baked in for the June meeting, with a further two cuts considered likely before the end of the year.

(Source: Bloomberg)

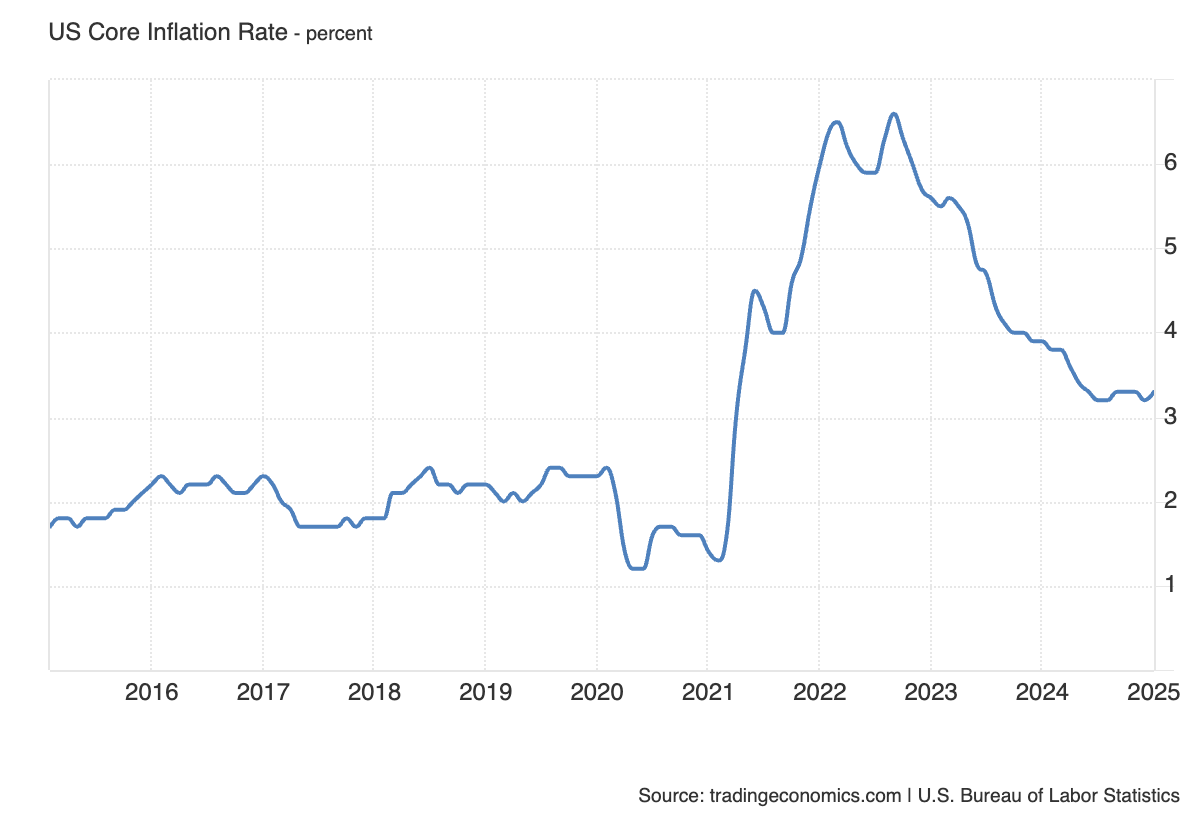

The Fed’s ability to cut interest rates relies on inflation continuing to moderate. The shift in market pricing suggests that the likely slowdown in growth is expected to weaken demand enough to lower price pressures. Arguably, inflation has been stuck, even re-anchored, around 3% largely due to resilient growth. The February CPI figures are tipped to show a very modest drop in headline and core CPI, following last month’s surprise jump, dismissed by many as being driven by new year price increases. Economists project headline inflation will dip to 2.9%, with core easing to 3.2%.

(Source: Trading Economics)

Steady or even an (albeit unlikely) increase in inflation for the month could stoke further volatility in financial markets. That’s because although there are serious growth concerns stemming from US President Donald Trump’s economic policies, there’s hope any slowdown can be managed by the Fed by cutting interest rates. Further evidence of sticky prices will mean the Fed has less wriggle room to cut rates in response to slowing demand, with the temporary price shock caused by tariffs also potentially complicating the central bank’s job.

Heading into the CPI release, the US Dollar’s short-term trend remains clearly to the downside as the US economy’s period of exceptional outperformance appears to be nearing an end. In the short-term, the Greenback appears slightly oversold, with the EUR/USD well below the 30-level on the RSI after testing a rejecting resistance at 1.0940/50. The RSI is indicating slowing upside momentum, although is flashing decisively bearish signals yet.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)