The markets expect FOMC to cut but outlook in 2025 is less certain

Markets expect a 25bp rate cut at the FOMC meeting on December 18, 2024, amid strong U.S. economic data. However, the outlook for 2025 remains uncertain as inflation and growth trends evolve.

As the Federal Open Market Committee (FOMC) prepares to convene on December 18, 2024, market participants are keenly focused on how the U.S. Federal Reserve will navigate its policy stance amid evolving economic dynamics. With inflation, employment, and GDP growth data painting a robust economic picture, expectations for a 25 basis-point rate cut are firmly priced in. However, what comes next remains a subject of debate.

Recent data points to resilient US economic growth

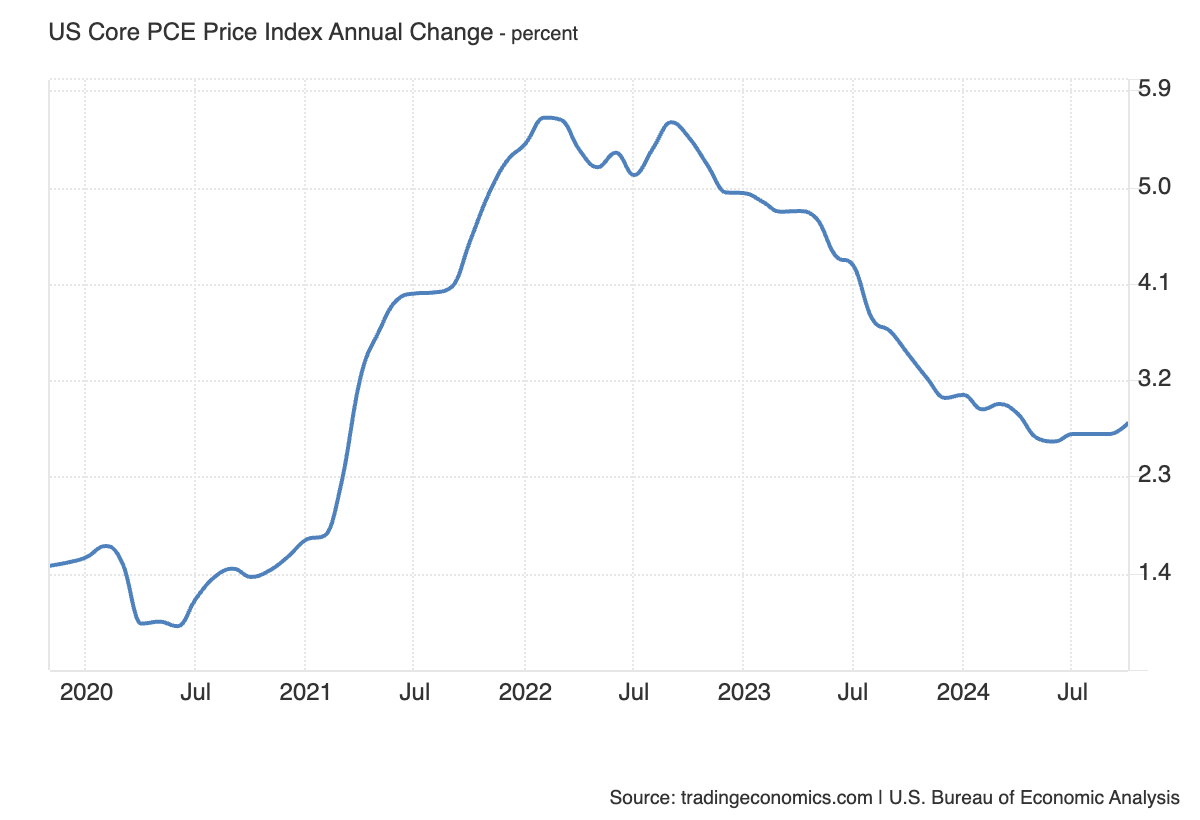

The U.S. economy has shown remarkable resilience. Inflation, as measured by the Personal Consumption Expenditures (PCE) price index, has moderated but remains above the Fed’s 2% target. Core PCE inflation stood at 2.8% year-on-year in October 2024, reflecting persistent service-sector inflation despite easing goods prices.

