Nvidia Q3 Earnings Preview: Hyperscaler demand, new chip ramp-ups, and China export risks in focus

Nvidia is tipped to deliver another strong set of quarterly results, but will guidance live up to expectations?

Nvidia is set to release its fiscal Q3 2026 earnings after market close, with expectations once again elevated despite a recent pullback in the share price.

Strong Q3 growth forecast, but guidance will shape the stock’s next move

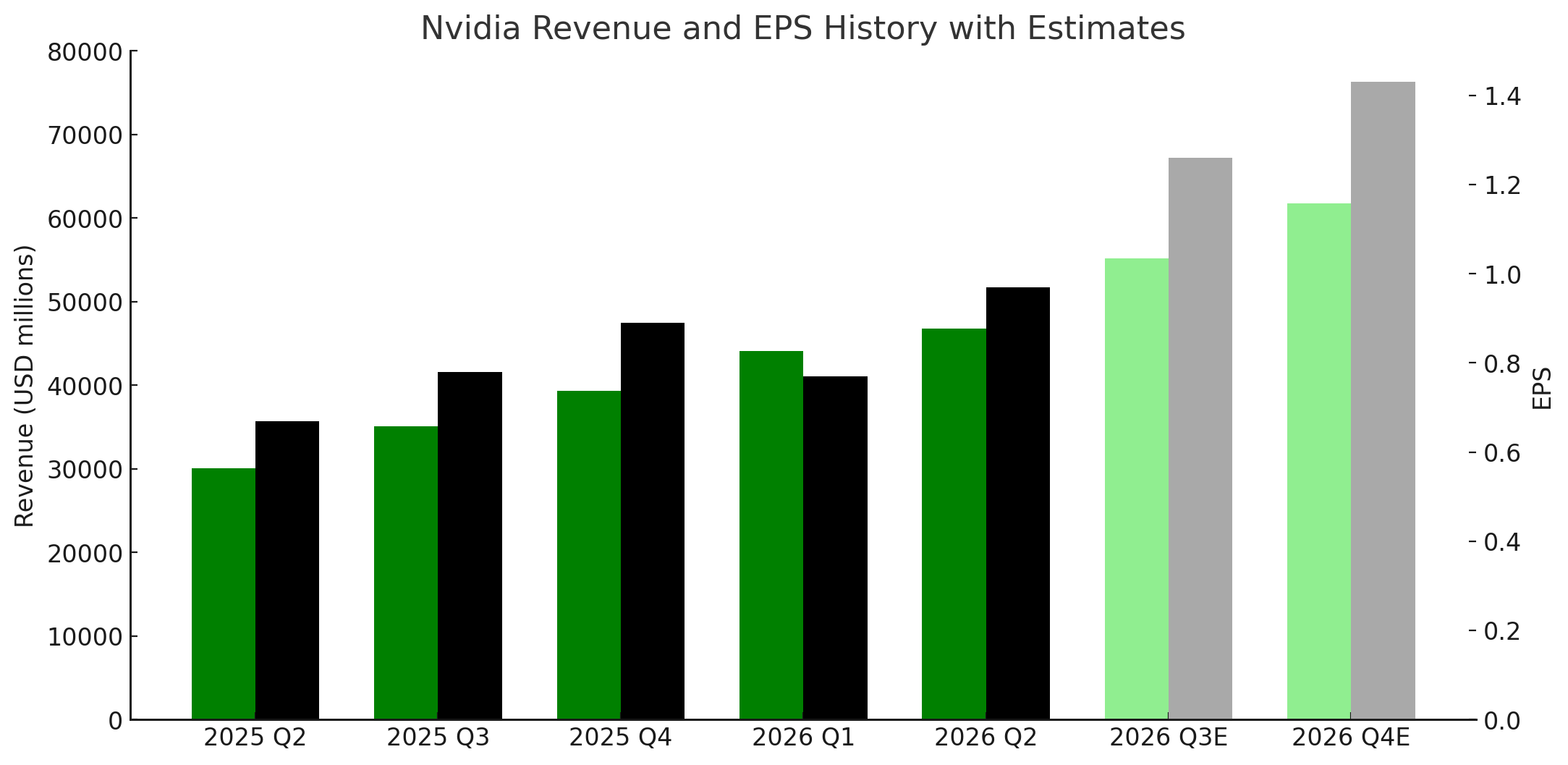

Analysts expect Nvidia to deliver adjusted EPS of $1.26, up from $0.97 in Q2 and showing 61% year-on-year growth. Revenue is forecast to reach $55.18 billion dollars, a meaningful acceleration from Q2’s $46.74 billion and nearly 56% higher than the prior year.

(Source: Capital.com, Bloomberg)

Nvidia’s profit metrics remain strong. Adjusted net income is estimated at $30.83 billion, reflecting sector-leading operating leverage and demand for Nvidia’s GB300, Blackwell and networking platforms. Gross margins are projected at 73.6 percent, a lift from a quarter earlier as costs are brought down and scale is achieved.

Consensus expectations are that Nvidia’s results will again benefit from ongoing hyperscaler deployments, robust enterprise and sovereign AI investment, and the earnings contribution from early Blackwell shipments. However, with the market already accustomed to multi-quarter beats, guidance will be the primary determinant of whether the stock can sustain or extend its rally. Commentary around hyperscaler budgets, supply availability and the 2026–27 demand pipeline will be crucial for sentiment. Currently, analysts forecast revenues and EPS for the final quarter of fiscal 2026 of $61.7 billion and $1.43 per share.

Export restrictions continue to influence revenue growth and remain a risk to the outlook. China remains effectively closed to Nvidia, and while the company has designed compliance-grade alternatives, demand has yet to scale meaningfully.

Nvidia remains one of the world’s largest companies, with a market cap nearing $5 trillion even after recent corrections. Analyst sentiment is overwhelmingly positive: 91.8% boast buy ratings, with an average target price of $235.69, implying roughly 20% upside from current levels.

Nvidia shares hold key support as momentum cools

Nvidia’s share price remains in a clear long-term uptrend, though momentum has eased. The stock has recently pulled back toward the $180 level, a critical zone defined by previous resistance now acting as support. A break below that level could open the door to downside and call into question the stock’s short-term uptrend.

For the uptrend to re-accelerate, the stock will need to reclaim the 210-dollar level. A break to new highs, particularly if driven by strong guidance, would reinforce bullish sentiment not only for Nvidia.

(Source: Trading View)

(Past performance is not a reliable indicator of future results)