RBA expected to cut again: markets look for dovish clues

The markets have fully priced in an RBA cut, with attention at this meeting on the central bank's guidance.

The Reserve Bank of Australia (RBA) is expected to deliver another interest rate cut at its July meeting, as the balance of risks in the Australian economy continues to shift from inflation toward growth and employment. With markets fully pricing in a 25-basis point reduction, taking the cash rate to 3.60%, the immediate focus is likely to fall on the tone of the central bank’s guidance and how much further easing is on the table before the year is out.

Inflation tamed, growth cracks emerging

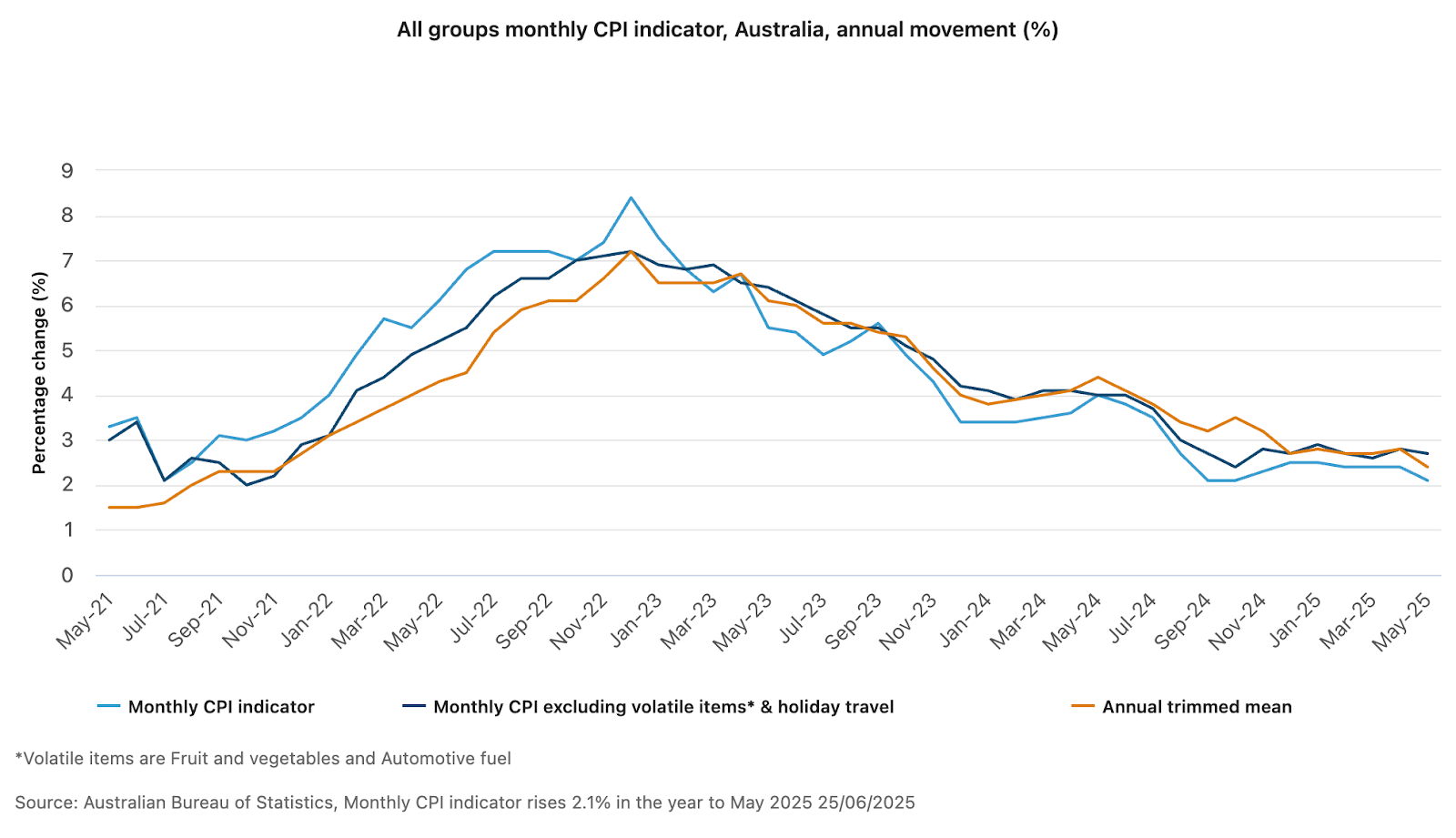

Australia’s macroeconomic environment has changed meaningfully in recent months. Inflation has returned to within the RBA’s 2–3% target band, with the official trimmed mean CPI coming in at 2.9% in the March quarter. More recently, the monthly CPI indicator’s annual trimmed mean fell to 2.4%, reinforcing the view that price pressures have broadly normalised.

(Source: ABS)

At the same time, signs of softening in the labour market have emerged. The unemployment rate remains relatively low at 4.1%, but May's employment report revealed a loss of 2,500 jobs, driven entirely by declines in part-time employment. While not alarming in isolation, the data adds to concerns that domestic demand may be flagging amid tepid domestic demand and sluggish global growth.