(Source: Trading Economics)

On the employment front, the latest Non-Farm Payrolls (NFP) report showed a gain of 227,000 jobs in November 2024, signalling strong labour demand, although the unemployment rate edged up to 4.2%. Wage growth increased by 0.3% month-on-month, translating to a year-over-year gain of 4.0%, stoking concerns about upside risks to inflation going forward. These figures suggest continued labor market strength and potentially ongoing excess demand, but ultimately highlight a modest loosening compared to prior months.

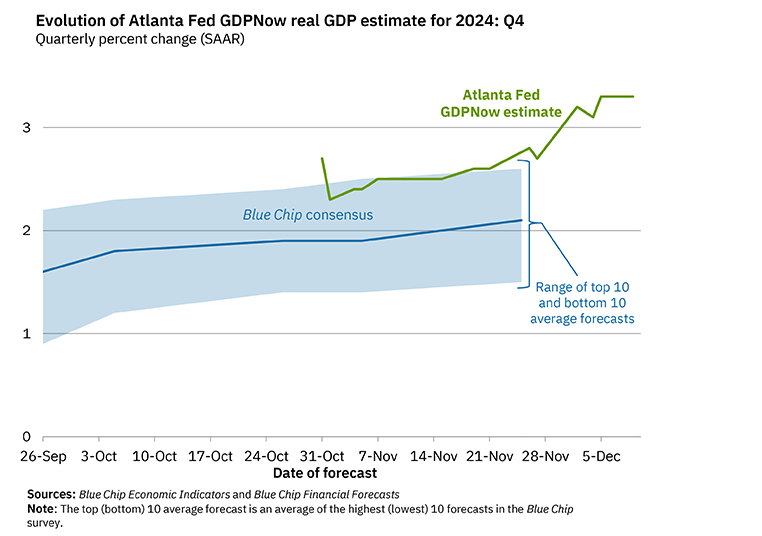

GDP growth for Q3 2024 was revised upward to 2.8% annualized, driven by solid consumer spending and business investment. Early Q4 indicators, including retail sales and industrial production data, suggest the economy is expanding at a still robust pace. The Atlanta Fed’s GDPNow indicator projects an above trend 3.3% growth rate for Q4.

(Source: Atlanta Fed)

The Fed is expected to cut but a pause in January is on the table

Markets are pricing in a 25 basis-point rate cut at the December meeting, which would lower the target range for the federal funds rate to 4.25% - 4.50%. On the day of the start of the FOMC meeting, Fed Funds Futures imply a 95% chance of a cut. Looking ahead, fed funds futures suggest a possible pause at the January 2025 meeting, reflecting the Fed's cautious approach amid resilient economic data. The markets ascribe an 80% chance of a January hold.

(Source: CME Group)

Beyond January, traders anticipate another 50 basis points of cuts throughout 2025. However, expectations are fluid, hinging on incoming data. A more dovish outlook could emerge if inflation cools faster than expected, while persistent inflationary pressures, possibly generated by stimulatory fiscal settings and tariffs from the Trump administration, might force the Fed to adopt a less aggressive easing cycle.