The RBA shifts gears: inflation to employment

The RBA’s previous meeting marked a clear dovish shift in tone, with policymakers placing greater emphasis on the employment side of their dual mandate. With core inflation essentially under control, the focus has turned to insulating the economy from downside risks—particularly those stemming from global demand weakness and trade policy uncertainty abroad.

The decision to pivot in May came despite slower progress towards the inflation target than expected. However, the RBA’s Statement on Monetary Policy, updated at that meeting, revealed a deeper expected decline in inflation and a deterioration in growth conditions. That underscored the RBA’s growing concern about the growth outlook and a willingness to pre-emptively ease policy to prevent a more pronounced slowdown, particularly as Australia remains highly exposed to swings in global trade.

Markets fully priced: guidance will be key

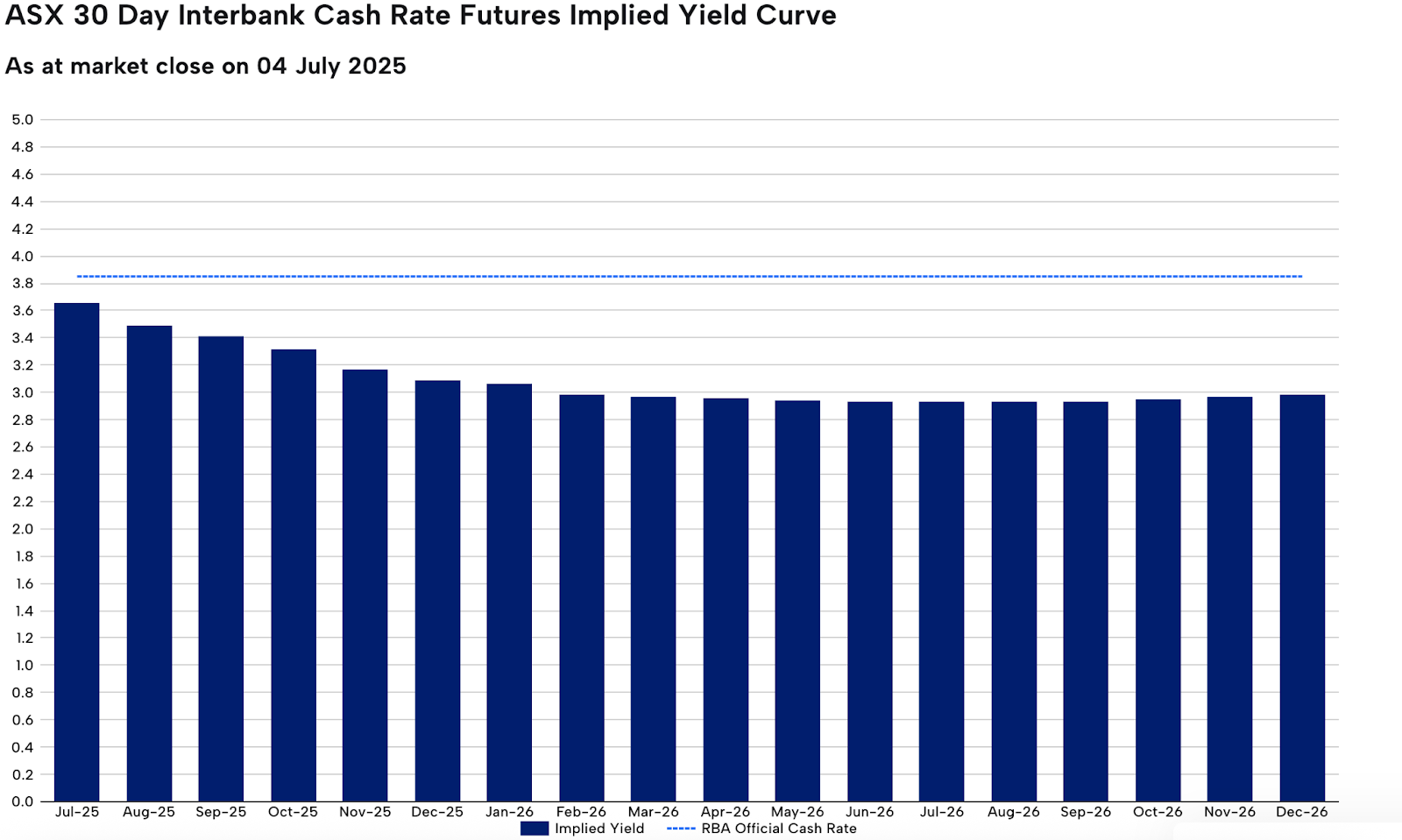

Futures markets are pricing in 27 basis points of easing for the July meeting, implying a 25bp cut is fully expected, with a non-zero probability of a 50bp move. That said, a double cut would be a genuine surprise and is viewed as unlikely. The bar for a dovish surprise is therefore high, and the market reaction may hinge more on the RBA’s forward guidance than the headline decision itself.

(Source: ASX)

Should the RBA signal that further cuts are likely—perhaps hinting at two additional moves by year-end, as current pricing implies—the Australian Dollar could come under renewed pressure while local equities receive a modest tailwind. However, in the absence of such guidance, the risks are asymmetric. A more balanced or cautious tone could trigger a mild hawkish repricing, supporting the AUD/USD and weighing on stocks.