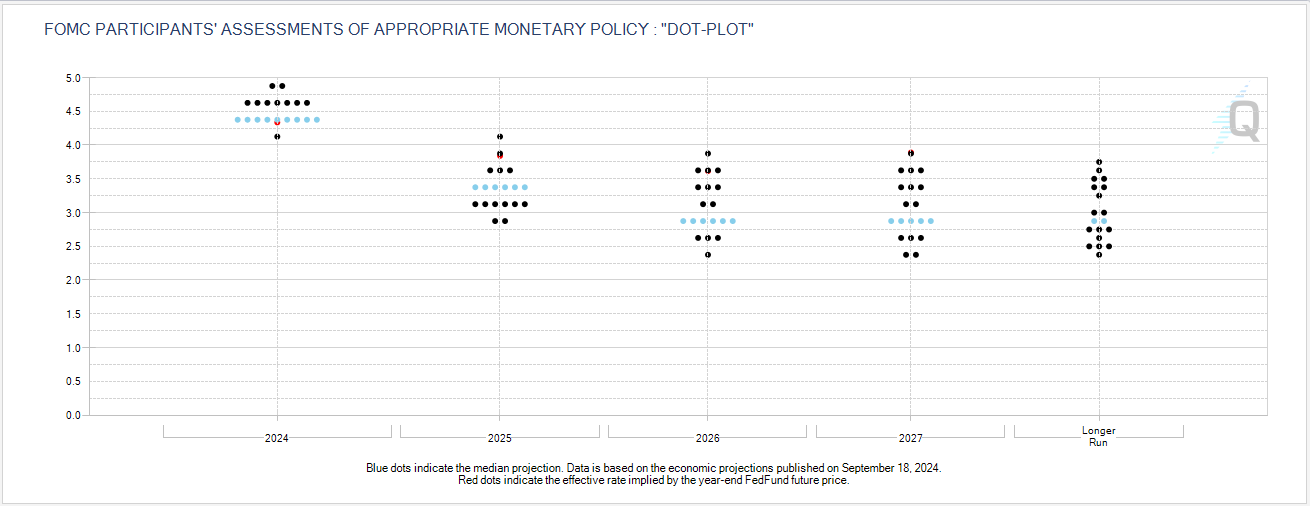

FOMC's September Projections: An Update Expected

The "dot plot," which outlines FOMC members' expectations for future rate levels, could also shift upward with the latest Summary of Economic Projections. Policymakers may signal a slower path to rate cuts in 2025, aligning with firmer growth and persistent inflation risks. Unemployment forecasts could be adjusted lower, acknowledging continued labor market strength.

While such a move would ostensibly be hawkish, the markets have already shifted to reflect fewer cuts in 2025, a higher trough rate, and a higher neutral rate than Fed forecasters projected. It suggests that the bar may be set high for a hawkish surprise, with the markets able to stomach structurally higher rates.

(Source: CME Group)

The markets look for signals of a hawkish or dovish cut

The market's reaction will depend on the Fed's forward guidance. Two primary scenarios are in play:

1. Dovish Cut with Open Door for More Easing

If the Fed cuts rates and emphasizes data dependence with a bias toward further easing, equity markets could rally as risk sentiment improves. Treasury yields would likely fall, weakening the U.S. dollar and boosting gold prices as real yields decline.

2. Hawkish Cut with Pause Signal

If the Fed cuts but hints at a pause or fewer cuts in 2025, markets could react defensively. Stocks might retreat amid concerns of tighter financial conditions. Bond yields could rise, strengthening the U.S. dollar and pressuring gold prices as investors adjust for a less accommodative Fed.

3. A Cut with Neutral Guidance

The Fed could cut rates but offer neutral guidance, potentially emphasising data dependence. Such a move would likely support a risk on move in markets as assets prices price-out the volatility associated with the event.

PCE data could inform rate expectations

The FOMC decision will be followed by the November PCE Index release a day later. The data may build-on or reverse the case for a January rate pause and inform expectations for inflation in 2025 and the shape of the futures curve. Consensus expectations point to a 0.3% month-on-month increase in core PCE, translating to a 2.9% annual gain. A softer-than-expected reading could reinforce the case for a prolonged easing cycle, while an upside surprise might temper market expectations for additional cuts.

FOMC the final hurdle in the way of a Santa rally

The S&P 500 remains in an uptrend and looks technically constructive, although upside momentum is slowing down. The market is pulling back going into the FOMC as traders position for the risk event. However, it’s carving out a symmetrical triangle continuation patterning, signalling a possible break-out. Such a break-out may see another test of the S&P 500’s upward sloping trend line resistance. On the downside, short-term support may be around the 6020 level and the 20-day MA.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)

References

- https://www.bls.gov/news.release/empsit.nr0.htm

- https://www.atlantafed.org/cqer/research/gdpnow

- https://www.bea.gov/news/2024/personal-income-and-outlays-october-2024

- https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

- https://www.federalreserve.gov/monetarypolicy/fomcprojtabl20240918.htm